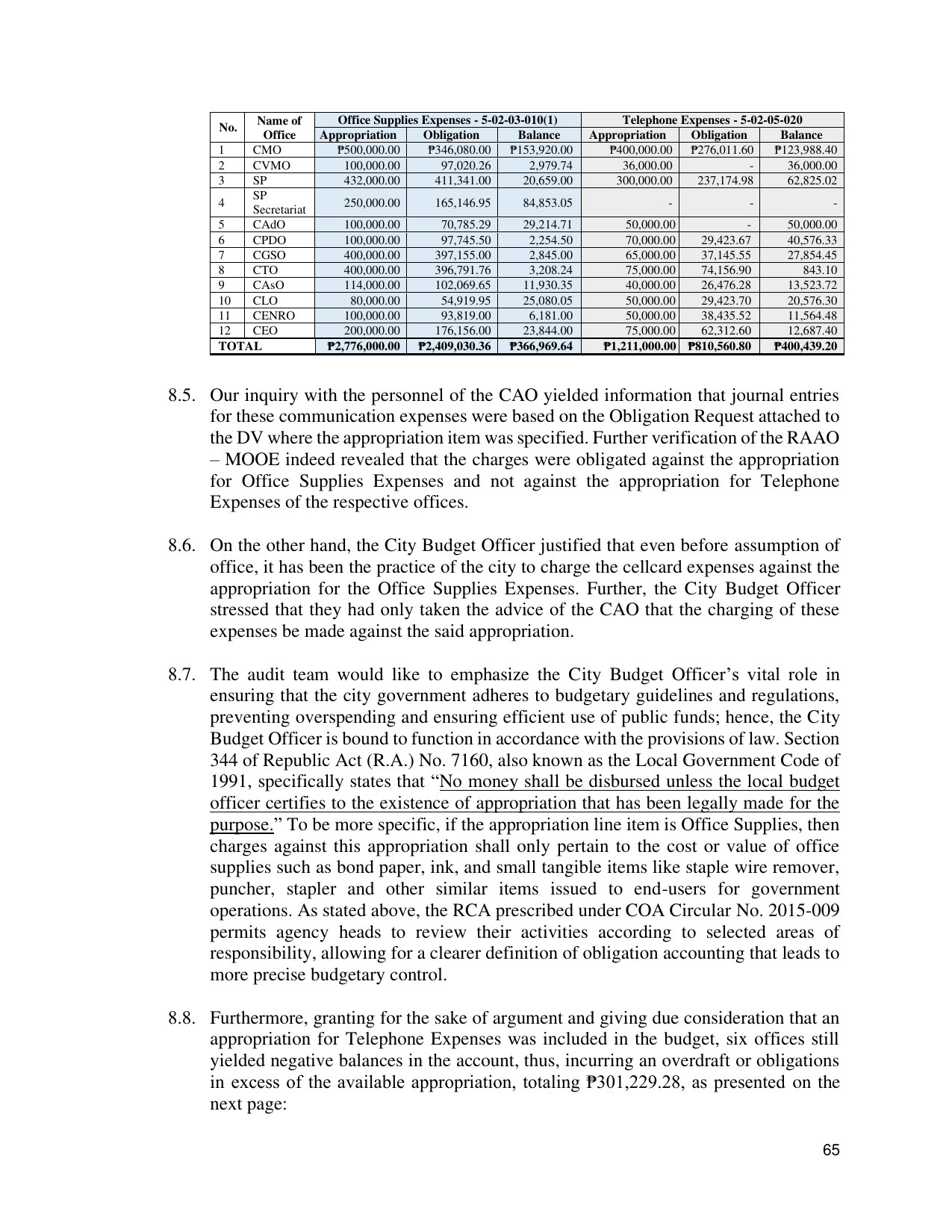

Name of Office Supplies Expenses - 5-02-03-010(1) Telephone Expenses - 5-02-05-020

No.

Office Appropriation Obligation Balance Appropriation Obligation Balance

1 CMO ₱500,000.00 ₱346,080.00 ₱153,920.00 ₱400,000.00 ₱276,011.60 ₱123,988.40

2 CVMO 100,000.00 97,020.26 2,979.74 36,000.00 - 36,000.00

3 SP 432,000.00 411,341.00 20,659.00 300,000.00 237,174.98 62,825.02

SP

4 250,000.00 165,146.95 84,853.05 - - -

Secretariat

5 CAdO 100,000.00 70,785.29 29,214.71 50,000.00 - 50,000.00

6 CPDO 100,000.00 97,745.50 2,254.50 70,000.00 29,423.67 40,576.33

7 CGSO 400,000.00 397,155.00 2,845.00 65,000.00 37,145.55 27,854.45

8 CTO 400,000.00 396,791.76 3,208.24 75,000.00 74,156.90 843.10

9 CAsO 114,000.00 102,069.65 11,930.35 40,000.00 26,476.28 13,523.72

10 CLO 80,000.00 54,919.95 25,080.05 50,000.00 29,423.70 20,576.30

11 CENRO 100,000.00 93,819.00 6,181.00 50,000.00 38,435.52 11,564.48

12 CEO 200,000.00 176,156.00 23,844.00 75,000.00 62,312.60 12,687.40

TOTAL ₱2,776,000.00 ₱2,409,030.36 ₱366,969.64 ₱1,211,000.00 ₱810,560.80 ₱400,439.20

8.5. Our inquiry with the personnel of the CAO yielded information that journal entries

for these communication expenses were based on the Obligation Request attached to

the DV where the appropriation item was specified. Further verification of the RAAO

– MOOE indeed revealed that the charges were obligated against the appropriation

for Office Supplies Expenses and not against the appropriation for Telephone

Expenses of the respective offices.

8.6. On the other hand, the City Budget Officer justified that even before assumption of

office, it has been the practice of the city to charge the cellcard expenses against the

appropriation for the Office Supplies Expenses. Further, the City Budget Officer

stressed that they had only taken the advice of the CAO that the charging of these

expenses be made against the said appropriation.

8.7. The audit team would like to emphasize the City Budget Officer’s vital role in

ensuring that the city government adheres to budgetary guidelines and regulations,

preventing overspending and ensuring efficient use of public funds; hence, the City

Budget Officer is bound to function in accordance with the provisions of law. Section

344 of Republic Act (R.A.) No. 7160, also known as the Local Government Code of

1991, specifically states that “No money shall be disbursed unless the local budget

officer certifies to the existence of appropriation that has been legally made for the

purpose.” To be more specific, if the appropriation line item is Office Supplies, then

charges against this appropriation shall only pertain to the cost or value of office

supplies such as bond paper, ink, and small tangible items like staple wire remover,

puncher, stapler and other similar items issued to end-users for government

operations. As stated above, the RCA prescribed under COA Circular No. 2015-009

permits agency heads to review their activities according to selected areas of

responsibility, allowing for a clearer definition of obligation accounting that leads to

more precise budgetary control.

8.8. Furthermore, granting for the sake of argument and giving due consideration that an

appropriation for Telephone Expenses was included in the budget, six offices still

yielded negative balances in the account, thus, incurring an overdraft or obligations

in excess of the available appropriation, totaling ₱301,229.28, as presented on the

next page:

65