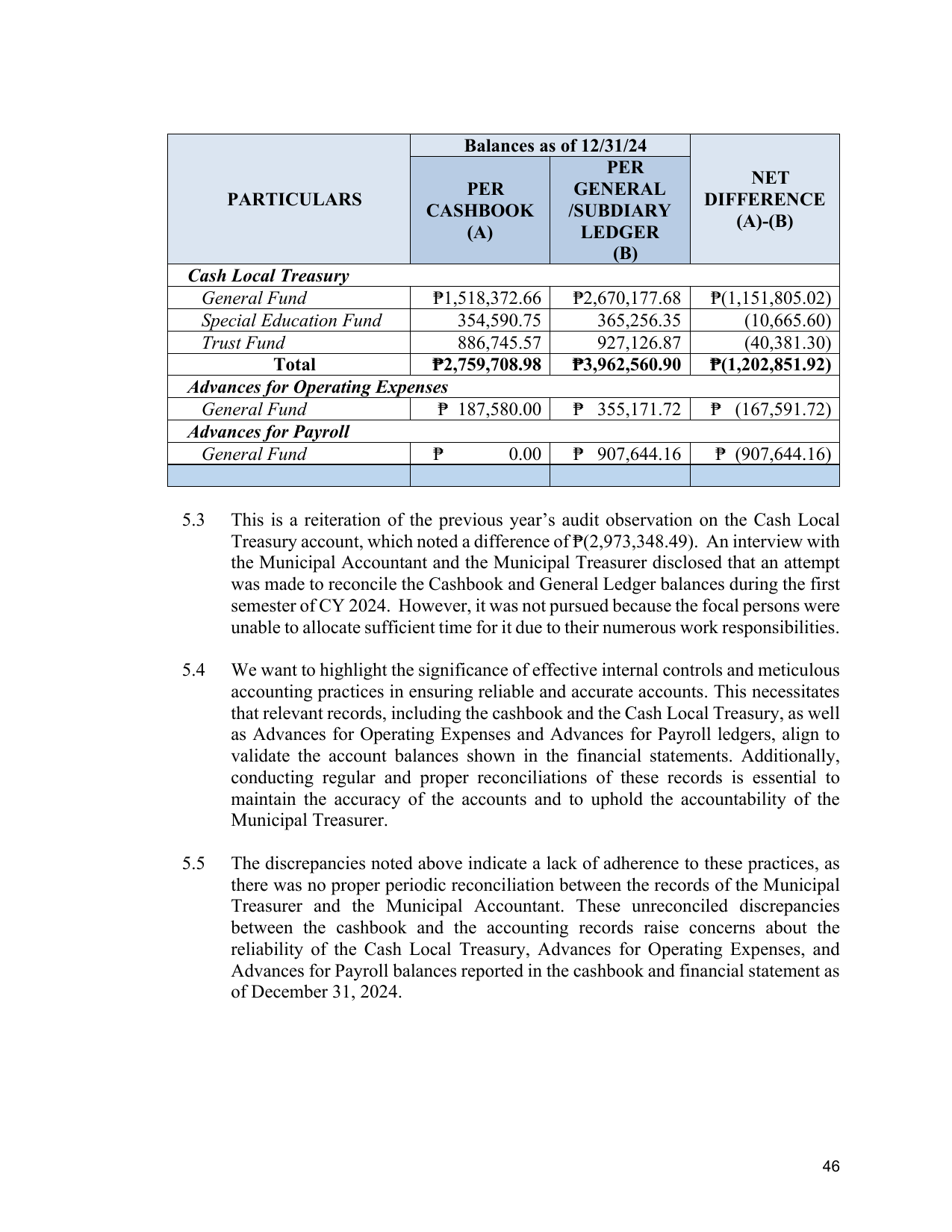

Balances as of 12/31/24

PER

NET

PER GENERAL

PARTICULARS DIFFERENCE

CASHBOOK /SUBDIARY

(A)-(B)

(A) LEDGER

(B)

Cash Local Treasury

General Fund ₱1,518,372.66 ₱2,670,177.68 ₱(1,151,805.02)

Special Education Fund 354,590.75 365,256.35 (10,665.60)

Trust Fund 886,745.57 927,126.87 (40,381.30)

Total ₱2,759,708.98 ₱3,962,560.90 ₱(1,202,851.92)

Advances for Operating Expenses

General Fund ₱ 187,580.00 ₱ 355,171.72 ₱ (167,591.72)

Advances for Payroll

General Fund ₱ 0.00 ₱ 907,644.16 ₱ (907,644.16)

5.3 This is a reiteration of the previous year’s audit observation on the Cash Local

Treasury account, which noted a difference of ₱(2,973,348.49). An interview with

the Municipal Accountant and the Municipal Treasurer disclosed that an attempt

was made to reconcile the Cashbook and General Ledger balances during the first

semester of CY 2024. However, it was not pursued because the focal persons were

unable to allocate sufficient time for it due to their numerous work responsibilities.

5.4 We want to highlight the significance of effective internal controls and meticulous

accounting practices in ensuring reliable and accurate accounts. This necessitates

that relevant records, including the cashbook and the Cash Local Treasury, as well

as Advances for Operating Expenses and Advances for Payroll ledgers, align to

validate the account balances shown in the financial statements. Additionally,

conducting regular and proper reconciliations of these records is essential to

maintain the accuracy of the accounts and to uphold the accountability of the

Municipal Treasurer.

5.5 The discrepancies noted above indicate a lack of adherence to these practices, as

there was no proper periodic reconciliation between the records of the Municipal

Treasurer and the Municipal Accountant. These unreconciled discrepancies

between the cashbook and the accounting records raise concerns about the

reliability of the Cash Local Treasury, Advances for Operating Expenses, and

Advances for Payroll balances reported in the cashbook and financial statement as

of December 31, 2024.

46