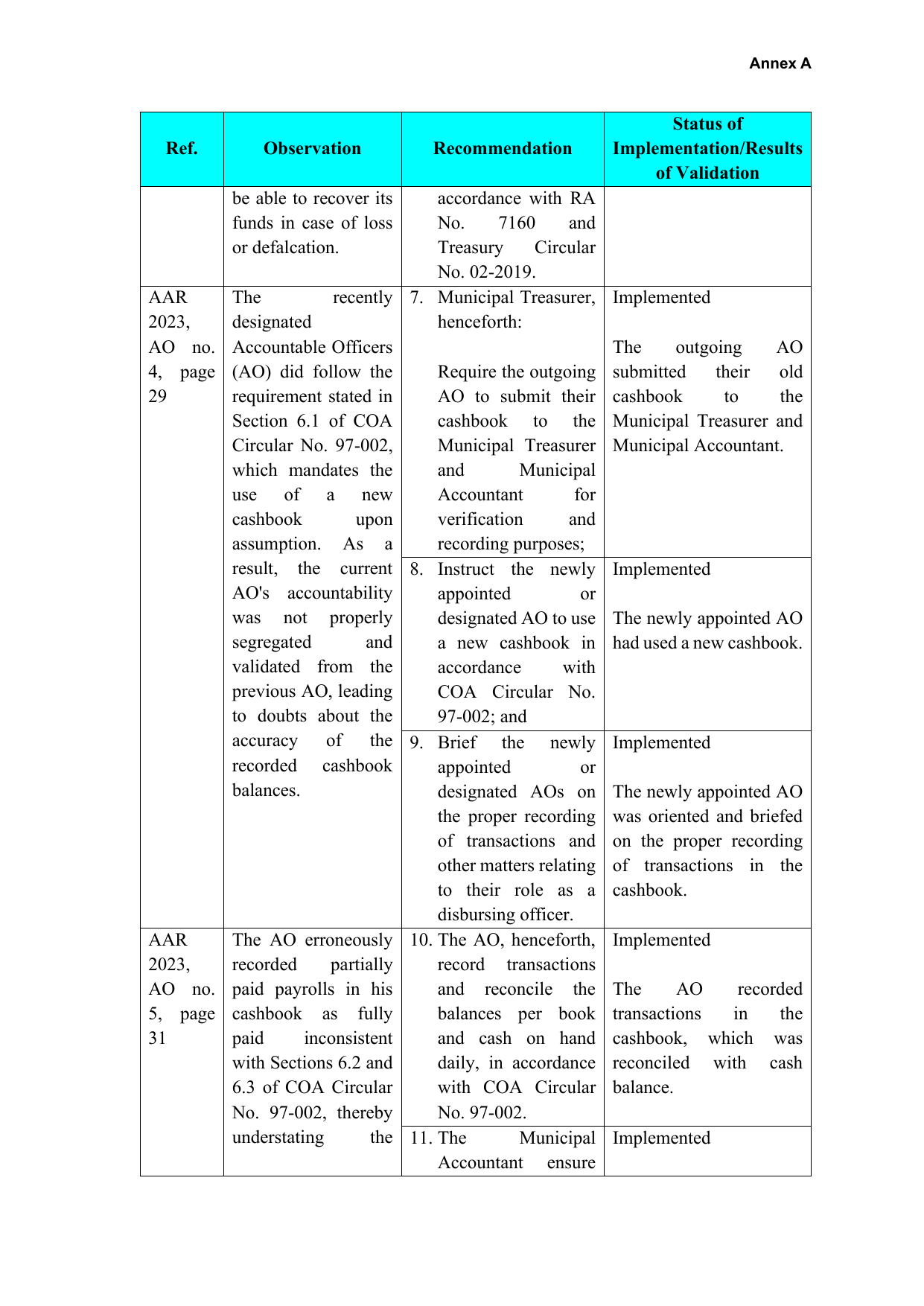

Annex A

Status of

Ref. Observation Recommendation Implementation/Results

of Validation

be able to recover its accordance with RA

funds in case of loss No. 7160 and

or defalcation. Treasury Circular

No. 02-2019.

AAR The recently 7. Municipal Treasurer, Implemented

2023, designated henceforth:

AO no. Accountable Officers The outgoing AO

4, page (AO) did follow the Require the outgoing submitted their old

29 requirement stated in AO to submit their cashbook to the

Section 6.1 of COA cashbook to the Municipal Treasurer and

Circular No. 97-002, Municipal Treasurer Municipal Accountant.

which mandates the and Municipal

use of a new Accountant for

cashbook upon verification and

assumption. As a recording purposes;

result, the current 8. Instruct the newly Implemented

AO's accountability appointed or

was not properly designated AO to use The newly appointed AO

segregated and a new cashbook in had used a new cashbook.

validated from the accordance with

previous AO, leading COA Circular No.

to doubts about the 97-002; and

accuracy of the 9. Brief the newly Implemented

recorded cashbook appointed or

balances. designated AOs on The newly appointed AO

the proper recording was oriented and briefed

of transactions and on the proper recording

other matters relating of transactions in the

to their role as a cashbook.

disbursing officer.

AAR The AO erroneously 10. The AO, henceforth, Implemented

2023, recorded partially record transactions

AO no. paid payrolls in his and reconcile the The AO recorded

5, page cashbook as fully balances per book transactions in the

31 paid inconsistent and cash on hand cashbook, which was

with Sections 6.2 and daily, in accordance reconciled with cash

6.3 of COA Circular with COA Circular balance.

No. 97-002, thereby No. 97-002.

understating the 11. The Municipal Implemented

Accountant ensure