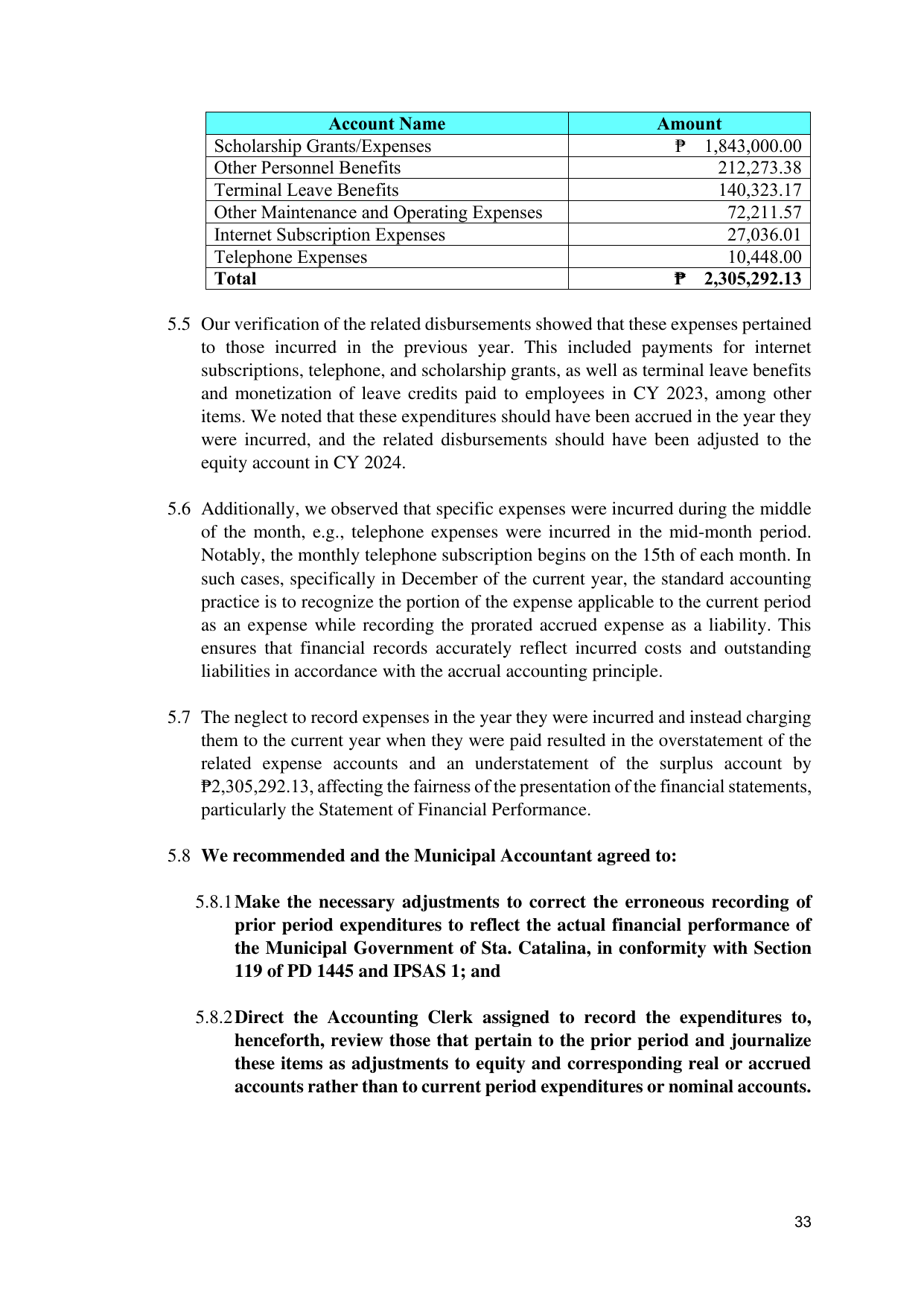

Account Name Amount

Scholarship Grants/Expenses ₱ 1,843,000.00

Other Personnel Benefits 212,273.38

Terminal Leave Benefits 140,323.17

Other Maintenance and Operating Expenses 72,211.57

Internet Subscription Expenses 27,036.01

Telephone Expenses 10,448.00

Total ₱ 2,305,292.13

5.5 Our verification of the related disbursements showed that these expenses pertained

to those incurred in the previous year. This included payments for internet

subscriptions, telephone, and scholarship grants, as well as terminal leave benefits

and monetization of leave credits paid to employees in CY 2023, among other

items. We noted that these expenditures should have been accrued in the year they

were incurred, and the related disbursements should have been adjusted to the

equity account in CY 2024.

5.6 Additionally, we observed that specific expenses were incurred during the middle

of the month, e.g., telephone expenses were incurred in the mid-month period.

Notably, the monthly telephone subscription begins on the 15th of each month. In

such cases, specifically in December of the current year, the standard accounting

practice is to recognize the portion of the expense applicable to the current period

as an expense while recording the prorated accrued expense as a liability. This

ensures that financial records accurately reflect incurred costs and outstanding

liabilities in accordance with the accrual accounting principle.

5.7 The neglect to record expenses in the year they were incurred and instead charging

them to the current year when they were paid resulted in the overstatement of the

related expense accounts and an understatement of the surplus account by

₱2,305,292.13, affecting the fairness of the presentation of the financial statements,

particularly the Statement of Financial Performance.

5.8 We recommended and the Municipal Accountant agreed to:

5.8.1 Make the necessary adjustments to correct the erroneous recording of

prior period expenditures to reflect the actual financial performance of

the Municipal Government of Sta. Catalina, in conformity with Section

119 of PD 1445 and IPSAS 1; and

5.8.2 Direct the Accounting Clerk assigned to record the expenditures to,

henceforth, review those that pertain to the prior period and journalize

these items as adjustments to equity and corresponding real or accrued

accounts rather than to current period expenditures or nominal accounts.

33