Page 89 of 111

Status of

Ref Observation Recommendations Implementation/

Results of Validation

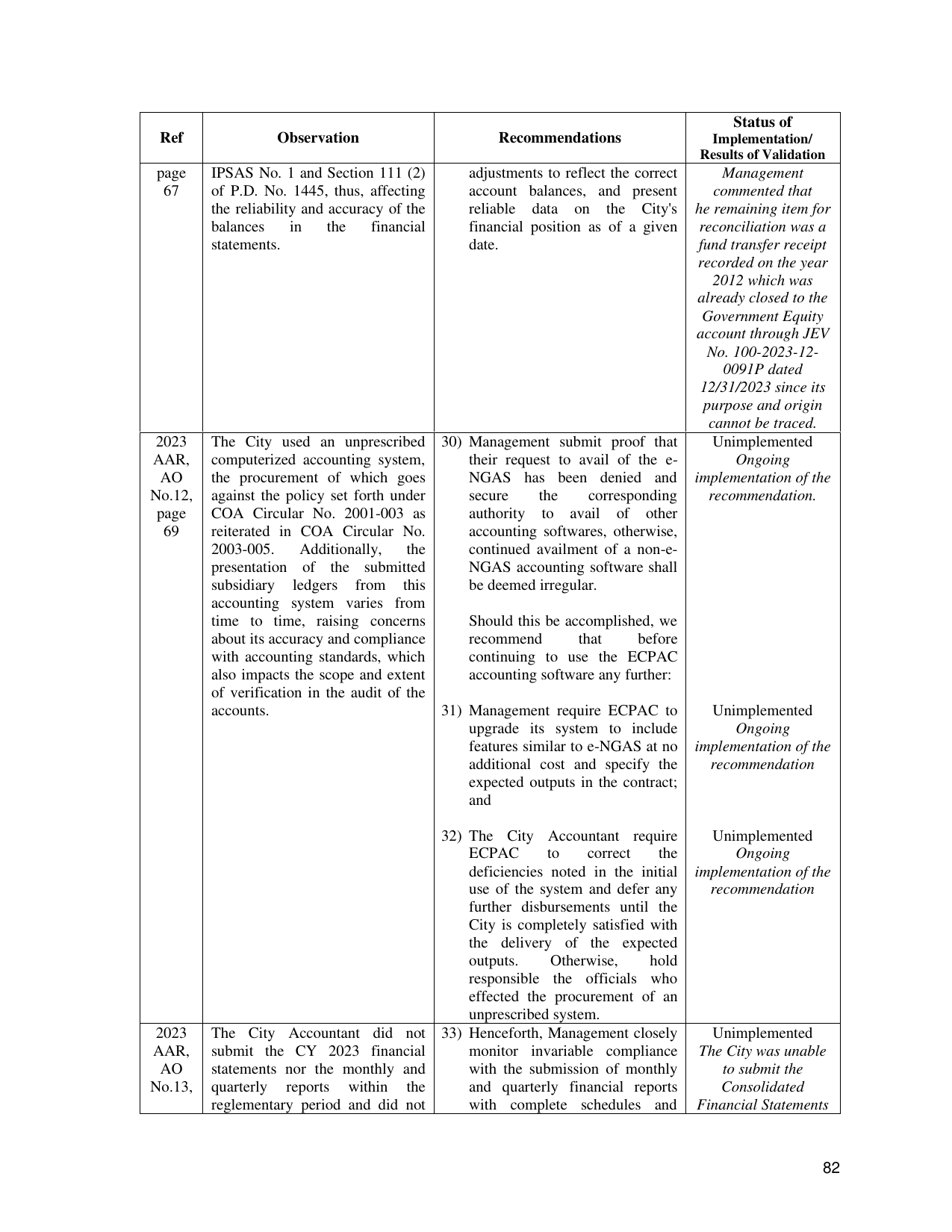

page IPSAS No. 1 and Section 111 (2) adjustments to reflect the correct Management

67 of P.D. No. 1445, thus, affecting account balances, and present commented that

the reliability and accuracy of the reliable data on the City's he remaining item for

balances in the financial financial position as of a given reconciliation was a

statements. date. fund transfer receipt

recorded on the year

2012 which was

already closed to the

Government Equity

account through JEV

No. 100-2023-12-

0091P dated

12/31/2023 since its

purpose and origin

cannot be traced.

2023 The City used an unprescribed 30) Management submit proof that Unimplemented

AAR, computerized accounting system, their request to avail of the e- Ongoing

AO the procurement of which goes NGAS has been denied and implementation of the

No.12, against the policy set forth under secure the corresponding recommendation.

page COA Circular No. 2001-003 as authority to avail of other

69 reiterated in COA Circular No. accounting softwares, otherwise,

2003-005. Additionally, the continued availment of a non-e-

presentation of the submitted NGAS accounting software shall

subsidiary ledgers from this be deemed irregular.

accounting system varies from

time to time, raising concerns Should this be accomplished, we

about its accuracy and compliance recommend that before

with accounting standards, which continuing to use the ECPAC

also impacts the scope and extent accounting software any further:

of verification in the audit of the

accounts. 31) Management require ECPAC to Unimplemented

upgrade its system to include Ongoing

features similar to e-NGAS at no implementation of the

additional cost and specify the recommendation

expected outputs in the contract;

and

32) The City Accountant require Unimplemented

ECPAC to correct the Ongoing

deficiencies noted in the initial implementation of the

use of the system and defer any recommendation

further disbursements until the

City is completely satisfied with

the delivery of the expected

outputs. Otherwise, hold

responsible the officials who

effected the procurement of an

unprescribed system.

2023 The City Accountant did not 33) Henceforth, Management closely Unimplemented

AAR, submit the CY 2023 financial monitor invariable compliance The City was unable

AO statements nor the monthly and with the submission of monthly to submit the

No.13, quarterly reports within the and quarterly financial reports Consolidated

reglementary period and did not with complete schedules and Financial Statements

82