Furthermore, we recommended that the Municipal Treasurer regularly issue

written notice to the payees at least one month before a check becomes stales,

informing them of the check’s existence.

2. Expenses for garbage collection and disposal totaling ₱170,215.00 were

erroneously recorded under the Repairs and Maintenance- Land

Improvements account instead of the “Environment/Sanitary Services”

account, resulting in an understatement of the “Environment/Sanitary

Services” account and an overstatement of the “Repairs and Maintenance –

Land Improvement” account by the same amount.

We recommended that the Municipal Accountant use the appropriate account for

garbage collection and disposal, as prescribed in COA Circular No. 2015-009

dated December 1, 2015.

3. The Municipality risks losing potential revenue that could be used to finance

development projects programs and activities (PPAs) due to a low collection

of delinquent real property taxes (RPT) amounting to ₱25,770,471.90 as of

December 31, 2024. Consequently, the Municipality.

We recommended and the Municipal Treasurer and Municipal Assessor agreed to

conduct tax mapping to cleanse their records of real properties and post the Notice

of Delinquency in the Payment of RPT pursuant to Section 254 of R.A 7160.

We further recommended that, after the Notice of Delinquency in the Payment of

RPT is posted, Management avail itself of the remedies provided under R.A. No.

7160 to collect delinquent taxes.

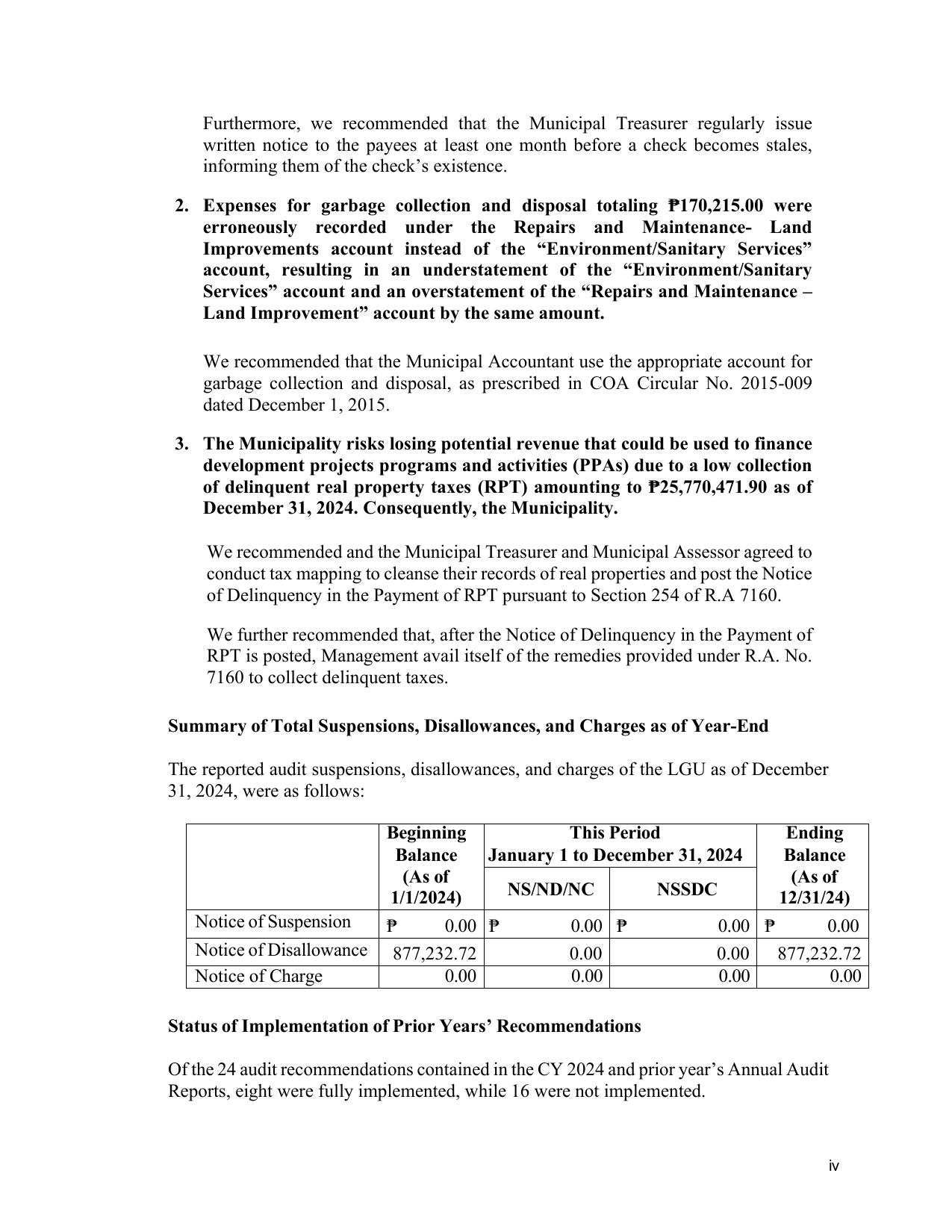

Summary of Total Suspensions, Disallowances, and Charges as of Year-End

The reported audit suspensions, disallowances, and charges of the LGU as of December

31, 2024, were as follows:

Beginning This Period Ending

Balance January 1 to December 31, 2024 Balance

(As of (As of

1/1/2024) NS/ND/NC NSSDC 12/31/24)

Notice of Suspension ₱ 0.00 ₱ 0.00 ₱ 0.00 ₱ 0.00

Notice of Disallowance 877,232.72 0.00 0.00 877,232.72

Notice of Charge 0.00 0.00 0.00 0.00

Status of Implementation of Prior Years’ Recommendations

Of the 24 audit recommendations contained in the CY 2024 and prior year’s Annual Audit

Reports, eight were fully implemented, while 16 were not implemented.

iv