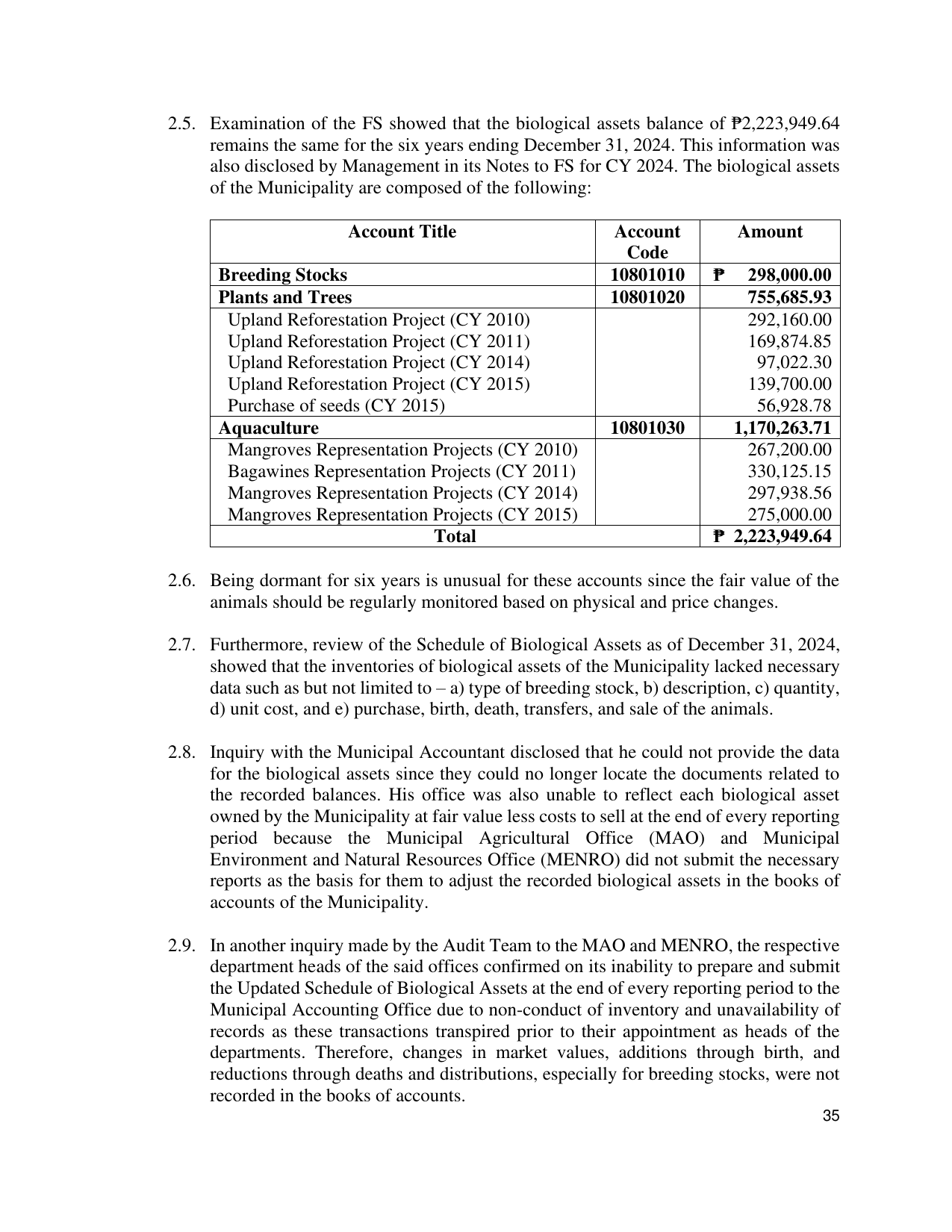

2.5. Examination of the FS showed that the biological assets balance of ₱2,223,949.64

remains the same for the six years ending December 31, 2024. This information was

also disclosed by Management in its Notes to FS for CY 2024. The biological assets

of the Municipality are composed of the following:

Account Title Account Amount

Code

Breeding Stocks 10801010 ₱ 298,000.00

Plants and Trees 10801020 755,685.93

Upland Reforestation Project (CY 2010) 292,160.00

Upland Reforestation Project (CY 2011) 169,874.85

Upland Reforestation Project (CY 2014) 97,022.30

Upland Reforestation Project (CY 2015) 139,700.00

Purchase of seeds (CY 2015) 56,928.78

Aquaculture 10801030 1,170,263.71

Mangroves Representation Projects (CY 2010) 267,200.00

Bagawines Representation Projects (CY 2011) 330,125.15

Mangroves Representation Projects (CY 2014) 297,938.56

Mangroves Representation Projects (CY 2015) 275,000.00

Total ₱ 2,223,949.64

2.6. Being dormant for six years is unusual for these accounts since the fair value of the

animals should be regularly monitored based on physical and price changes.

2.7. Furthermore, review of the Schedule of Biological Assets as of December 31, 2024,

showed that the inventories of biological assets of the Municipality lacked necessary

data such as but not limited to – a) type of breeding stock, b) description, c) quantity,

d) unit cost, and e) purchase, birth, death, transfers, and sale of the animals.

2.8. Inquiry with the Municipal Accountant disclosed that he could not provide the data

for the biological assets since they could no longer locate the documents related to

the recorded balances. His office was also unable to reflect each biological asset

owned by the Municipality at fair value less costs to sell at the end of every reporting

period because the Municipal Agricultural Office (MAO) and Municipal

Environment and Natural Resources Office (MENRO) did not submit the necessary

reports as the basis for them to adjust the recorded biological assets in the books of

accounts of the Municipality.

2.9. In another inquiry made by the Audit Team to the MAO and MENRO, the respective

department heads of the said offices confirmed on its inability to prepare and submit

the Updated Schedule of Biological Assets at the end of every reporting period to the

Municipal Accounting Office due to non-conduct of inventory and unavailability of

records as these transactions transpired prior to their appointment as heads of the

departments. Therefore, changes in market values, additions through birth, and

reductions through deaths and distributions, especially for breeding stocks, were not

recorded in the books of accounts.

35