1. Repairs and Maintenance – Land Improvements. This account is used to

record the cost of repairs and maintenance on Aquaculture structures and

other land improvements constructed/ acquired/ developed for public use.

2. Environment/Sanitary Services. This account is used to record the cost of

services contracted/undertaken by administration for the upkeep and

sanitation of the public places. This includes the cost of clean and green

program, garbage and hospital waste collection and disposal.

6.3 Our verification of the Disbursement Vouchers (DVs) revealed that in CY 2024,

the Municipality paid the LGU of Bayawan City a total of ₱170,215.00 as a

tipping fee. A review of the Memorandum of Agreement between the

Municipality of San Jose and the City of Bayawan showed that this payment is a

requirement for the disposal of the Municipality’s solid waste at Bayawan City’s

Sanitary Landfill. Therefore, the tipping fee should be recorded under the

“Environment/Sanitary Services” account as it pertains to the cost of garbage

disposal.

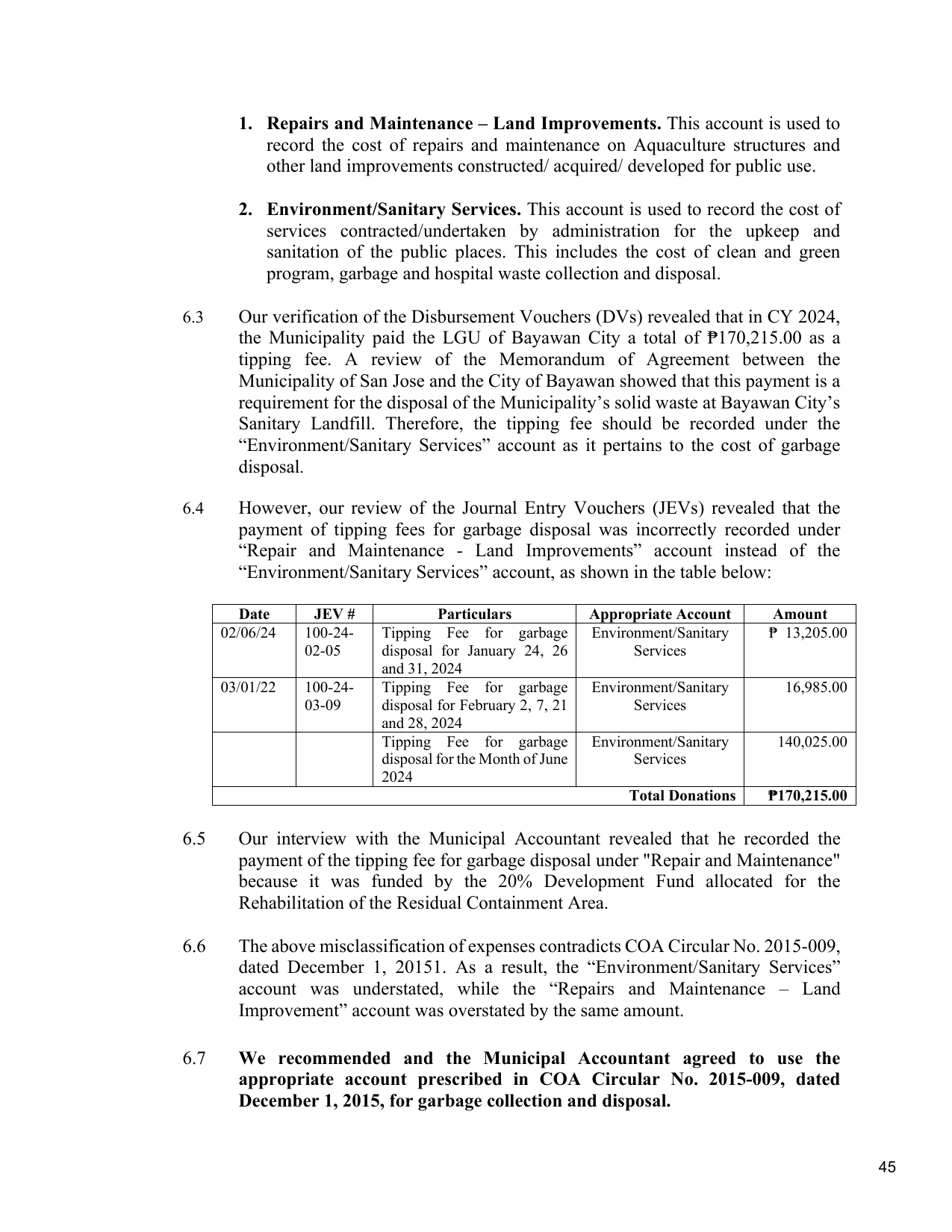

6.4 However, our review of the Journal Entry Vouchers (JEVs) revealed that the

payment of tipping fees for garbage disposal was incorrectly recorded under

“Repair and Maintenance - Land Improvements” account instead of the

“Environment/Sanitary Services” account, as shown in the table below:

Date JEV # Particulars Appropriate Account Amount

02/06/24 100-24- Tipping Fee for garbage Environment/Sanitary ₱ 13,205.00

02-05 disposal for January 24, 26 Services

and 31, 2024

03/01/22 100-24- Tipping Fee for garbage Environment/Sanitary 16,985.00

03-09 disposal for February 2, 7, 21 Services

and 28, 2024

Tipping Fee for garbage Environment/Sanitary 140,025.00

disposal for the Month of June Services

2024

Total Donations ₱170,215.00

6.5 Our interview with the Municipal Accountant revealed that he recorded the

payment of the tipping fee for garbage disposal under "Repair and Maintenance"

because it was funded by the 20% Development Fund allocated for the

Rehabilitation of the Residual Containment Area.

6.6 The above misclassification of expenses contradicts COA Circular No. 2015-009,

dated December 1, 20151. As a result, the “Environment/Sanitary Services”

account was understated, while the “Repairs and Maintenance – Land

Improvement” account was overstated by the same amount.

6.7 We recommended and the Municipal Accountant agreed to use the

appropriate account prescribed in COA Circular No. 2015-009, dated

December 1, 2015, for garbage collection and disposal.

45