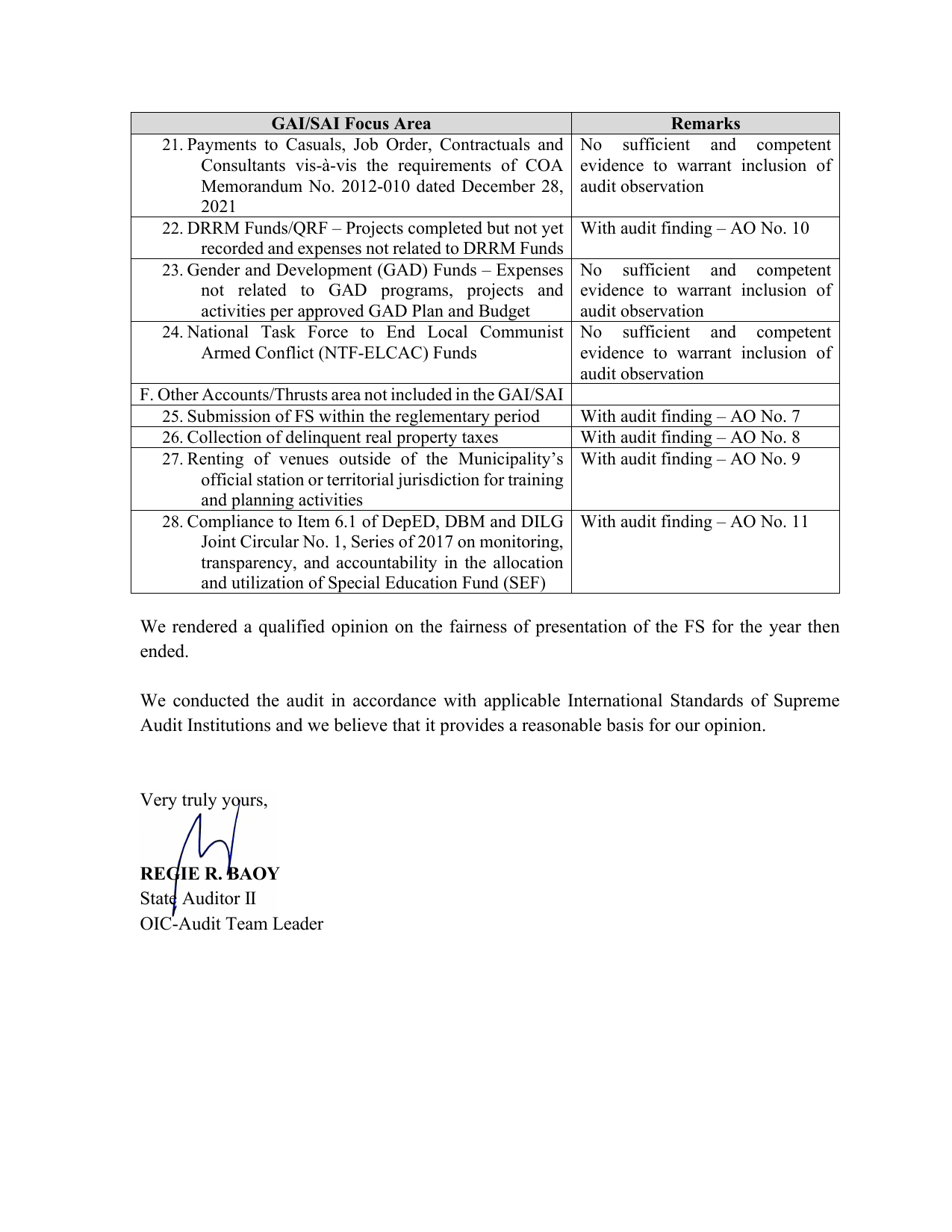

GAI/SAI Focus Area Remarks

21. Payments to Casuals, Job Order, Contractuals and No sufficient and competent

Consultants vis-à-vis the requirements of COA evidence to warrant inclusion of

Memorandum No. 2012-010 dated December 28, audit observation

2021

22. DRRM Funds/QRF – Projects completed but not yet With audit finding – AO No. 10

recorded and expenses not related to DRRM Funds

23. Gender and Development (GAD) Funds – Expenses No sufficient and competent

not related to GAD programs, projects and evidence to warrant inclusion of

activities per approved GAD Plan and Budget audit observation

24. National Task Force to End Local Communist No sufficient and competent

Armed Conflict (NTF-ELCAC) Funds evidence to warrant inclusion of

audit observation

F. Other Accounts/Thrusts area not included in the GAI/SAI

25. Submission of FS within the reglementary period With audit finding – AO No. 7

26. Collection of delinquent real property taxes With audit finding – AO No. 8

27. Renting of venues outside of the Municipality’s With audit finding – AO No. 9

official station or territorial jurisdiction for training

and planning activities

28. Compliance to Item 6.1 of DepED, DBM and DILG With audit finding – AO No. 11

Joint Circular No. 1, Series of 2017 on monitoring,

transparency, and accountability in the allocation

and utilization of Special Education Fund (SEF)

We rendered a qualified opinion on the fairness of presentation of the FS for the year then

ended.

We conducted the audit in accordance with applicable International Standards of Supreme

Audit Institutions and we believe that it provides a reasonable basis for our opinion.

Very truly yours,

REGIE R. BAOY

State Auditor II

OIC-Audit Team Leader