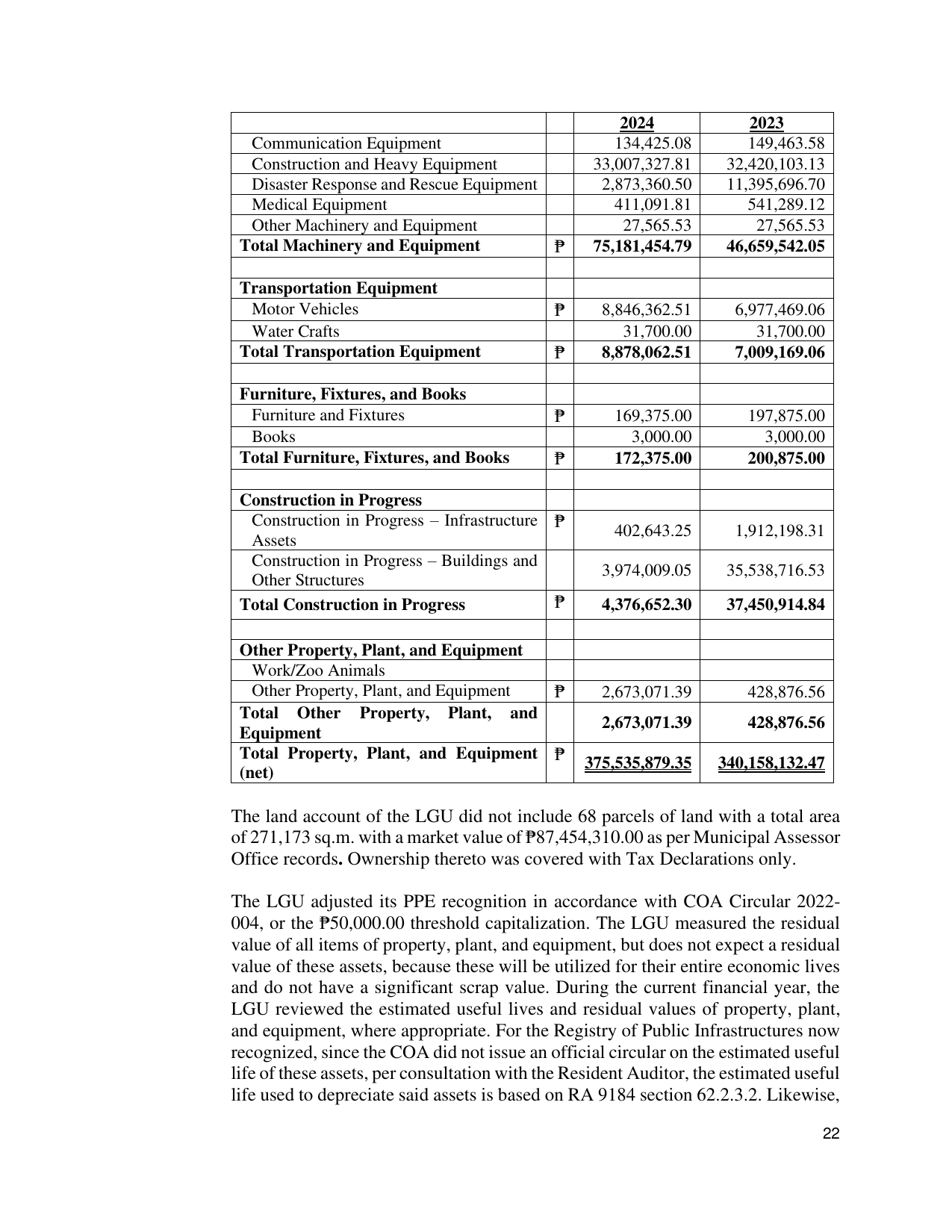

2024 2023

Communication Equipment 134,425.08 149,463.58

Construction and Heavy Equipment 33,007,327.81 32,420,103.13

Disaster Response and Rescue Equipment 2,873,360.50 11,395,696.70

Medical Equipment 411,091.81 541,289.12

Other Machinery and Equipment 27,565.53 27,565.53

Total Machinery and Equipment ₱ 75,181,454.79 46,659,542.05

Transportation Equipment

Motor Vehicles ₱ 8,846,362.51 6,977,469.06

Water Crafts 31,700.00 31,700.00

Total Transportation Equipment ₱ 8,878,062.51 7,009,169.06

Furniture, Fixtures, and Books

Furniture and Fixtures ₱ 169,375.00 197,875.00

Books 3,000.00 3,000.00

Total Furniture, Fixtures, and Books ₱ 172,375.00 200,875.00

Construction in Progress

Construction in Progress – Infrastructure ₱

402,643.25 1,912,198.31

Assets

Construction in Progress – Buildings and

3,974,009.05 35,538,716.53

Other Structures

Total Construction in Progress ₱ 4,376,652.30 37,450,914.84

Other Property, Plant, and Equipment

Work/Zoo Animals

Other Property, Plant, and Equipment ₱ 2,673,071.39 428,876.56

Total Other Property, Plant, and

2,673,071.39 428,876.56

Equipment

Total Property, Plant, and Equipment ₱

375,535,879.35 340,158,132.47

(net)

The land account of the LGU did not include 68 parcels of land with a total area

of 271,173 sq.m. with a market value of ₱87,454,310.00 as per Municipal Assessor

Office records. Ownership thereto was covered with Tax Declarations only.

The LGU adjusted its PPE recognition in accordance with COA Circular 2022-

004, or the ₱50,000.00 threshold capitalization. The LGU measured the residual

value of all items of property, plant, and equipment, but does not expect a residual

value of these assets, because these will be utilized for their entire economic lives

and do not have a significant scrap value. During the current financial year, the

LGU reviewed the estimated useful lives and residual values of property, plant,

and equipment, where appropriate. For the Registry of Public Infrastructures now

recognized, since the COA did not issue an official circular on the estimated useful

life of these assets, per consultation with the Resident Auditor, the estimated useful

life used to depreciate said assets is based on RA 9184 section 62.2.3.2. Likewise,

22