STATUS OF

REFERENCE OBSERVATION RECOMMENDATION IMPLEMENTATION /

RESULTS OF VALIDATION

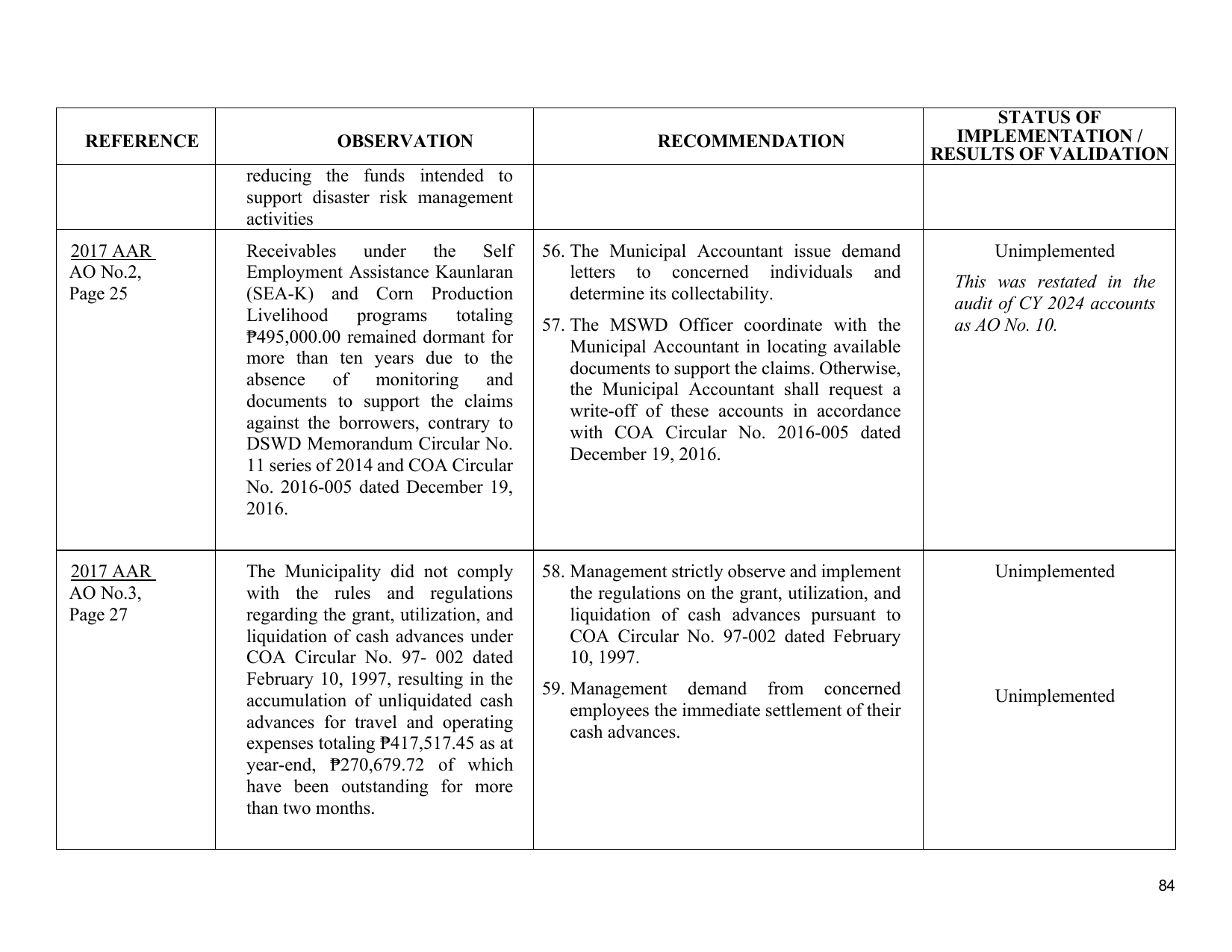

reducing the funds intended to

support disaster risk management

activities

2017 AAR Receivables under the Self 56. The Municipal Accountant issue demand Unimplemented

AO No.2, Employment Assistance Kaunlaran letters to concerned individuals and

This was restated in the

Page 25 (SEA-K) and Corn Production determine its collectability.

audit of CY 2024 accounts

Livelihood programs totaling

57. The MSWD Officer coordinate with the as AO No. 10.

₱495,000.00 remained dormant for

Municipal Accountant in locating available

more than ten years due to the

documents to support the claims. Otherwise,

absence of monitoring and

the Municipal Accountant shall request a

documents to support the claims

write-off of these accounts in accordance

against the borrowers, contrary to

with COA Circular No. 2016-005 dated

DSWD Memorandum Circular No.

December 19, 2016.

11 series of 2014 and COA Circular

No. 2016-005 dated December 19,

2016.

2017 AAR The Municipality did not comply 58. Management strictly observe and implement Unimplemented

AO No.3, with the rules and regulations the regulations on the grant, utilization, and

Page 27 regarding the grant, utilization, and liquidation of cash advances pursuant to

liquidation of cash advances under COA Circular No. 97-002 dated February

COA Circular No. 97- 002 dated 10, 1997.

February 10, 1997, resulting in the

59. Management demand from concerned Unimplemented

accumulation of unliquidated cash

employees the immediate settlement of their

advances for travel and operating

cash advances.

expenses totaling ₱417,517.45 as at

year-end, ₱270,679.72 of which

have been outstanding for more

than two months.

84