AUDIT OBSERVATIONS AND RECOMMENDATIONS

FINANCIAL AUDIT

Property, Plant, and Equipment (PPE)

1. The Local Government Unit did not take advantage of the guidelines and

procedures of COA Circular No. 2020-006 dated January 31, 2020 on the one-time

cleansing of Property, Plant and Equipment (PPE), thus affecting the fairness of

presentation of the financial position in the financial statements and depriving the

government of reliable and useful information in decision-making and

accountability for these assets.

1.1 COA Circular No. 2020-006 dated January 31, 2020 was issued to prescribe the

guidelines and procedures on inventory taking, recognition of those found at

station and disposition for missing PPE items for the one-time cleansing of PPE

accounts of government agencies to establish PPE balances that are verifiable as

to existence, condition and accountability.

1.2 Review of the compliance of the Agency with the said circular revealed that they

have not taken advantage of the various guidelines and procedures to cleanse their

PPE accounts balances as discussed below:

a. Non-conduct of a complete physical count of all its PPE

1.3 We interviewed the Municipal Treasurer and Municipal Accountant to inquire

about compliance with the requirement to conduct a physical count of all its PPE,

whether acquired through purchase or donation, including those constructed by

administration and found at the station. The Municipal Treasurer and Municipal

Accountant explained that the activity was not carried out because the Inventory

Committee was unable to mobilize due to a shortage of manpower and insufficient

time to fulfill its responsibilities.

b. Non-adoption of unique property number for each PPE and absence of property

stickers placed on each PPE.

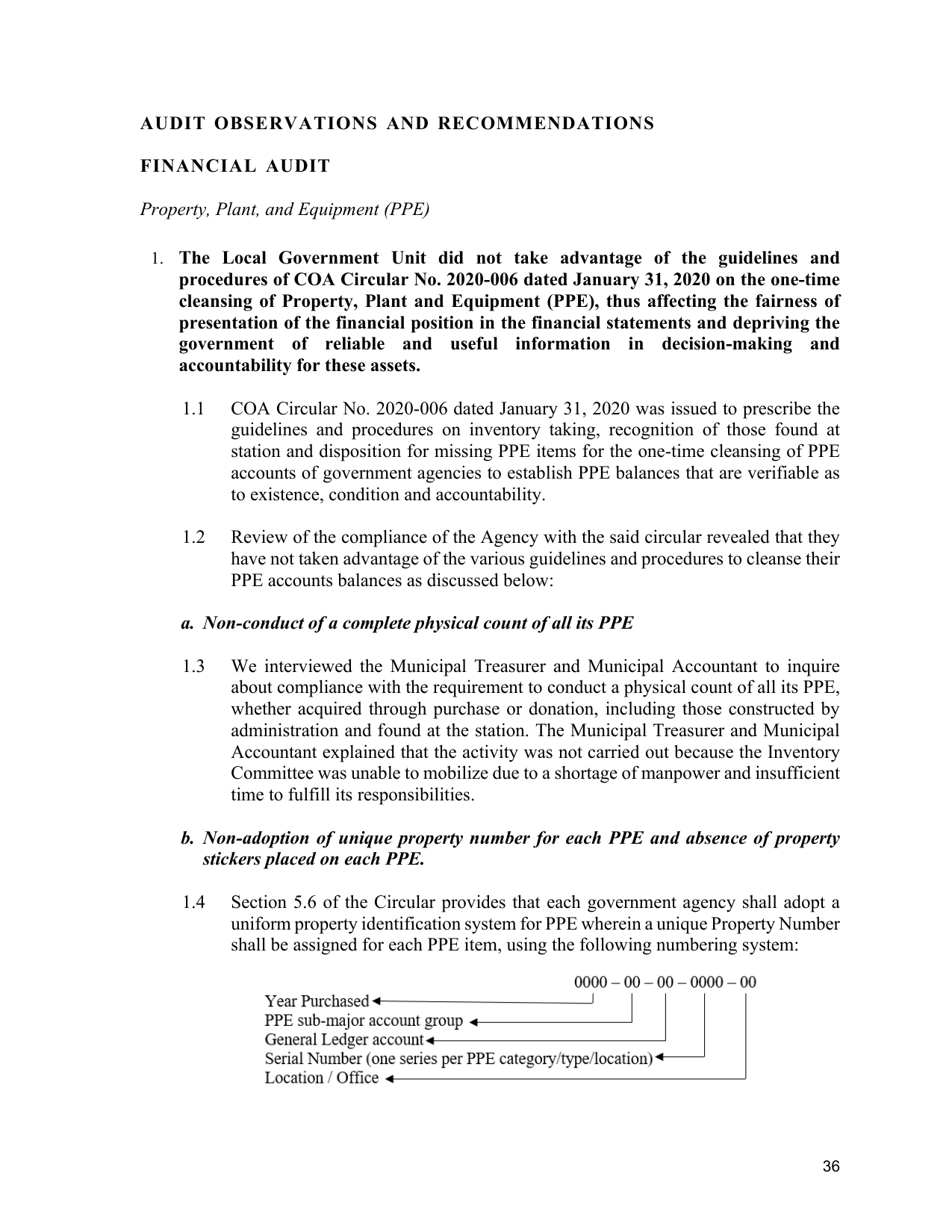

1.4 Section 5.6 of the Circular provides that each government agency shall adopt a

uniform property identification system for PPE wherein a unique Property Number

shall be assigned for each PPE item, using the following numbering system:

36