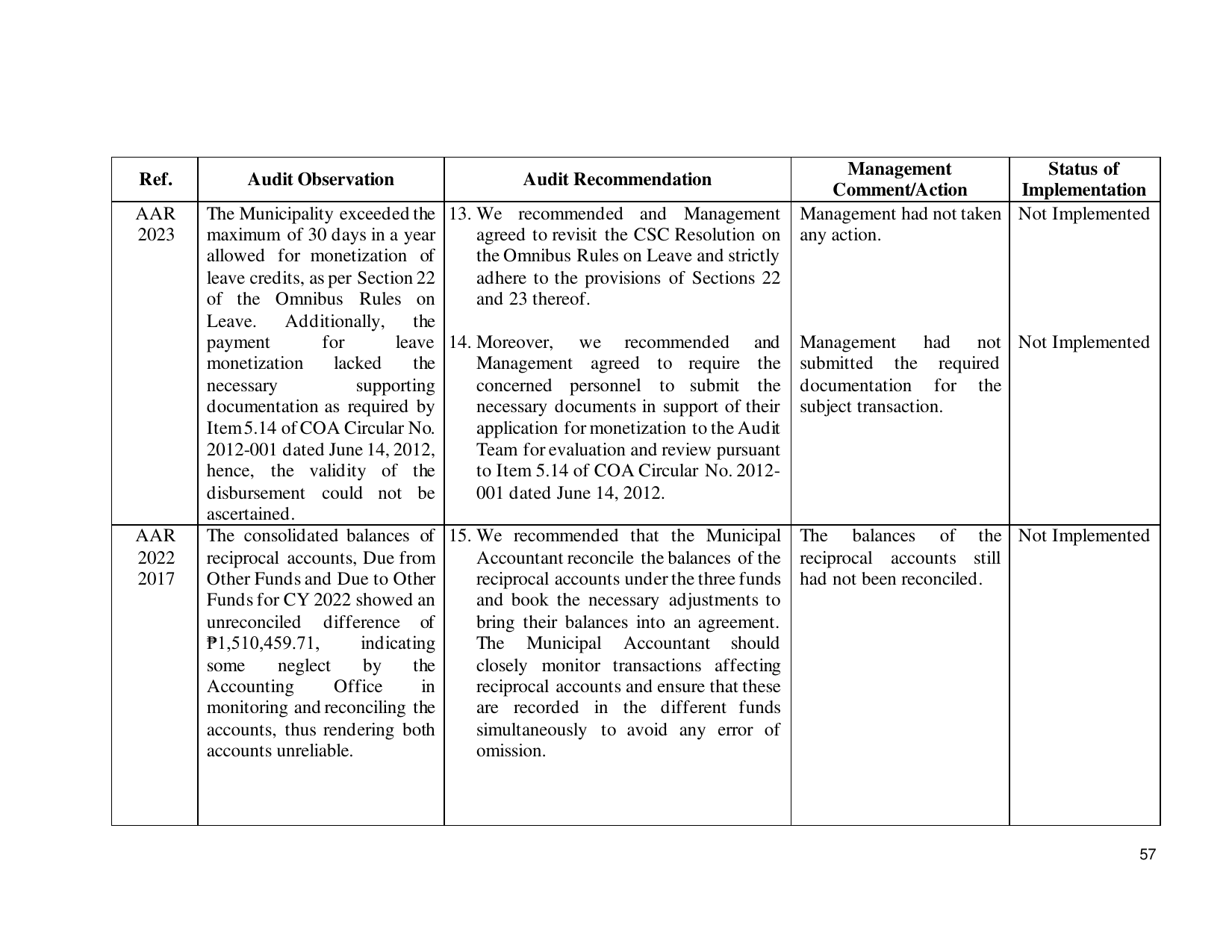

Management Status of

Ref. Audit Observation Audit Recommendation

Comment/Action Implementation

AAR The Municipality exceeded the 13. We recommended and Management Management had not taken Not Implemented

2023 maximum of 30 days in a year agreed to revisit the CSC Resolution on any action.

allowed for monetization of the Omnibus Rules on Leave and strictly

leave credits, as per Section 22 adhere to the provisions of Sections 22

of the Omnibus Rules on and 23 thereof.

Leave. Additionally, the

payment for leave 14. Moreover, we recommended and Management had not Not Implemented

monetization lacked the Management agreed to require the submitted the required

necessary supporting concerned personnel to submit the documentation for the

documentation as required by necessary documents in support of their subject transaction.

Item 5.14 of COA Circular No. application for monetization to the Audit

2012-001 dated June 14, 2012, Team for evaluation and review pursuant

hence, the validity of the to Item 5.14 of COA Circular No. 2012-

disbursement could not be 001 dated June 14, 2012.

ascertained.

AAR The consolidated balances of 15. We recommended that the Municipal The balances of the Not Implemented

2022 reciprocal accounts, Due from Accountant reconcile the balances of the reciprocal accounts still

2017 Other Funds and Due to Other reciprocal accounts under the three funds had not been reconciled.

Funds for CY 2022 showed an and book the necessary adjustments to

unreconciled difference of bring their balances into an agreement.

₱1,510,459.71, indicating The Municipal Accountant should

some neglect by the closely monitor transactions affecting

Accounting Office in reciprocal accounts and ensure that these

monitoring and reconciling the are recorded in the different funds

accounts, thus rendering both simultaneously to avoid any error of

accounts unreliable. omission.

57