18. The Municipal Accountant also explained that the operations of her office, along with

the Office of the Municipal Treasurer, were hindered by circumstances arising from

changes in the political setting within the Municipality during the audited year. There

were employees who were transferred and detailed, resulting in unfinished work and

responsibilities, which were directly linked to the accomplishment of transaction

documents and reports necessary for the recording of accounts and preparation of the

financial statements.

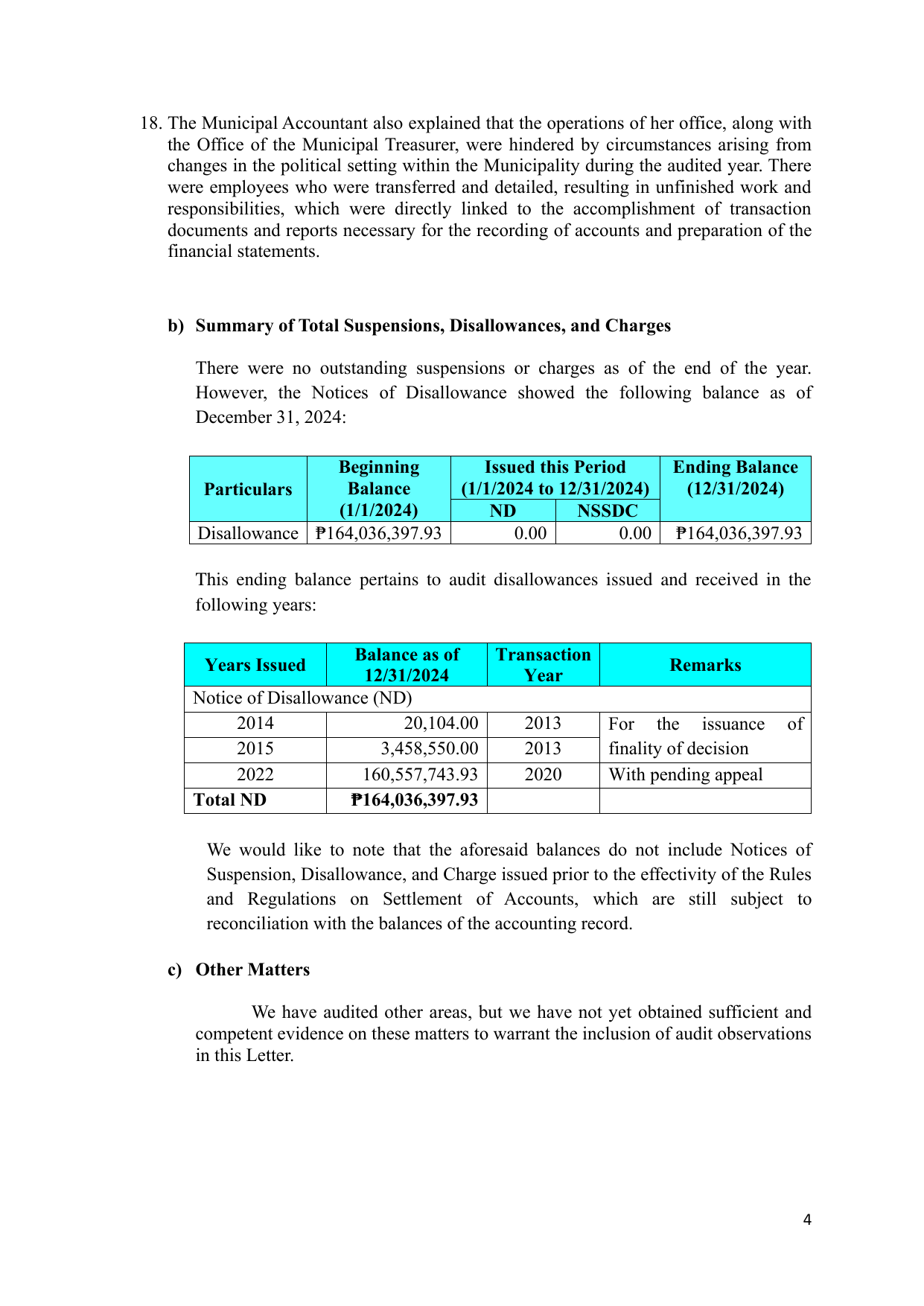

b) Summary of Total Suspensions, Disallowances, and Charges

There were no outstanding suspensions or charges as of the end of the year.

However, the Notices of Disallowance showed the following balance as of

December 31, 2024:

Beginning Issued this Period Ending Balance

Particulars Balance (1/1/2024 to 12/31/2024) (12/31/2024)

(1/1/2024) ND NSSDC

Disallowance ₱164,036,397.93 0.00 0.00 ₱164,036,397.93

This ending balance pertains to audit disallowances issued and received in the

following years:

Balance as of Transaction

Years Issued Remarks

12/31/2024 Year

Notice of Disallowance (ND)

2014 20,104.00 2013 For the issuance of

2015 3,458,550.00 2013 finality of decision

2022 160,557,743.93 2020 With pending appeal

Total ND ₱164,036,397.93

We would like to note that the aforesaid balances do not include Notices of

Suspension, Disallowance, and Charge issued prior to the effectivity of the Rules

and Regulations on Settlement of Accounts, which are still subject to

reconciliation with the balances of the accounting record.

c) Other Matters

We have audited other areas, but we have not yet obtained sufficient and

competent evidence on these matters to warrant the inclusion of audit observations

in this Letter.

4