supported by detailed records for each item. Regular purchases shall be recorded

through the inventory account, and issuances recognized as they occur. However,

purchases made from the petty cash fund for immediate use or stock shall be

directly charged to the appropriate expense accounts.

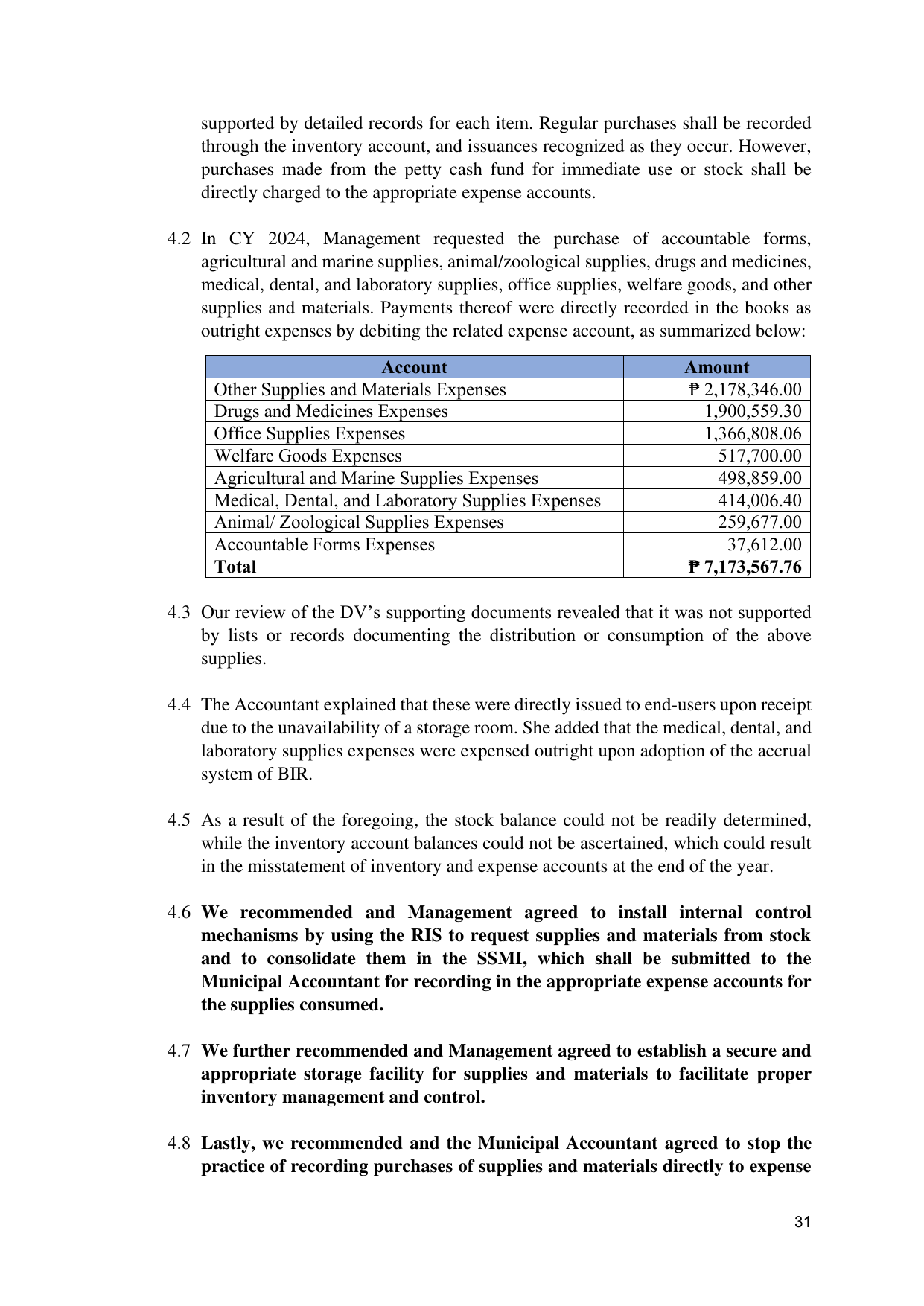

4.2 In CY 2024, Management requested the purchase of accountable forms,

agricultural and marine supplies, animal/zoological supplies, drugs and medicines,

medical, dental, and laboratory supplies, office supplies, welfare goods, and other

supplies and materials. Payments thereof were directly recorded in the books as

outright expenses by debiting the related expense account, as summarized below:

Account Amount

Other Supplies and Materials Expenses ₱ 2,178,346.00

Drugs and Medicines Expenses 1,900,559.30

Office Supplies Expenses 1,366,808.06

Welfare Goods Expenses 517,700.00

Agricultural and Marine Supplies Expenses 498,859.00

Medical, Dental, and Laboratory Supplies Expenses 414,006.40

Animal/ Zoological Supplies Expenses 259,677.00

Accountable Forms Expenses 37,612.00

Total ₱ 7,173,567.76

4.3 Our review of the DV’s supporting documents revealed that it was not supported

by lists or records documenting the distribution or consumption of the above

supplies.

4.4 The Accountant explained that these were directly issued to end-users upon receipt

due to the unavailability of a storage room. She added that the medical, dental, and

laboratory supplies expenses were expensed outright upon adoption of the accrual

system of BIR.

4.5 As a result of the foregoing, the stock balance could not be readily determined,

while the inventory account balances could not be ascertained, which could result

in the misstatement of inventory and expense accounts at the end of the year.

4.6 We recommended and Management agreed to install internal control

mechanisms by using the RIS to request supplies and materials from stock

and to consolidate them in the SSMI, which shall be submitted to the

Municipal Accountant for recording in the appropriate expense accounts for

the supplies consumed.

4.7 We further recommended and Management agreed to establish a secure and

appropriate storage facility for supplies and materials to facilitate proper

inventory management and control.

4.8 Lastly, we recommended and the Municipal Accountant agreed to stop the

practice of recording purchases of supplies and materials directly to expense

31