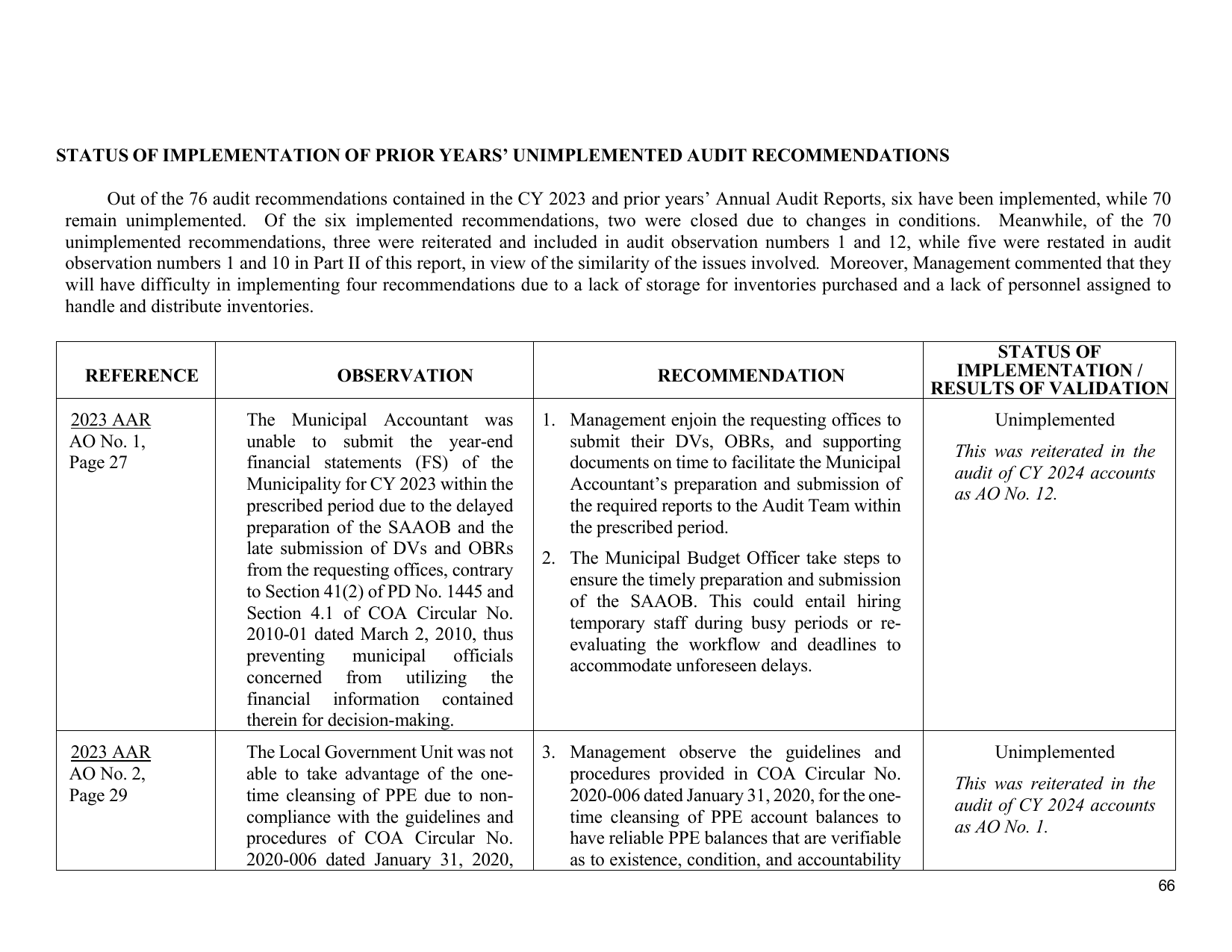

STATUS OF IMPLEMENTATION OF PRIOR YEARS’ UNIMPLEMENTED AUDIT RECOMMENDATIONS

Out of the 76 audit recommendations contained in the CY 2023 and prior years’ Annual Audit Reports, six have been implemented, while 70

remain unimplemented. Of the six implemented recommendations, two were closed due to changes in conditions. Meanwhile, of the 70

unimplemented recommendations, three were reiterated and included in audit observation numbers 1 and 12, while five were restated in audit

observation numbers 1 and 10 in Part II of this report, in view of the similarity of the issues involved. Moreover, Management commented that they

will have difficulty in implementing four recommendations due to a lack of storage for inventories purchased and a lack of personnel assigned to

handle and distribute inventories.

STATUS OF

REFERENCE OBSERVATION RECOMMENDATION IMPLEMENTATION /

RESULTS OF VALIDATION

2023 AAR The Municipal Accountant was 1. Management enjoin the requesting offices to Unimplemented

AO No. 1, unable to submit the year-end submit their DVs, OBRs, and supporting

This was reiterated in the

Page 27 financial statements (FS) of the documents on time to facilitate the Municipal

audit of CY 2024 accounts

Municipality for CY 2023 within the Accountant’s preparation and submission of

as AO No. 12.

prescribed period due to the delayed the required reports to the Audit Team within

preparation of the SAAOB and the the prescribed period.

late submission of DVs and OBRs

2. The Municipal Budget Officer take steps to

from the requesting offices, contrary

ensure the timely preparation and submission

to Section 41(2) of PD No. 1445 and

of the SAAOB. This could entail hiring

Section 4.1 of COA Circular No.

temporary staff during busy periods or re-

2010-01 dated March 2, 2010, thus

evaluating the workflow and deadlines to

preventing municipal officials

accommodate unforeseen delays.

concerned from utilizing the

financial information contained

therein for decision-making.

2023 AAR The Local Government Unit was not 3. Management observe the guidelines and Unimplemented

AO No. 2, able to take advantage of the one- procedures provided in COA Circular No.

This was reiterated in the

Page 29 time cleansing of PPE due to non- 2020-006 dated January 31, 2020, for the one-

audit of CY 2024 accounts

compliance with the guidelines and time cleansing of PPE account balances to

as AO No. 1.

procedures of COA Circular No. have reliable PPE balances that are verifiable

2020-006 dated January 31, 2020, as to existence, condition, and accountability

66