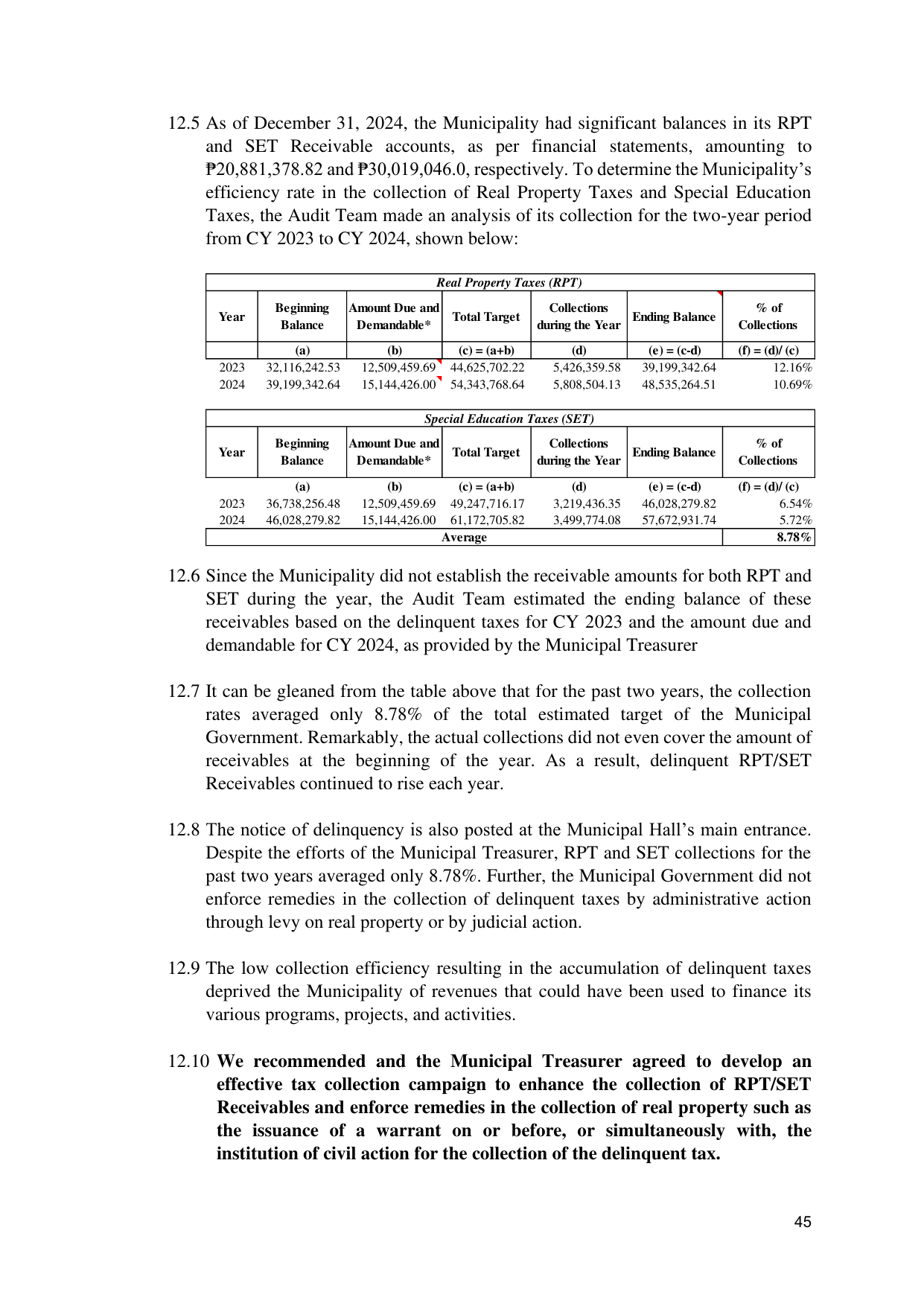

12.5 As of December 31, 2024, the Municipality had significant balances in its RPT

and SET Receivable accounts, as per financial statements, amounting to

₱20,881,378.82 and ₱30,019,046.0, respectively. To determine the Municipality’s

efficiency rate in the collection of Real Property Taxes and Special Education

Taxes, the Audit Team made an analysis of its collection for the two-year period

from CY 2023 to CY 2024, shown below:

Real Property Taxes (RPT)

Beginning Amount Due and Collections % of

Year Total Target Ending Balance

Balance Demandable* during the Year Collections

(a) (b) (c) = (a+b) (d) (e) = (c-d) (f) = (d)/ (c)

2023 32,116,242.53 12,509,459.69 44,625,702.22 5,426,359.58 39,199,342.64 12.16%

2024 39,199,342.64 15,144,426.00 54,343,768.64 5,808,504.13 48,535,264.51 10.69%

Special Education Taxes (SET)

Beginning Amount Due and Collections % of

Year Total Target Ending Balance

Balance Demandable* during the Year Collections

(a) (b) (c) = (a+b) (d) (e) = (c-d) (f) = (d)/ (c)

2023 36,738,256.48 12,509,459.69 49,247,716.17 3,219,436.35 46,028,279.82 6.54%

2024 46,028,279.82 15,144,426.00 61,172,705.82 3,499,774.08 57,672,931.74 5.72%

Average 8.78%

12.6 Since the Municipality did not establish the receivable amounts for both RPT and

SET during the year, the Audit Team estimated the ending balance of these

receivables based on the delinquent taxes for CY 2023 and the amount due and

demandable for CY 2024, as provided by the Municipal Treasurer

12.7 It can be gleaned from the table above that for the past two years, the collection

rates averaged only 8.78% of the total estimated target of the Municipal

Government. Remarkably, the actual collections did not even cover the amount of

receivables at the beginning of the year. As a result, delinquent RPT/SET

Receivables continued to rise each year.

12.8 The notice of delinquency is also posted at the Municipal Hall’s main entrance.

Despite the efforts of the Municipal Treasurer, RPT and SET collections for the

past two years averaged only 8.78%. Further, the Municipal Government did not

enforce remedies in the collection of delinquent taxes by administrative action

through levy on real property or by judicial action.

12.9 The low collection efficiency resulting in the accumulation of delinquent taxes

deprived the Municipality of revenues that could have been used to finance its

various programs, projects, and activities.

12.10 We recommended and the Municipal Treasurer agreed to develop an

effective tax collection campaign to enhance the collection of RPT/SET

Receivables and enforce remedies in the collection of real property such as

the issuance of a warrant on or before, or simultaneously with, the

institution of civil action for the collection of the delinquent tax.

45