b) The nature of the asset, its susceptibility and adaptability to changes in

technology and processes;

c) The nature of the processes in which the asset is deployed; and

d) Changes in the market in relation to the asset.

Receivables

Receivables are amounts owed by consumers and are presented net of impairment

losses. The LGU has a credit risk policy in place, and the exposure to credit risk is

monitored on an ongoing basis. The LGU is compelled, by its constitutional

mandate, to provide all its residents with basic minimum services, without recourse

to an assessment of creditworthiness. There were no material changes in the

exposure to credit risk and its objectives, policies, and processes for managing and

measuring the risk during the year under review.

The LGU’s maximum exposure to credit risk is represented by the carrying value

of each financial asset in the statement of financial performance. The LGU has no

significant concentration of credit risk, with exposure spread over a large number

of consumers, and is not concentrated in any particular sector or geographic area.

The LGU establishes an allowance for impairment that represents its estimate of

anticipated losses in respect of receivables.

Capital management

The primary objective of managing the LGU’s capital is to ensure sufficient cash

available to support the LGU’s funding requirements, including capital

expenditure, so that the LGU remains financially sound. The LGU monitors capital

using a gearing ratio, which is net debt, divided by total capital, plus net debt. In a

capital-intensive industry, a gearing ratio of 54.5% or less can be considered

reasonable. Included in net debt are interest-bearing loans and borrowings,

payables, less investments.

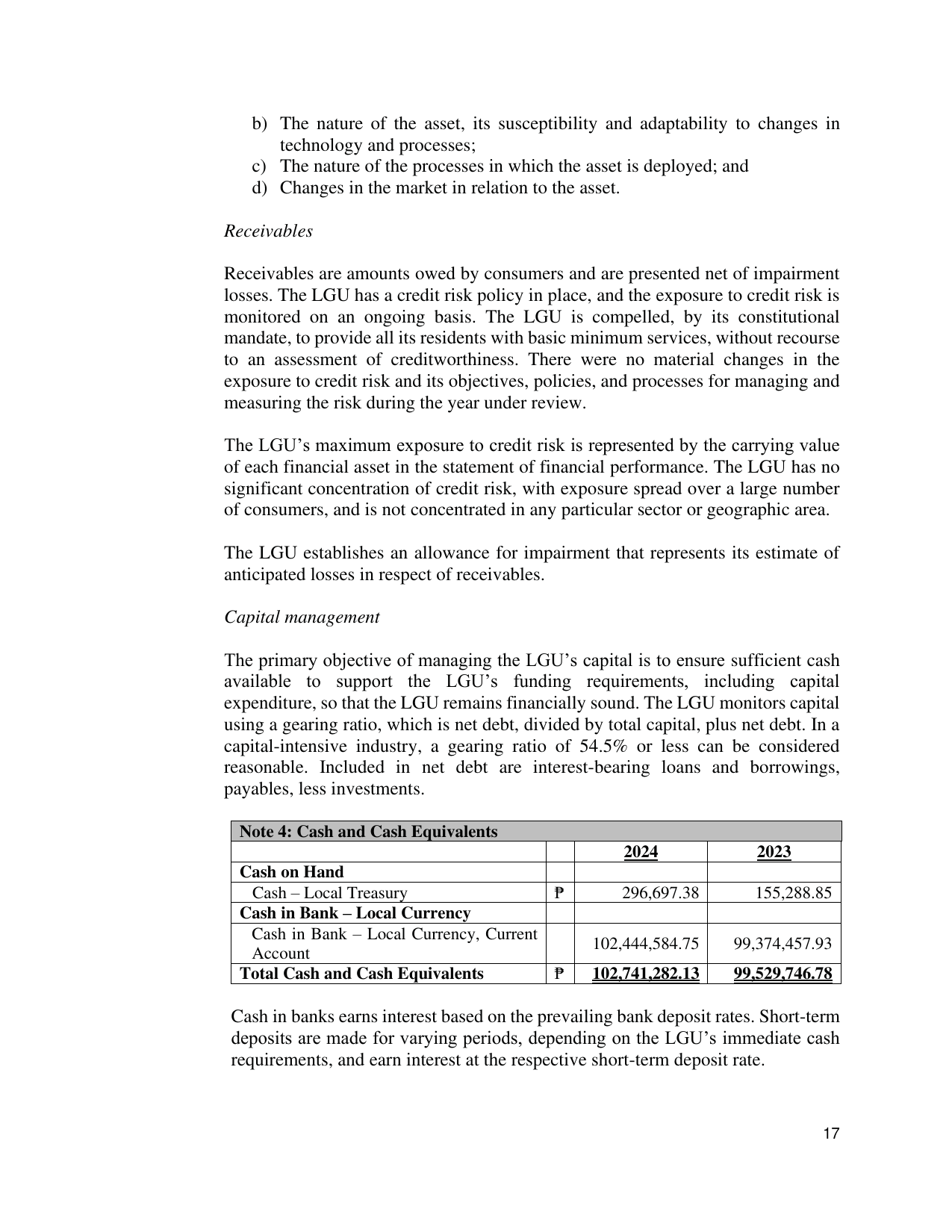

Note 4: Cash and Cash Equivalents

2024 2023

Cash on Hand

Cash – Local Treasury ₱ 296,697.38 155,288.85

Cash in Bank – Local Currency

Cash in Bank – Local Currency, Current

102,444,584.75 99,374,457.93

Account

Total Cash and Cash Equivalents ₱ 102,741,282.13 99,529,746.78

Cash in banks earns interest based on the prevailing bank deposit rates. Short-term

deposits are made for varying periods, depending on the LGU’s immediate cash

requirements, and earn interest at the respective short-term deposit rate.

17