Completed infrastructure projects not reclassified to appropriate PPE accounts – ₱12,111,182.21

6. Completed infrastructure projects totaling ₱12,111,182.21 were not reclassified

from the Construction in Progress (CIP) account to the appropriate Property, Plant,

and Equipment (PPE) accounts upon completion, contrary to Section 50 of the New

Government Accounting System (NGAS) Manual for LGUs, Volume I, thereby

omitting the recognition of depreciation and misstating the balances of affected

accounts in the financial statements.

6.1 Section 50 of the NGAS for LGUs, Volume I, requires that during the

construction period, agency assets and public infrastructures shall be taken up in

the books as “Construction in Progress” with the appropriate asset classification.

As soon as the project is completed, the Construction in Progress for agency

assets is closed to the appropriate asset account.

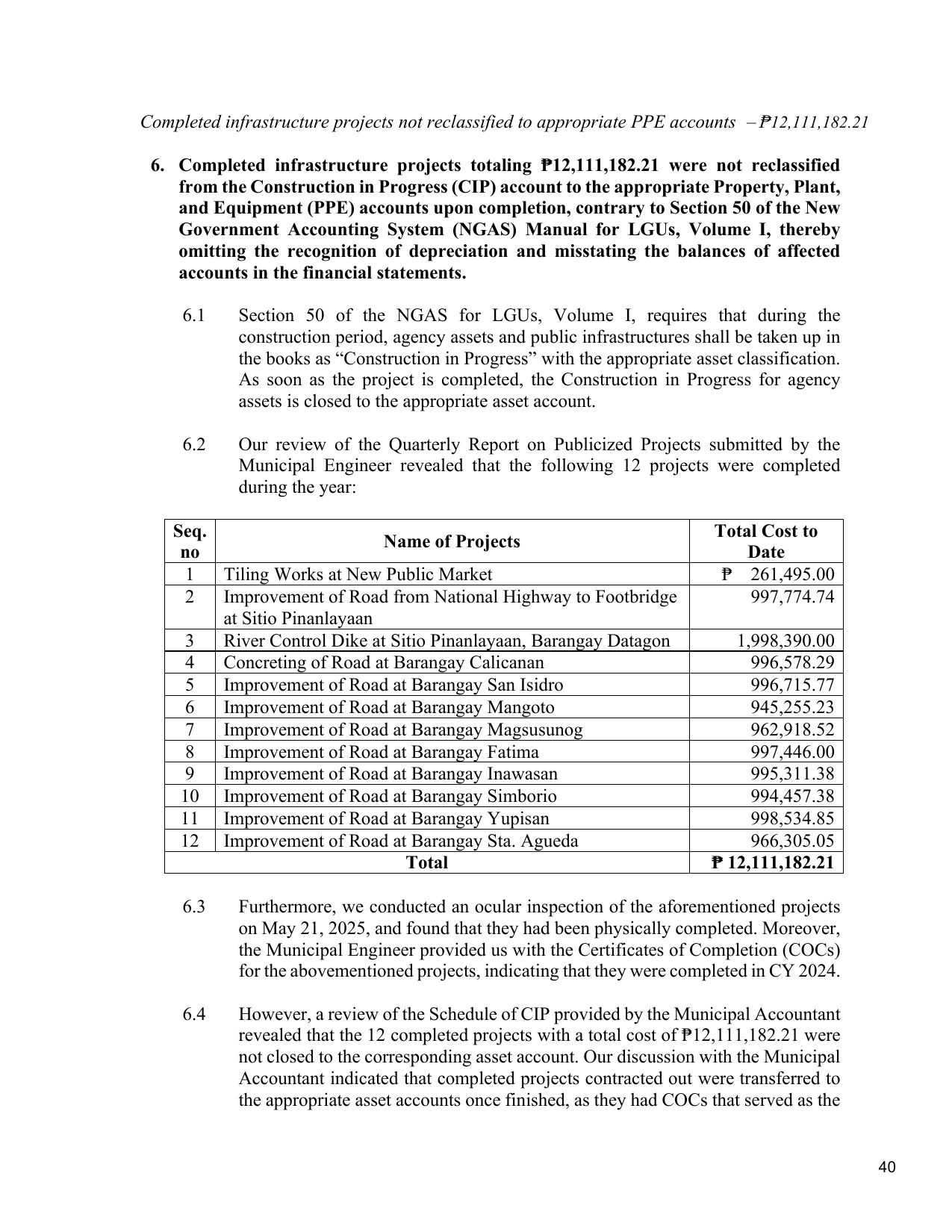

6.2 Our review of the Quarterly Report on Publicized Projects submitted by the

Municipal Engineer revealed that the following 12 projects were completed

during the year:

Seq. Total Cost to

Name of Projects

no Date

1 Tiling Works at New Public Market ₱ 261,495.00

2 Improvement of Road from National Highway to Footbridge 997,774.74

at Sitio Pinanlayaan

3 River Control Dike at Sitio Pinanlayaan, Barangay Datagon 1,998,390.00

4 Concreting of Road at Barangay Calicanan 996,578.29

5 Improvement of Road at Barangay San Isidro 996,715.77

6 Improvement of Road at Barangay Mangoto 945,255.23

7 Improvement of Road at Barangay Magsusunog 962,918.52

8 Improvement of Road at Barangay Fatima 997,446.00

9 Improvement of Road at Barangay Inawasan 995,311.38

10 Improvement of Road at Barangay Simborio 994,457.38

11 Improvement of Road at Barangay Yupisan 998,534.85

12 Improvement of Road at Barangay Sta. Agueda 966,305.05

Total ₱ 12,111,182.21

6.3 Furthermore, we conducted an ocular inspection of the aforementioned projects

on May 21, 2025, and found that they had been physically completed. Moreover,

the Municipal Engineer provided us with the Certificates of Completion (COCs)

for the abovementioned projects, indicating that they were completed in CY 2024.

6.4 However, a review of the Schedule of CIP provided by the Municipal Accountant

revealed that the 12 completed projects with a total cost of ₱12,111,182.21 were

not closed to the corresponding asset account. Our discussion with the Municipal

Accountant indicated that completed projects contracted out were transferred to

the appropriate asset accounts once finished, as they had COCs that served as the

40