6.9. We recommended and the LDRRMO agreed to:

6.9.1. Include PPAs that are chargeable against the prior years’ unexpended

LDRRMF in the annual LDRRMFIP of the current year, in accordance

with the format prescribed under Annex A of COA Circular No. 2012-

002; and

6.9.2. Establish an efficient review and monitoring system to ensure that the

LDRRMFIP complies with the requirements outlined in COA Circular

No. 2012-002.

C. OTHER MANDATORY AREAS

Compliance with Mandatory Deductions and Tax Laws

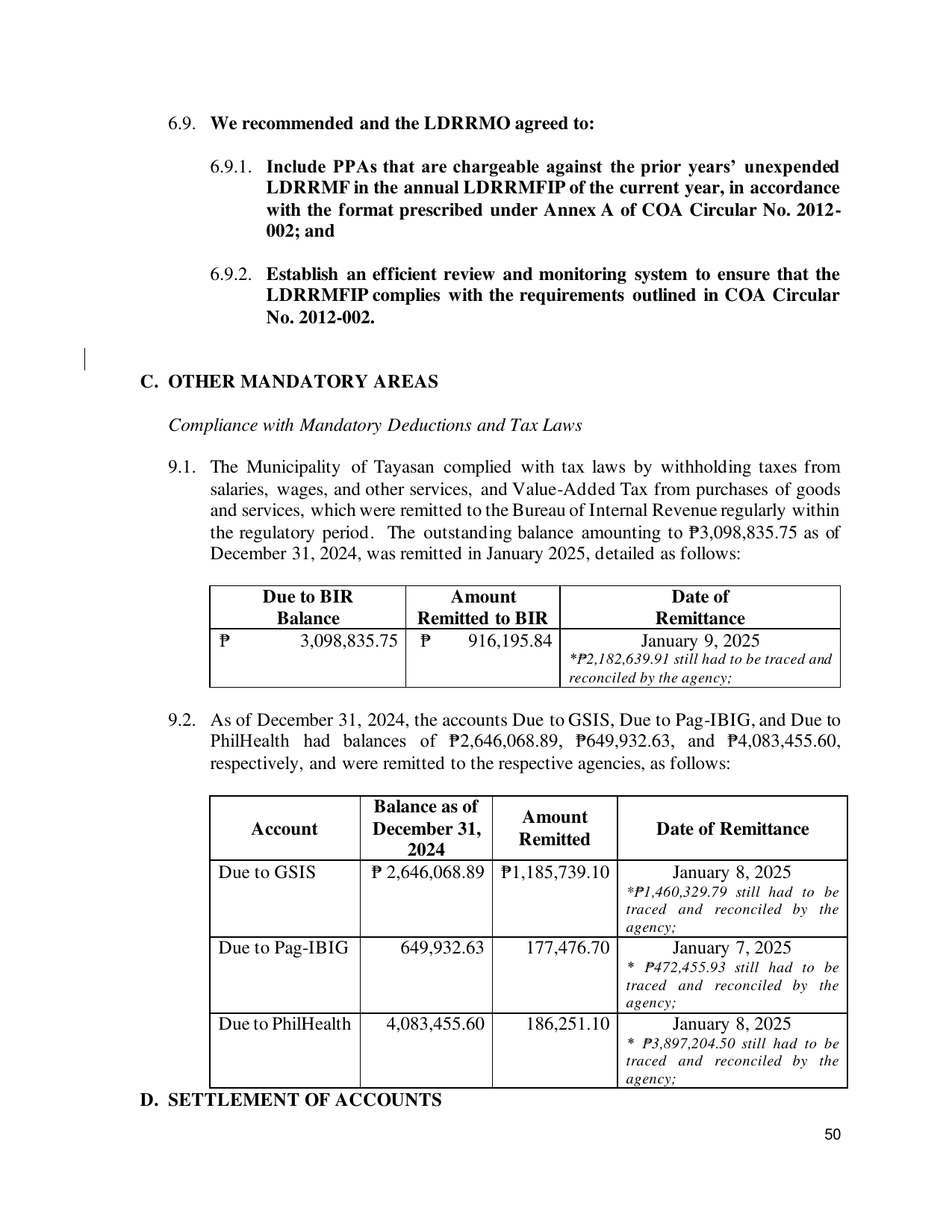

9.1. The Municipality of Tayasan complied with tax laws by withholding taxes from

salaries, wages, and other services, and Value-Added Tax from purchases of goods

and services, which were remitted to the Bureau of Internal Revenue regularly within

the regulatory period. The outstanding balance amounting to ₱3,098,835.75 as of

December 31, 2024, was remitted in January 2025, detailed as follows:

Due to BIR Amount Date of

Balance Remitted to BIR Remittance

₱ 3,098,835.75 ₱ 916,195.84 January 9, 2025

*₱2,182,639.91 still had to be traced and

reconciled by the agency;

9.2. As of December 31, 2024, the accounts Due to GSIS, Due to Pag-IBIG, and Due to

PhilHealth had balances of ₱2,646,068.89, ₱649,932.63, and ₱4,083,455.60,

respectively, and were remitted to the respective agencies, as follows:

Balance as of

Amount

Account December 31, Date of Remittance

Remitted

2024

Due to GSIS ₱ 2,646,068.89 ₱1,185,739.10 January 8, 2025

*₱1,460,329.79 still had to be

traced and reconciled by the

agency;

Due to Pag-IBIG 649,932.63 177,476.70 January 7, 2025

* ₱472,455.93 still had to be

traced and reconciled by the

agency;

Due to PhilHealth 4,083,455.60 186,251.10 January 8, 2025

* ₱3,897,204.50 still had to be

traced and reconciled by the

agency;

D. SETTLEMENT OF ACCOUNTS

50