4.1 COA Circular No. 96-011 dated October 2, 1996, provides guidelines on the

preparation of the BRS. Item 3.3 of the circular requires the accountant to draw

journal vouchers to record all valid reconciling items that require adjustment and

correction in the General Ledger (GL).

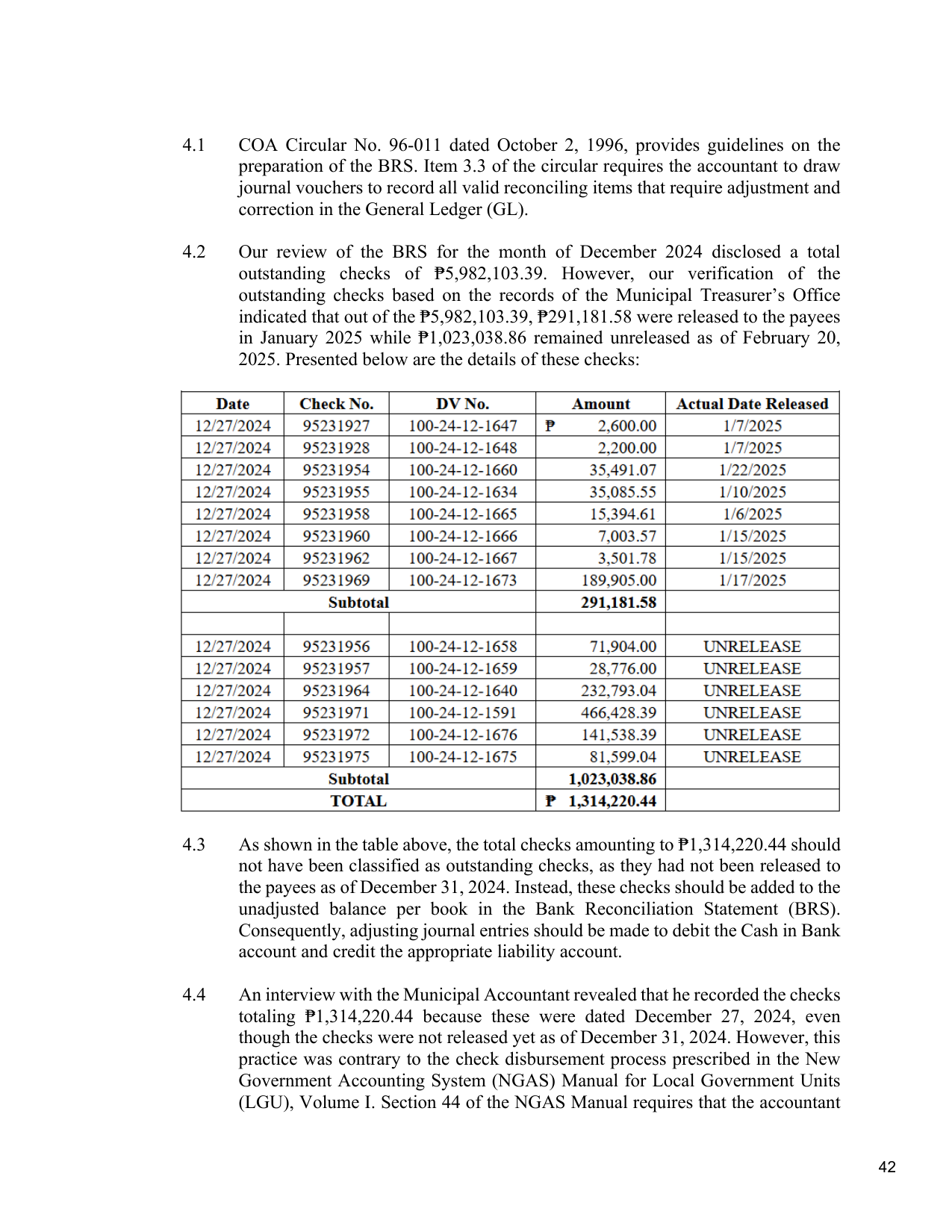

4.2 Our review of the BRS for the month of December 2024 disclosed a total

outstanding checks of ₱5,982,103.39. However, our verification of the

outstanding checks based on the records of the Municipal Treasurer’s Office

indicated that out of the ₱5,982,103.39, ₱291,181.58 were released to the payees

in January 2025 while ₱1,023,038.86 remained unreleased as of February 20,

2025. Presented below are the details of these checks:

4.3 As shown in the table above, the total checks amounting to ₱1,314,220.44 should

not have been classified as outstanding checks, as they had not been released to

the payees as of December 31, 2024. Instead, these checks should be added to the

unadjusted balance per book in the Bank Reconciliation Statement (BRS).

Consequently, adjusting journal entries should be made to debit the Cash in Bank

account and credit the appropriate liability account.

4.4 An interview with the Municipal Accountant revealed that he recorded the checks

totaling ₱1,314,220.44 because these were dated December 27, 2024, even

though the checks were not released yet as of December 31, 2024. However, this

practice was contrary to the check disbursement process prescribed in the New

Government Accounting System (NGAS) Manual for Local Government Units

(LGU), Volume I. Section 44 of the NGAS Manual requires that the accountant

42