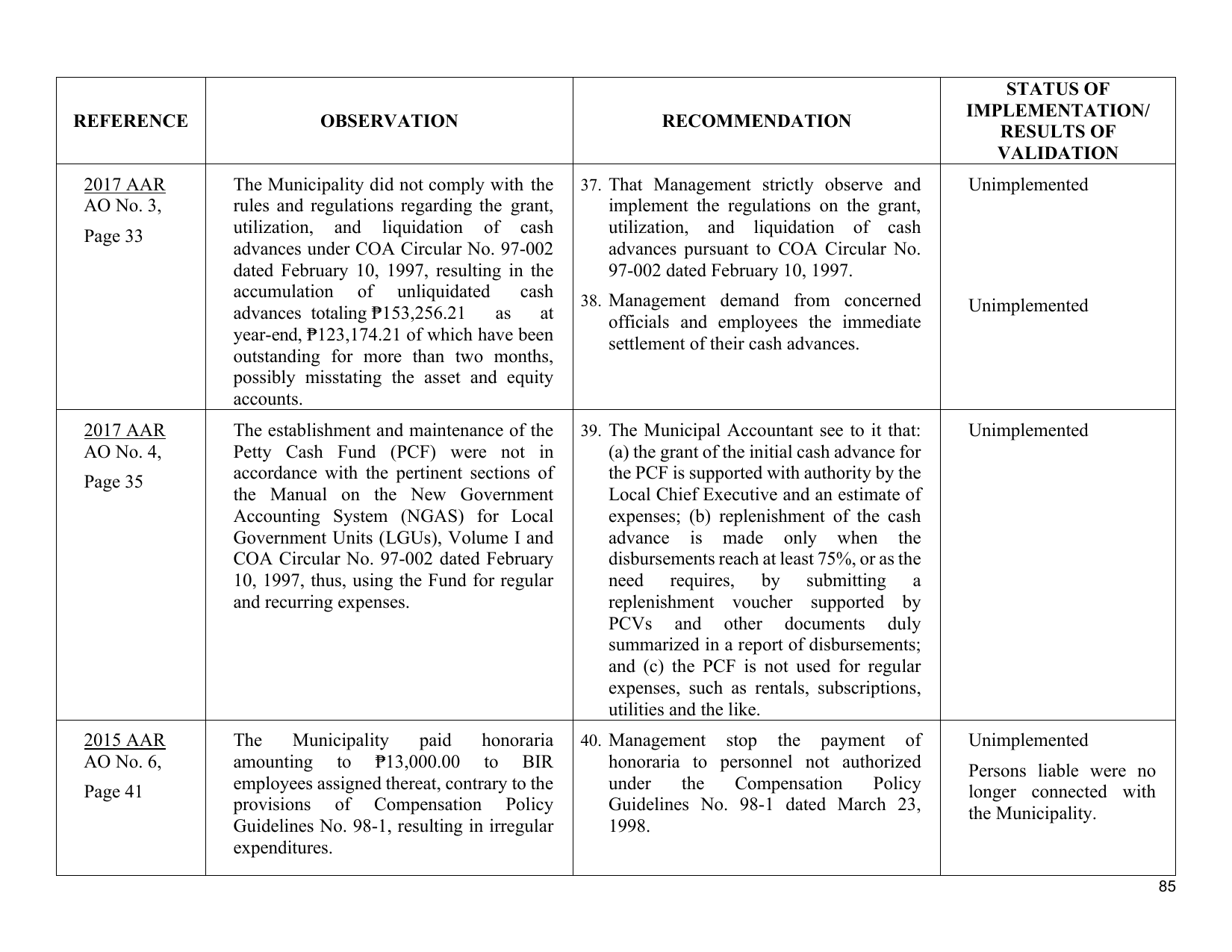

STATUS OF

IMPLEMENTATION/

REFERENCE OBSERVATION RECOMMENDATION

RESULTS OF

VALIDATION

2017 AAR The Municipality did not comply with the 37. That Management strictly observe and Unimplemented

AO No. 3, rules and regulations regarding the grant, implement the regulations on the grant,

Page 33 utilization, and liquidation of cash utilization, and liquidation of cash

advances under COA Circular No. 97-002 advances pursuant to COA Circular No.

dated February 10, 1997, resulting in the 97-002 dated February 10, 1997.

accumulation of unliquidated cash 38. Management demand from concerned

advances totaling ₱153,256.21 as at Unimplemented

officials and employees the immediate

year-end, ₱123,174.21 of which have been settlement of their cash advances.

outstanding for more than two months,

possibly misstating the asset and equity

accounts.

2017 AAR The establishment and maintenance of the 39. The Municipal Accountant see to it that: Unimplemented

AO No. 4, Petty Cash Fund (PCF) were not in (a) the grant of the initial cash advance for

Page 35 accordance with the pertinent sections of the PCF is supported with authority by the

the Manual on the New Government Local Chief Executive and an estimate of

Accounting System (NGAS) for Local expenses; (b) replenishment of the cash

Government Units (LGUs), Volume I and advance is made only when the

COA Circular No. 97-002 dated February disbursements reach at least 75%, or as the

10, 1997, thus, using the Fund for regular need requires, by submitting a

and recurring expenses. replenishment voucher supported by

PCVs and other documents duly

summarized in a report of disbursements;

and (c) the PCF is not used for regular

expenses, such as rentals, subscriptions,

utilities and the like.

2015 AAR The Municipality paid honoraria 40. Management stop the payment of Unimplemented

AO No. 6, amounting to ₱13,000.00 to BIR honoraria to personnel not authorized Persons liable were no

Page 41 employees assigned thereat, contrary to the under the Compensation Policy longer connected with

provisions of Compensation Policy Guidelines No. 98-1 dated March 23, the Municipality.

Guidelines No. 98-1, resulting in irregular 1998.

expenditures.

85