3.5 We recommended and the Municipal Accountant agreed to ensure that the

unexpended balance of the LDRRMF—QRF and MOOE of the MF is

properly recorded in the Trust Fund books at year-end to reflect accurate

financial reporting pursuant to COA Circular 2012-02 dated September 12,

2012.

3.6 We further recommended and the Municipal Accountant agreed to conduct

training sessions for accounting personnel to emphasize the importance of

timely and accurate journal entries related to LDRRMF transfers and

compliance with regulatory guidelines.

Non-recording of book reconciling items-

4. The Cash in Bank balances showed a discrepancy of ₱(3,068,540.08), net of

outstanding checks, compared to the confirmed balances from the depository bank,

which remained unadjusted because book reconciling items in the Bank

Reconciliation Statements (BRS) were not recorded during the year, inconsistent

with Sections 3.2 and 3.3 of COA Circular No. 96-011 dated October 2, 1996, thus

presenting an inaccurate and unreliable balance in the financial statements.

4.1 Sections 3.2 and 3.3 of COA Circular No. 96-011 dated October 2, 1996, state that

the Local Accountant shall reconcile the Bank Statements (BS) with the General

Ledgers (GL) within ten days of their receipt and prepare the BRS. He is also

required to issue journal vouchers to record all valid reconciling items that

necessitate adjustments and corrections in the GL.

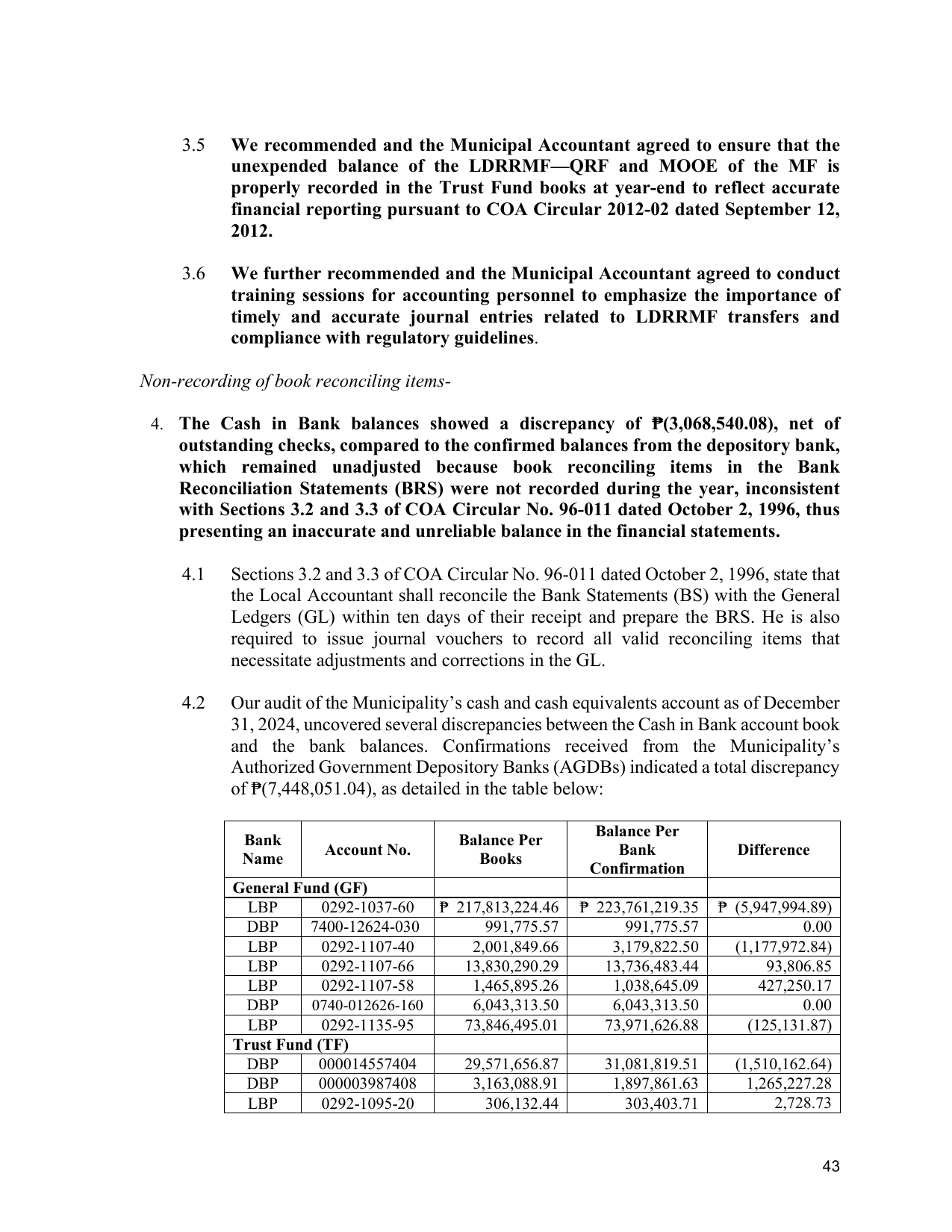

4.2 Our audit of the Municipality’s cash and cash equivalents account as of December

31, 2024, uncovered several discrepancies between the Cash in Bank account book

and the bank balances. Confirmations received from the Municipality’s

Authorized Government Depository Banks (AGDBs) indicated a total discrepancy

of ₱(7,448,051.04), as detailed in the table below:

Balance Per

Bank Balance Per

Account No. Bank Difference

Name Books

Confirmation

General Fund (GF)

LBP 0292-1037-60 ₱ 217,813,224.46 ₱ 223,761,219.35 ₱ (5,947,994.89)

DBP 7400-12624-030 991,775.57 991,775.57 0.00

LBP 0292-1107-40 2,001,849.66 3,179,822.50 (1,177,972.84)

LBP 0292-1107-66 13,830,290.29 13,736,483.44 93,806.85

LBP 0292-1107-58 1,465,895.26 1,038,645.09 427,250.17

DBP 0740-012626-160 6,043,313.50 6,043,313.50 0.00

LBP 0292-1135-95 73,846,495.01 73,971,626.88 (125,131.87)

Trust Fund (TF)

DBP 000014557404 29,571,656.87 31,081,819.51 (1,510,162.64)

DBP 000003987408 3,163,088.91 1,897,861.63 1,265,227.28

LBP 0292-1095-20 306,132.44 303,403.71 2,728.73

43