were deposited into the General Fund bank account of the Municipal Government,

rather than a separate bank account designated for this specific purpose.

10.5 Thus, the total cash balance in the bank account includes not only those for GF

Proper but also funds under the 20 percent DF, which is composed of its current

appropriations amounting to ₱77,937,148.56 and continuing appropriations

amounting to ₱183,583,707.73, or a total of ₱261,520,856.29, as reported in the

Status of Appropriations, Allotments, and Obligations (SAAOB) as of December

31, 2024.

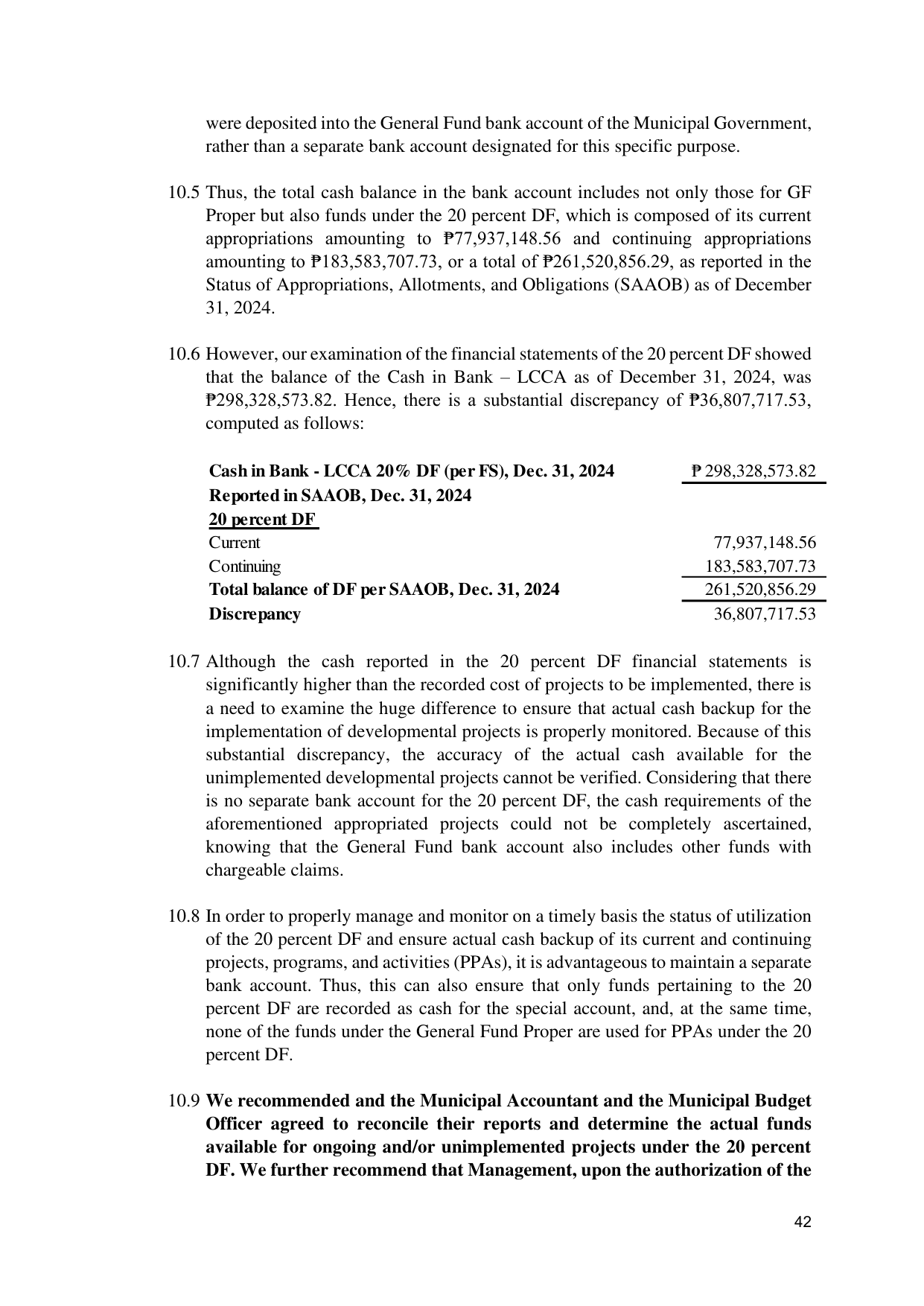

10.6 However, our examination of the financial statements of the 20 percent DF showed

that the balance of the Cash in Bank – LCCA as of December 31, 2024, was

₱298,328,573.82. Hence, there is a substantial discrepancy of ₱36,807,717.53,

computed as follows:

Cash in Bank - LCCA 20% DF (per FS), Dec. 31, 2024 ₱ 298,328,573.82

Reported in SAAOB, Dec. 31, 2024

20 percent DF

Current 77,937,148.56

Continuing 183,583,707.73

Total balance of DF per SAAOB, Dec. 31, 2024 261,520,856.29

Discrepancy 36,807,717.53

10.7 Although the cash reported in the 20 percent DF financial statements is

significantly higher than the recorded cost of projects to be implemented, there is

a need to examine the huge difference to ensure that actual cash backup for the

implementation of developmental projects is properly monitored. Because of this

substantial discrepancy, the accuracy of the actual cash available for the

unimplemented developmental projects cannot be verified. Considering that there

is no separate bank account for the 20 percent DF, the cash requirements of the

aforementioned appropriated projects could not be completely ascertained,

knowing that the General Fund bank account also includes other funds with

chargeable claims.

10.8 In order to properly manage and monitor on a timely basis the status of utilization

of the 20 percent DF and ensure actual cash backup of its current and continuing

projects, programs, and activities (PPAs), it is advantageous to maintain a separate

bank account. Thus, this can also ensure that only funds pertaining to the 20

percent DF are recorded as cash for the special account, and, at the same time,

none of the funds under the General Fund Proper are used for PPAs under the 20

percent DF.

10.9 We recommended and the Municipal Accountant and the Municipal Budget

Officer agreed to reconcile their reports and determine the actual funds

available for ongoing and/or unimplemented projects under the 20 percent

DF. We further recommend that Management, upon the authorization of the

42