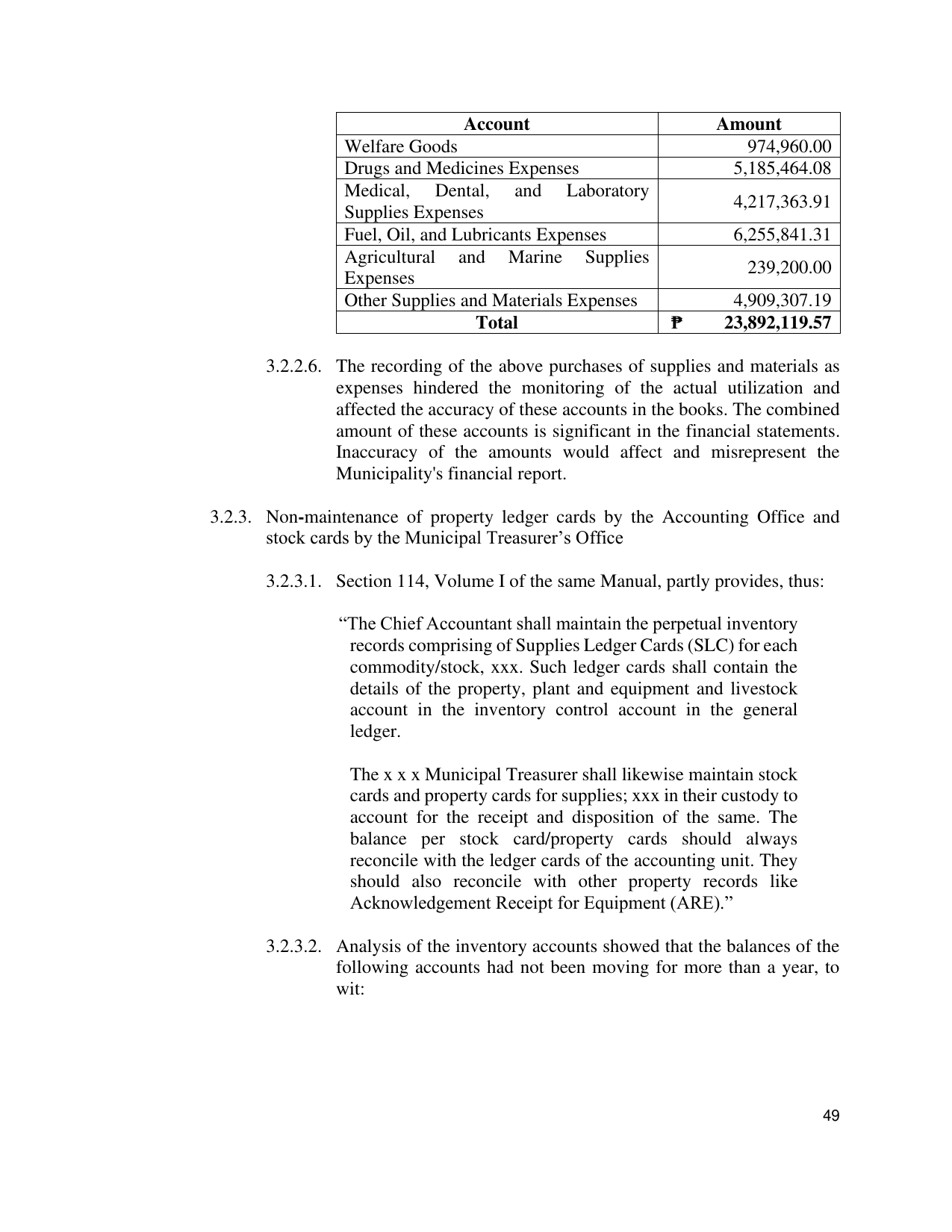

Account Amount

Welfare Goods 974,960.00

Drugs and Medicines Expenses 5,185,464.08

Medical, Dental, and Laboratory

4,217,363.91

Supplies Expenses

Fuel, Oil, and Lubricants Expenses 6,255,841.31

Agricultural and Marine Supplies

239,200.00

Expenses

Other Supplies and Materials Expenses 4,909,307.19

Total ₱ 23,892,119.57

3.2.2.6. The recording of the above purchases of supplies and materials as

expenses hindered the monitoring of the actual utilization and

affected the accuracy of these accounts in the books. The combined

amount of these accounts is significant in the financial statements.

Inaccuracy of the amounts would affect and misrepresent the

Municipality's financial report.

3.2.3. Non-maintenance of property ledger cards by the Accounting Office and

stock cards by the Municipal Treasurer’s Office

3.2.3.1. Section 114, Volume I of the same Manual, partly provides, thus:

“The Chief Accountant shall maintain the perpetual inventory

records comprising of Supplies Ledger Cards (SLC) for each

commodity/stock, xxx. Such ledger cards shall contain the

details of the property, plant and equipment and livestock

account in the inventory control account in the general

ledger.

The x x x Municipal Treasurer shall likewise maintain stock

cards and property cards for supplies; xxx in their custody to

account for the receipt and disposition of the same. The

balance per stock card/property cards should always

reconcile with the ledger cards of the accounting unit. They

should also reconcile with other property records like

Acknowledgement Receipt for Equipment (ARE).”

3.2.3.2. Analysis of the inventory accounts showed that the balances of the

following accounts had not been moving for more than a year, to

wit:

49