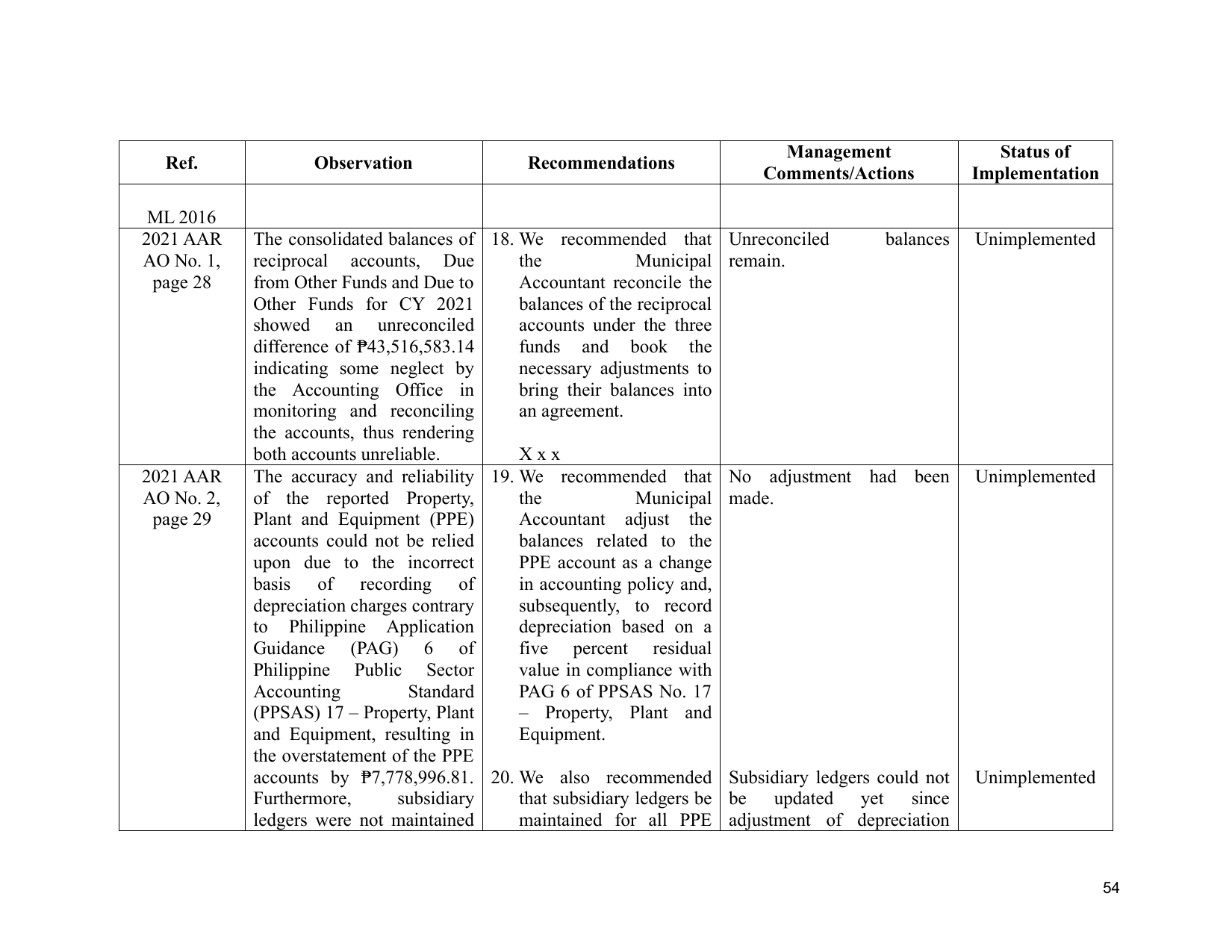

Management Status of

Ref. Observation Recommendations

Comments/Actions Implementation

ML 2016

2021 AAR The consolidated balances of 18. We recommended that Unreconciled balances Unimplemented

AO No. 1, reciprocal accounts, Due the Municipal remain.

page 28 from Other Funds and Due to Accountant reconcile the

Other Funds for CY 2021 balances of the reciprocal

showed an unreconciled accounts under the three

difference of ₱43,516,583.14 funds and book the

indicating some neglect by necessary adjustments to

the Accounting Office in bring their balances into

monitoring and reconciling an agreement.

the accounts, thus rendering

both accounts unreliable. Xxx

2021 AAR The accuracy and reliability 19. We recommended that No adjustment had been Unimplemented

AO No. 2, of the reported Property, the Municipal made.

page 29 Plant and Equipment (PPE) Accountant adjust the

accounts could not be relied balances related to the

upon due to the incorrect PPE account as a change

basis of recording of in accounting policy and,

depreciation charges contrary subsequently, to record

to Philippine Application depreciation based on a

Guidance (PAG) 6 of five percent residual

Philippine Public Sector value in compliance with

Accounting Standard PAG 6 of PPSAS No. 17

(PPSAS) 17 – Property, Plant – Property, Plant and

and Equipment, resulting in Equipment.

the overstatement of the PPE

accounts by ₱7,778,996.81. 20. We also recommended Subsidiary ledgers could not Unimplemented

Furthermore, subsidiary that subsidiary ledgers be be updated yet since

ledgers were not maintained maintained for all PPE adjustment of depreciation

54