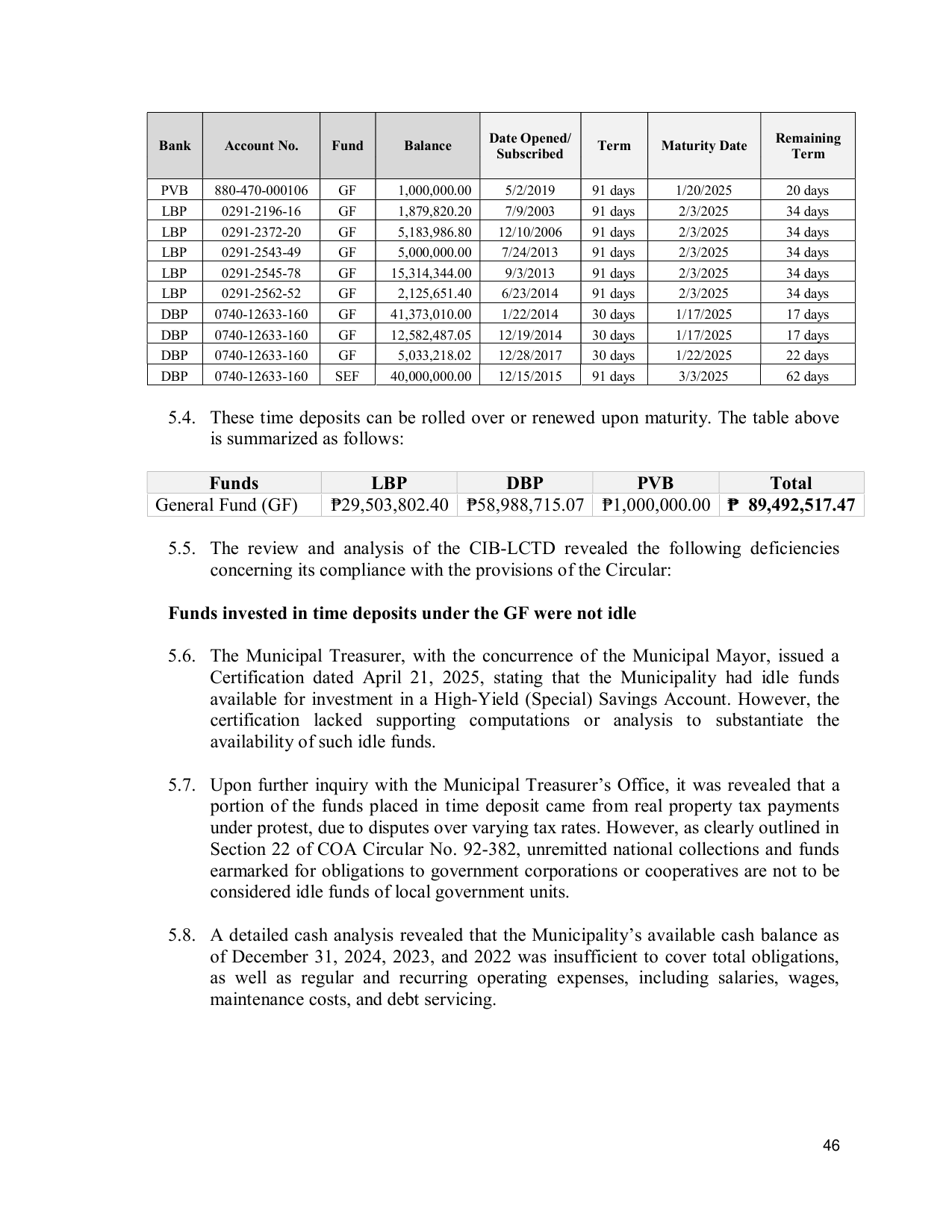

Date Opened/ Remaining

Bank Account No. Fund Balance Term Maturity Date

Subscribed Term

PVB 880-470-000106 GF 1,000,000.00 5/2/2019 91 days 1/20/2025 20 days

LBP 0291-2196-16 GF 1,879,820.20 7/9/2003 91 days 2/3/2025 34 days

LBP 0291-2372-20 GF 5,183,986.80 12/10/2006 91 days 2/3/2025 34 days

LBP 0291-2543-49 GF 5,000,000.00 7/24/2013 91 days 2/3/2025 34 days

LBP 0291-2545-78 GF 15,314,344.00 9/3/2013 91 days 2/3/2025 34 days

LBP 0291-2562-52 GF 2,125,651.40 6/23/2014 91 days 2/3/2025 34 days

DBP 0740-12633-160 GF 41,373,010.00 1/22/2014 30 days 1/17/2025 17 days

DBP 0740-12633-160 GF 12,582,487.05 12/19/2014 30 days 1/17/2025 17 days

DBP 0740-12633-160 GF 5,033,218.02 12/28/2017 30 days 1/22/2025 22 days

DBP 0740-12633-160 SEF 40,000,000.00 12/15/2015 91 days 3/3/2025 62 days

5.4. These time deposits can be rolled over or renewed upon maturity. The table above

is summarized as follows:

Funds LBP DBP PVB Total

General Fund (GF) ₱29,503,802.40 ₱58,988,715.07 ₱1,000,000.00 ₱ 89,492,517.47

5.5. The review and analysis of the CIB-LCTD revealed the following deficiencies

concerning its compliance with the provisions of the Circular:

Funds invested in time deposits under the GF were not idle

5.6. The Municipal Treasurer, with the concurrence of the Municipal Mayor, issued a

Certification dated April 21, 2025, stating that the Municipality had idle funds

available for investment in a High-Yield (Special) Savings Account. However, the

certification lacked supporting computations or analysis to substantiate the

availability of such idle funds.

5.7. Upon further inquiry with the Municipal Treasurer’s Office, it was revealed that a

portion of the funds placed in time deposit came from real property tax payments

under protest, due to disputes over varying tax rates. However, as clearly outlined in

Section 22 of COA Circular No. 92-382, unremitted national collections and funds

earmarked for obligations to government corporations or cooperatives are not to be

considered idle funds of local government units.

5.8. A detailed cash analysis revealed that the Municipality’s available cash balance as

of December 31, 2024, 2023, and 2022 was insufficient to cover total obligations,

as well as regular and recurring operating expenses, including salaries, wages,

maintenance costs, and debt servicing.

46