5.12 Property records shall be updated based on the results of the physical

inventory and reconciled with accounting records to come up with the

reconciled balances of PPE accounts to be considered as the correct

balance of the agency's PPEs.”

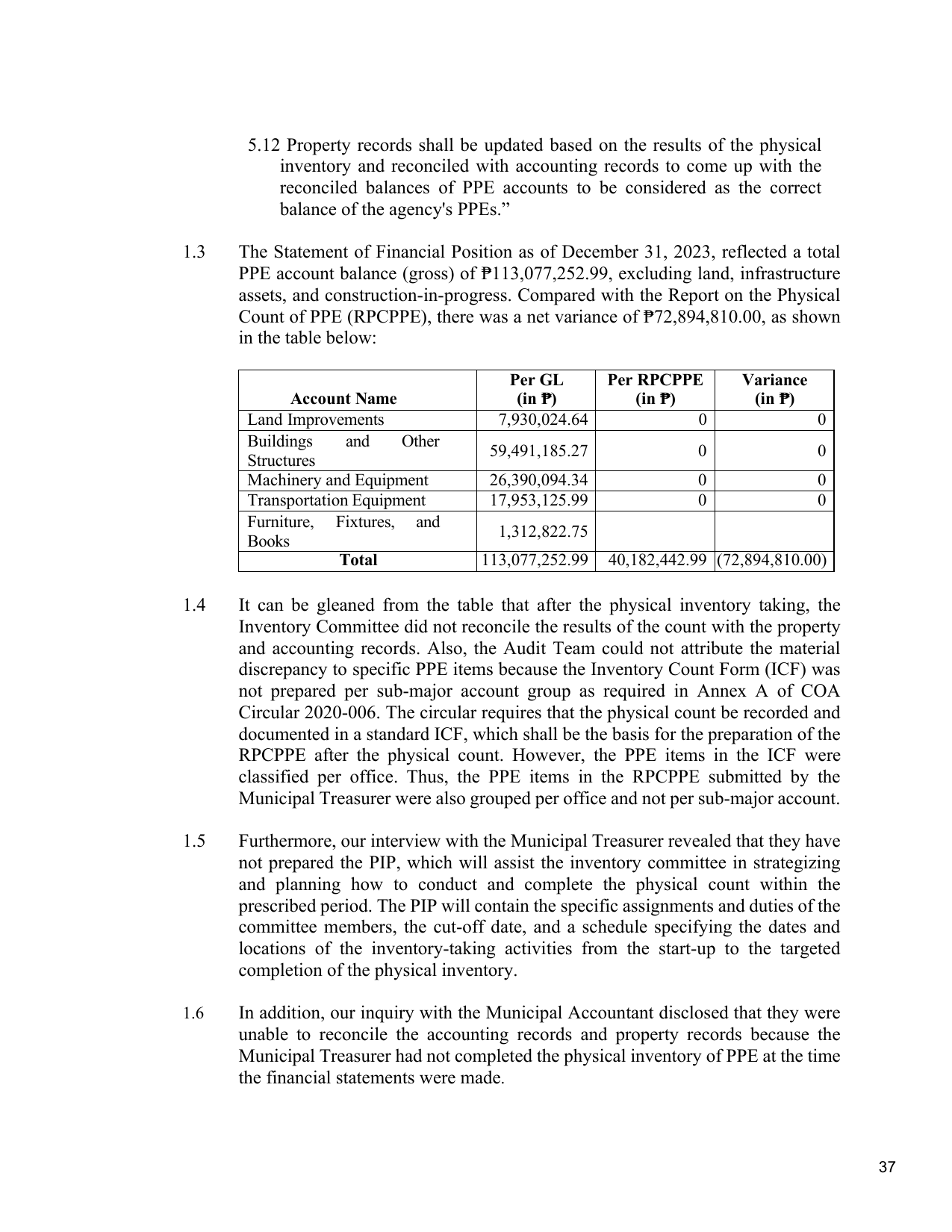

1.3 The Statement of Financial Position as of December 31, 2023, reflected a total

PPE account balance (gross) of ₱113,077,252.99, excluding land, infrastructure

assets, and construction-in-progress. Compared with the Report on the Physical

Count of PPE (RPCPPE), there was a net variance of ₱72,894,810.00, as shown

in the table below:

Per GL Per RPCPPE Variance

Account Name (in ₱) (in ₱) (in ₱)

Land Improvements 7,930,024.64 0 0

Buildings and Other

59,491,185.27 0 0

Structures

Machinery and Equipment 26,390,094.34 0 0

Transportation Equipment 17,953,125.99 0 0

Furniture, Fixtures, and

1,312,822.75

Books

Total 113,077,252.99 40,182,442.99 (72,894,810.00)

1.4 It can be gleaned from the table that after the physical inventory taking, the

Inventory Committee did not reconcile the results of the count with the property

and accounting records. Also, the Audit Team could not attribute the material

discrepancy to specific PPE items because the Inventory Count Form (ICF) was

not prepared per sub-major account group as required in Annex A of COA

Circular 2020-006. The circular requires that the physical count be recorded and

documented in a standard ICF, which shall be the basis for the preparation of the

RPCPPE after the physical count. However, the PPE items in the ICF were

classified per office. Thus, the PPE items in the RPCPPE submitted by the

Municipal Treasurer were also grouped per office and not per sub-major account.

1.5 Furthermore, our interview with the Municipal Treasurer revealed that they have

not prepared the PIP, which will assist the inventory committee in strategizing

and planning how to conduct and complete the physical count within the

prescribed period. The PIP will contain the specific assignments and duties of the

committee members, the cut-off date, and a schedule specifying the dates and

locations of the inventory-taking activities from the start-up to the targeted

completion of the physical inventory.

1.6 In addition, our inquiry with the Municipal Accountant disclosed that they were

unable to reconcile the accounting records and property records because the

Municipal Treasurer had not completed the physical inventory of PPE at the time

the financial statements were made.

37