c. Direct the Municipal Accountant to immediately coordinate with the

concerned Barangays to submit liquidation reports for the ₱420,000.00

fund transfers, and require compliance within a specified timeframe.

13.7 On June 2, 2025, copies of the MOAs and Approved Activity Design were

submitted to the Audit Team.

Long outstanding receivables from officers and employees

14. The Municipality did not enforce the timely collection of receivables from its officers

and employees, amounting to ₱108,336.22, which have been outstanding for up to

three years or more, indicating lapses in financial management and non-compliance

with Section 2 of PD No. 1445, thereby compromising the principles of efficiency,

economy, and effectiveness in government operations.

14.1 Section 2 of PD No. 1445 provides that it is the declared policy of the State that

all resources of the government shall be managed, expended or utilized in

accordance with law and regulations, and safeguard against loss or wastage

through illegal or improper disposition, with a view to ensuring efficiency,

economy and effectiveness in the operations of government. The responsibility to

take care that such policy is faithfully adhered to rests directly with the chief or

head of the government agency concerned.

14.2 COA Circular 2015-009 dated December 1, 2015, prescribes the Revised Chart of

Accounts for Local Government Units (LGUs). Annex B of the circular prescribes

that the account Due from Officers and Employees is debited for the amount of

claims from the agency’s officers and employees for overpayment, cash shortage,

loss of assets, and other bills issued by the agency. The account is credited for the

collection of the receivable.

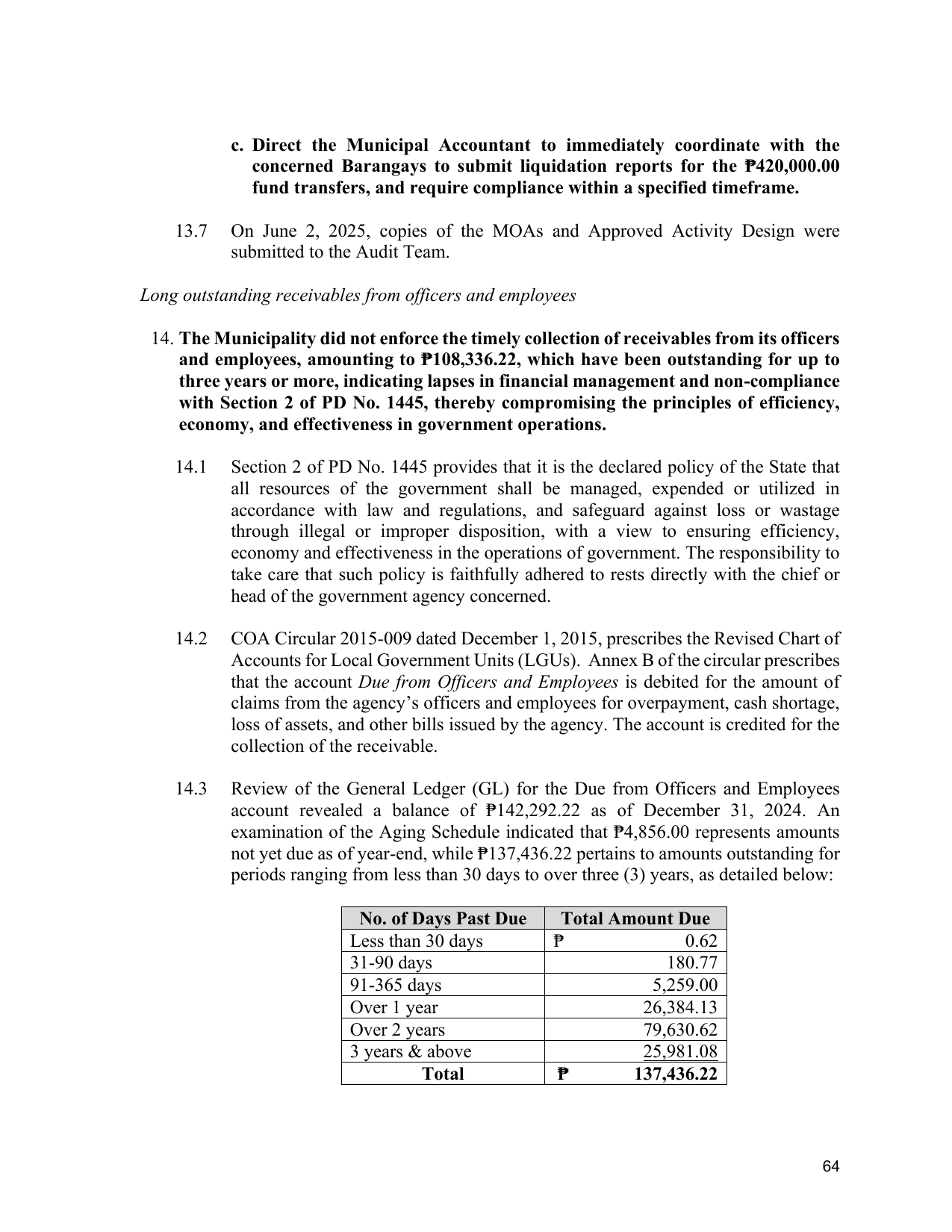

14.3 Review of the General Ledger (GL) for the Due from Officers and Employees

account revealed a balance of ₱142,292.22 as of December 31, 2024. An

examination of the Aging Schedule indicated that ₱4,856.00 represents amounts

not yet due as of year-end, while ₱137,436.22 pertains to amounts outstanding for

periods ranging from less than 30 days to over three (3) years, as detailed below:

No. of Days Past Due Total Amount Due

Less than 30 days ₱ 0.62

31-90 days 180.77

91-365 days 5,259.00

Over 1 year 26,384.13

Over 2 years 79,630.62

3 years & above 25,981.08

Total ₱ 137,436.22

64