(c) Provide additional information that is not presented on the face

of the financial position, statement of financial performance,

statement of changes in net asset and equity, or cash flow

statement that is relevant to an understanding of any of them.”

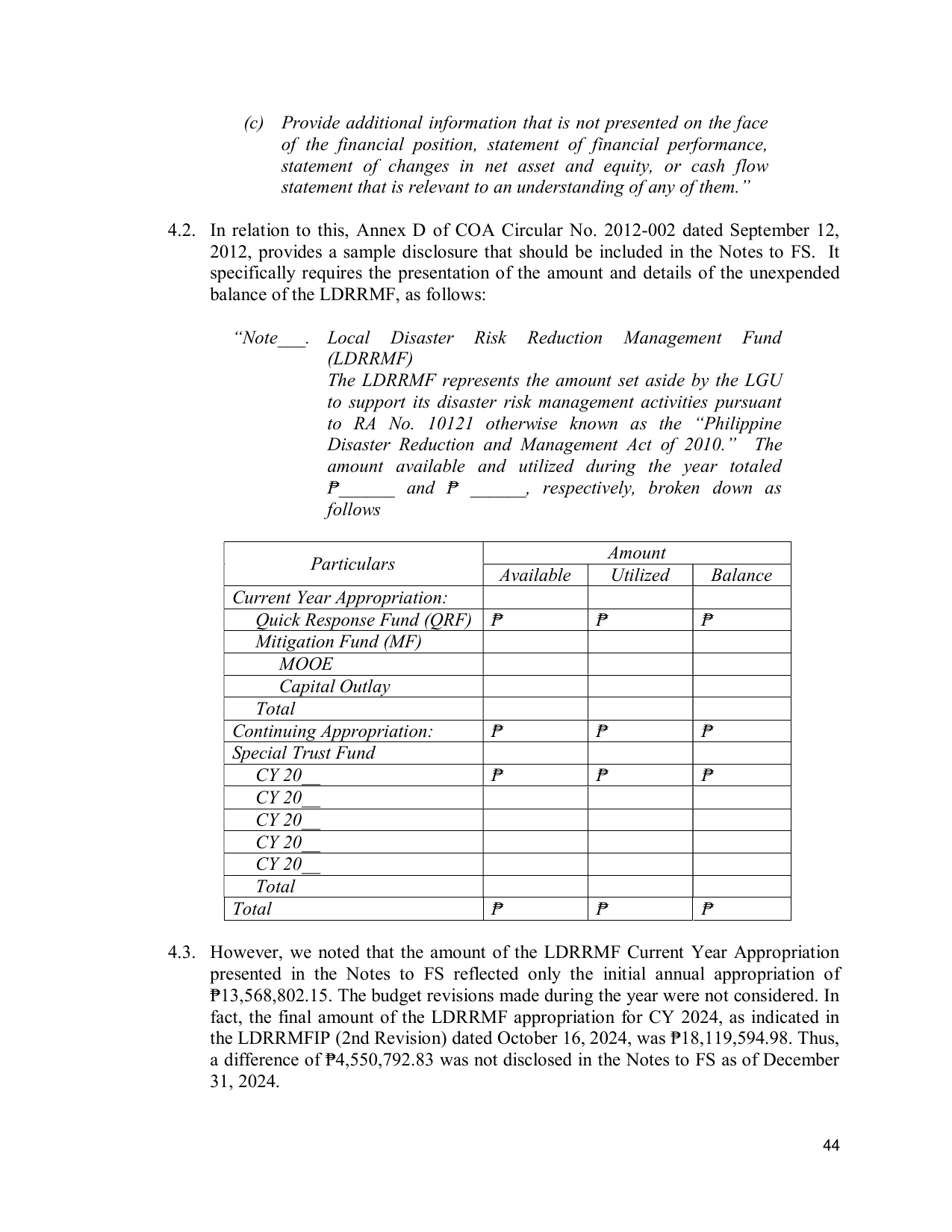

4.2. In relation to this, Annex D of COA Circular No. 2012-002 dated September 12,

2012, provides a sample disclosure that should be included in the Notes to FS. It

specifically requires the presentation of the amount and details of the unexpended

balance of the LDRRMF, as follows:

“Note___. Local Disaster Risk Reduction Management Fund

(LDRRMF)

The LDRRMF represents the amount set aside by the LGU

to support its disaster risk management activities pursuant

to RA No. 10121 otherwise known as the “Philippine

Disaster Reduction and Management Act of 2010.” The

amount available and utilized during the year totaled

₱______ and ₱ ______, respectively, broken down as

follows

Amount

Particulars

Available Utilized Balance

Current Year Appropriation:

Quick Response Fund (QRF) ₱ ₱ ₱

Mitigation Fund (MF)

MOOE

Capital Outlay

Total

Continuing Appropriation: ₱ ₱ ₱

Special Trust Fund

CY 20__ ₱ ₱ ₱

CY 20__

CY 20__

CY 20__

CY 20__

Total

Total ₱ ₱ ₱

4.3. However, we noted that the amount of the LDRRMF Current Year Appropriation

presented in the Notes to FS reflected only the initial annual appropriation of

₱13,568,802.15. The budget revisions made during the year were not considered. In

fact, the final amount of the LDRRMF appropriation for CY 2024, as indicated in

the LDRRMFIP (2nd Revision) dated October 16, 2024, was ₱18,119,594.98. Thus,

a difference of ₱4,550,792.83 was not disclosed in the Notes to FS as of December

31, 2024.

44