prevailing cost to sell these biological assets.

3. The Municipal Accountant did not prepare Journal Entry Vouchers

(JEV) for book reconciling items in the Bank Reconciliation Statements

(BRS) totaling ₱1,792,371.24, resulting in an understatement of both the

Cash in Bank and Liability accounts by the same amount.

We recommended that the Municipal Accountant prepare JEVs for valid

reconciling items that require adjustment and correction in the GL.

We further recommended that the Municipal Accountant follow the check

disbursement process prescribed in Section 44 of the NGAS Manual for

LGUs, Volume I, to ensure that the JEVs are prepared and recorded based on

the RCI together with the DVs and supporting documents received from the

Municipal Treasurer’s Office.

These and all other audit observations and recommendations are discussed in

detail in Part II of this Report.

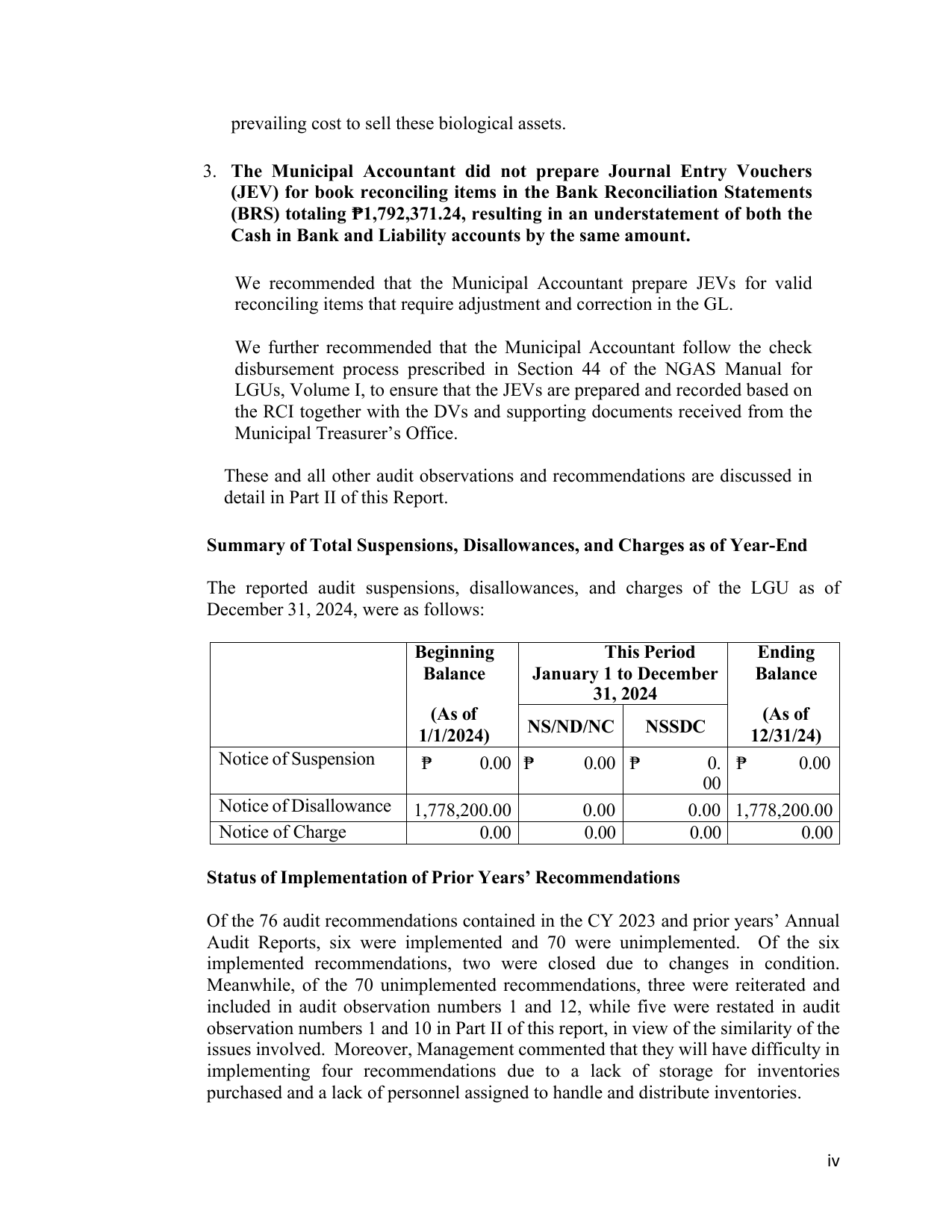

Summary of Total Suspensions, Disallowances, and Charges as of Year-End

The reported audit suspensions, disallowances, and charges of the LGU as of

December 31, 2024, were as follows:

Beginning This Period Ending

Balance January 1 to December Balance

31, 2024

(As of (As of

1/1/2024) NS/ND/NC NSSDC 12/31/24)

Notice of Suspension ₱ 0.00 ₱ 0.00 ₱ 0. ₱ 0.00

00

Notice of Disallowance 1,778,200.00 0.00 0.00 1,778,200.00

Notice of Charge 0.00 0.00 0.00 0.00

Status of Implementation of Prior Years’ Recommendations

Of the 76 audit recommendations contained in the CY 2023 and prior years’ Annual

Audit Reports, six were implemented and 70 were unimplemented. Of the six

implemented recommendations, two were closed due to changes in condition.

Meanwhile, of the 70 unimplemented recommendations, three were reiterated and

included in audit observation numbers 1 and 12, while five were restated in audit

observation numbers 1 and 10 in Part II of this report, in view of the similarity of the

issues involved. Moreover, Management commented that they will have difficulty in

implementing four recommendations due to a lack of storage for inventories

purchased and a lack of personnel assigned to handle and distribute inventories.

iv