FINANCIAL AUDIT

Unreconciled amount due per Certified List of Taxpayers and RPT and SET Receivables -

₱22,098,576.94

1. Due to the delayed submission of the Certified List of Taxpayers and Amounts

Due and Collectible for the Year by the Municipal Treasurer to the Municipal

Accountant, as mandated by Section 20 of the NGAS Manual, Volume I for LGUs,

along with the lack of coordination between the two offices regarding the effects

of the Real Property Valuation and Assessment Reform Act on the delinquencies

of the Certified List, the balances of the RPT and SET receivables are overstated

by ₱22,098,576.94 as of December 31, 2024.

1.1 Sec. 111(2) of PD No. 1445, also known as the “Government Auditing Code of

the Philippines,” mandates that the highest standards of honesty, objectivity, and

consistency shall be observed in the keeping of accounts to safeguard against

inaccurate or misleading information.

1.2 Section 20 of the Manual on the New Government Accounting System (NGAS),

Volume I for Local Government Units (LGUs) requires the RPT and SET

receivables to be established by the Municipal Accountant at the beginning of the

year, based on the Real Property Tax Account Register or the Taxpayer’s index

card. Thus, the Municipal Treasurer must provide the Municipal Accountant with

a duly certified list showing the name of taxpayers and the amount due and

collectible for the period. Based on this list, the Municipal Accountant shall

prepare a JEV to record the debit to RPT Receivable/SET Receivable and credit

the corresponding Deferred RPT Income/SET Income. Upon collection of RPT

from taxpayers, the account Deferred RPT Income/SET Income shall be debited,

while the RPT Income due to the municipality is recognized/credited. The

corresponding share of the province and barangay shall also be credited to Due to

LGUs.

1.3 Pursuant to the above regulation, the Municipal Treasurer prepares, at the

beginning of each year, a list of taxpayers and the amount due and collectible for

the year. This is supposed to have been previously updated to include all new

assessments and reassessments as reported by the Municipal Assessor to the

treasurer on or before December 31 (Sec. 248, R.A. 7160). The certified list of

taxpayers and amounts due is based on the Real Property Tax Account

Register/Taxpayer’s Index Card maintained by the treasurer.

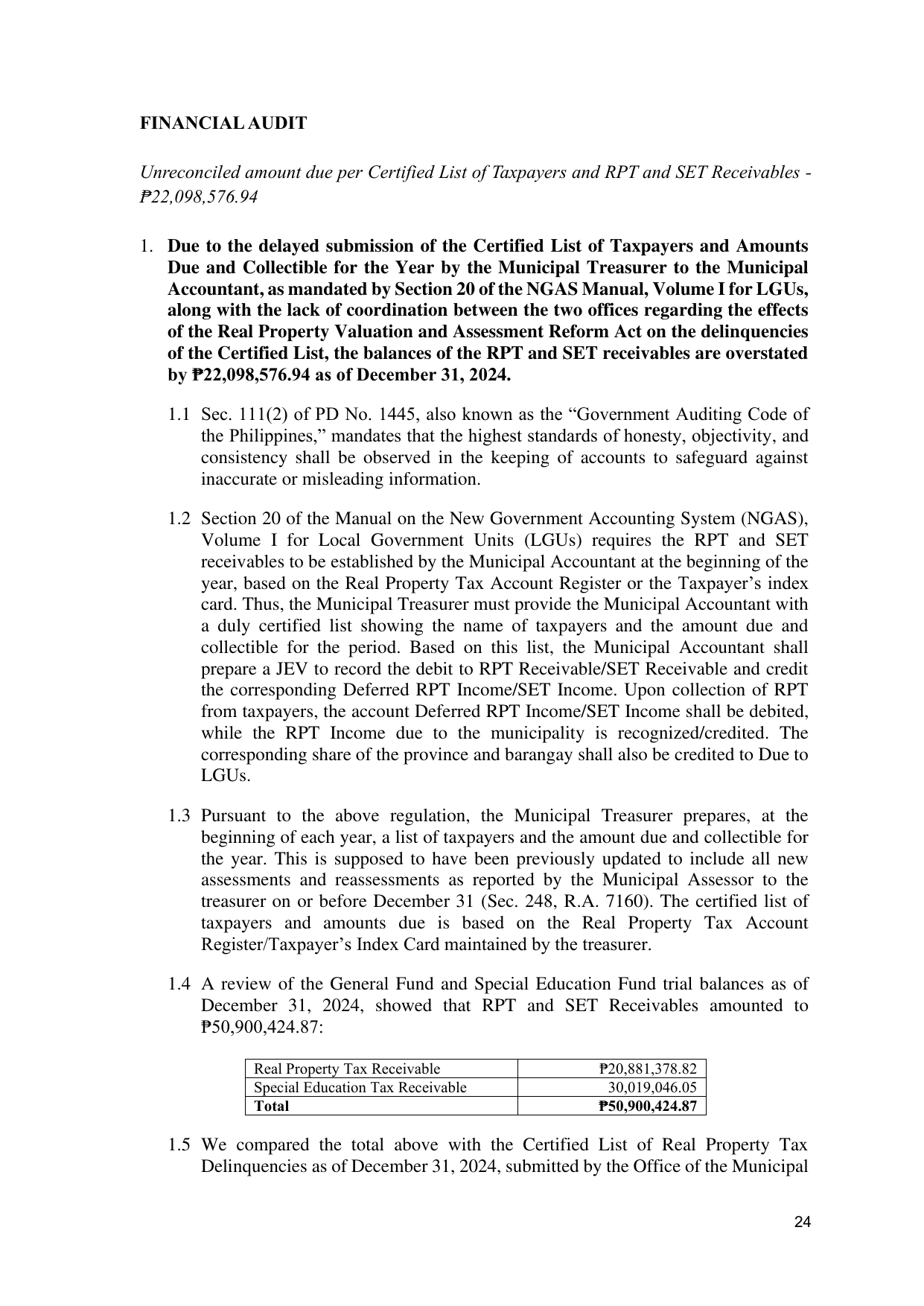

1.4 A review of the General Fund and Special Education Fund trial balances as of

December 31, 2024, showed that RPT and SET Receivables amounted to

₱50,900,424.87:

Real Property Tax Receivable ₱20,881,378.82

Special Education Tax Receivable 30,019,046.05

Total ₱50,900,424.87

1.5 We compared the total above with the Certified List of Real Property Tax

Delinquencies as of December 31, 2024, submitted by the Office of the Municipal

24