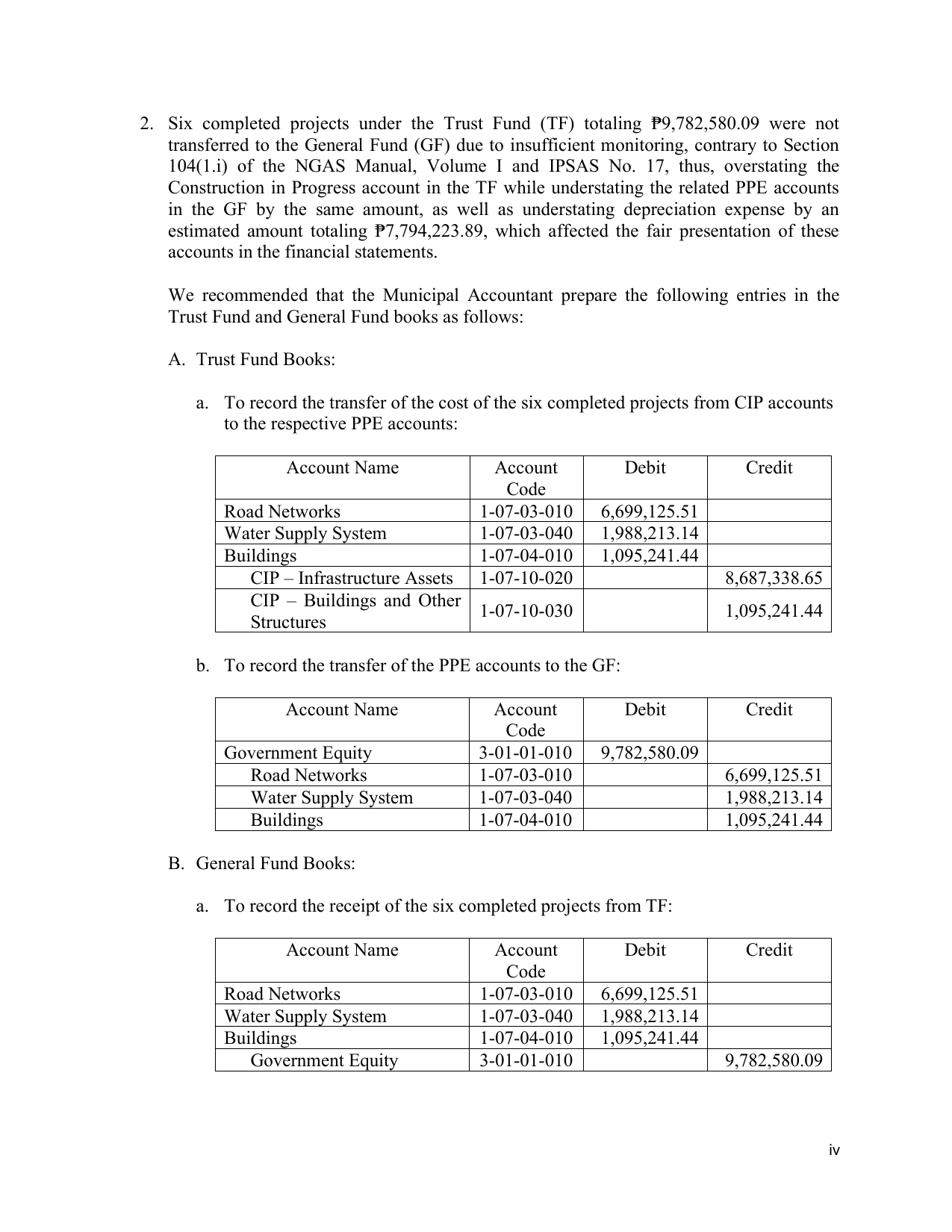

2. Six completed projects under the Trust Fund (TF) totaling ₱9,782,580.09 were not

transferred to the General Fund (GF) due to insufficient monitoring, contrary to Section

104(1.i) of the NGAS Manual, Volume I and IPSAS No. 17, thus, overstating the

Construction in Progress account in the TF while understating the related PPE accounts

in the GF by the same amount, as well as understating depreciation expense by an

estimated amount totaling ₱7,794,223.89, which affected the fair presentation of these

accounts in the financial statements.

We recommended that the Municipal Accountant prepare the following entries in the

Trust Fund and General Fund books as follows:

A. Trust Fund Books:

a. To record the transfer of the cost of the six completed projects from CIP accounts

to the respective PPE accounts:

Account Name Account Debit Credit

Code

Road Networks 1-07-03-010 6,699,125.51

Water Supply System 1-07-03-040 1,988,213.14

Buildings 1-07-04-010 1,095,241.44

CIP – Infrastructure Assets 1-07-10-020 8,687,338.65

CIP – Buildings and Other

1-07-10-030 1,095,241.44

Structures

b. To record the transfer of the PPE accounts to the GF:

Account Name Account Debit Credit

Code

Government Equity 3-01-01-010 9,782,580.09

Road Networks 1-07-03-010 6,699,125.51

Water Supply System 1-07-03-040 1,988,213.14

Buildings 1-07-04-010 1,095,241.44

B. General Fund Books:

a. To record the receipt of the six completed projects from TF:

Account Name Account Debit Credit

Code

Road Networks 1-07-03-010 6,699,125.51

Water Supply System 1-07-03-040 1,988,213.14

Buildings 1-07-04-010 1,095,241.44

Government Equity 3-01-01-010 9,782,580.09

iv