4.8. The inability to transfer the cost of the above PPE accounts from the Trust Fund

to the General Fund resulted in the overstatement of the PPE accounts in the Trust

Fund and the understatement of the same accounts in the General Fund.

Moreover, the non-provision of depreciation expenses for these PPEs understated

the total expenses and overstated the equity accounts in the General Fund by an

undetermined amount, thus adversely affecting the fairness of presentation of the

financial statements.

4.9. This observation was communicated to Management through Audit Observation

Memorandum No. 2025-01(2024)-Manjuyod dated February 21, 2025.

4.10. We recommended and Management agreed that:

4.10.1. The Municipal Mayor require the Municipal Engineer to provide the

Municipal Accountant with a report on completed Trust Fund

projects so that these can immediately be transferred to the General

Fund.

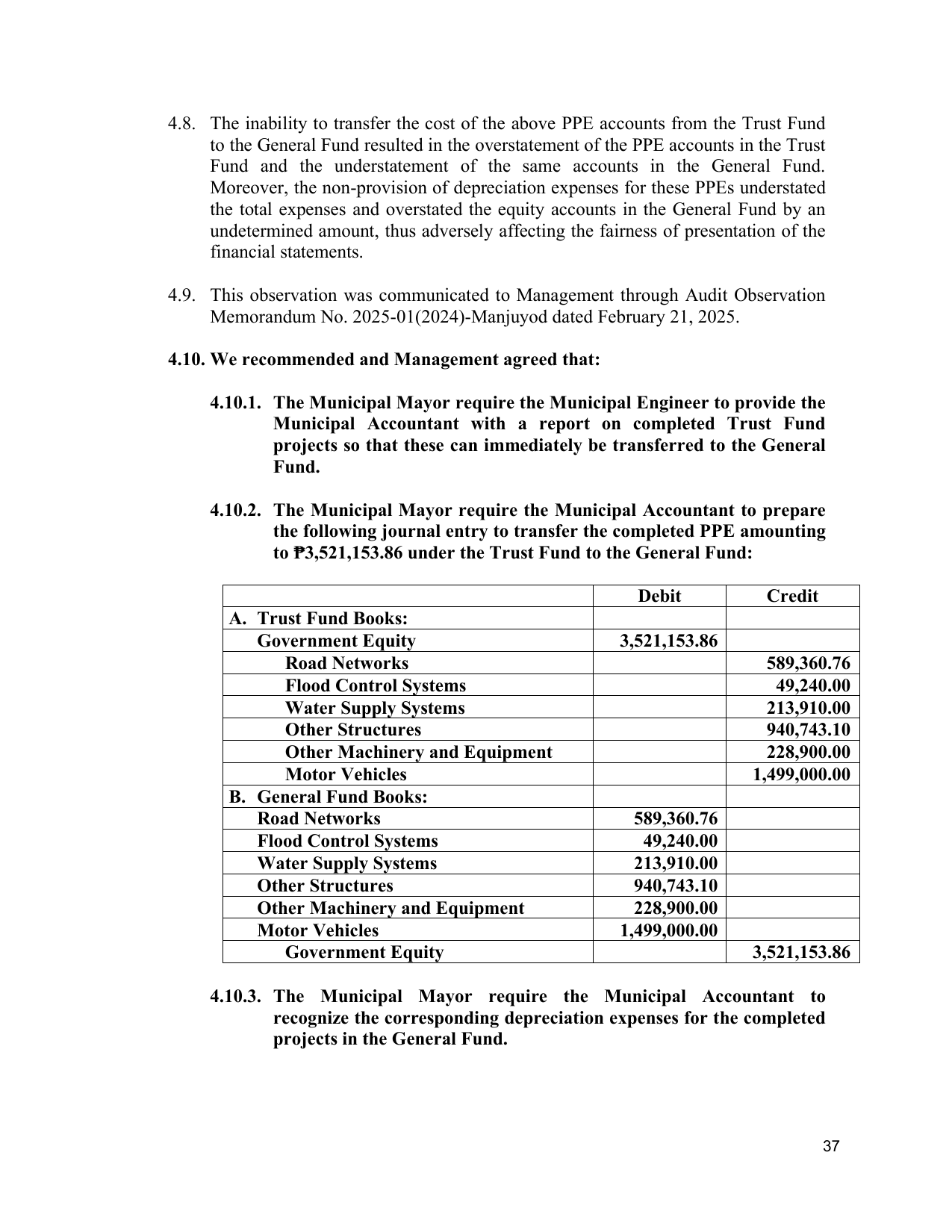

4.10.2. The Municipal Mayor require the Municipal Accountant to prepare

the following journal entry to transfer the completed PPE amounting

to ₱3,521,153.86 under the Trust Fund to the General Fund:

Debit Credit

A. Trust Fund Books:

Government Equity 3,521,153.86

Road Networks 589,360.76

Flood Control Systems 49,240.00

Water Supply Systems 213,910.00

Other Structures 940,743.10

Other Machinery and Equipment 228,900.00

Motor Vehicles 1,499,000.00

B. General Fund Books:

Road Networks 589,360.76

Flood Control Systems 49,240.00

Water Supply Systems 213,910.00

Other Structures 940,743.10

Other Machinery and Equipment 228,900.00

Motor Vehicles 1,499,000.00

Government Equity 3,521,153.86

4.10.3. The Municipal Mayor require the Municipal Accountant to

recognize the corresponding depreciation expenses for the completed

projects in the General Fund.

37