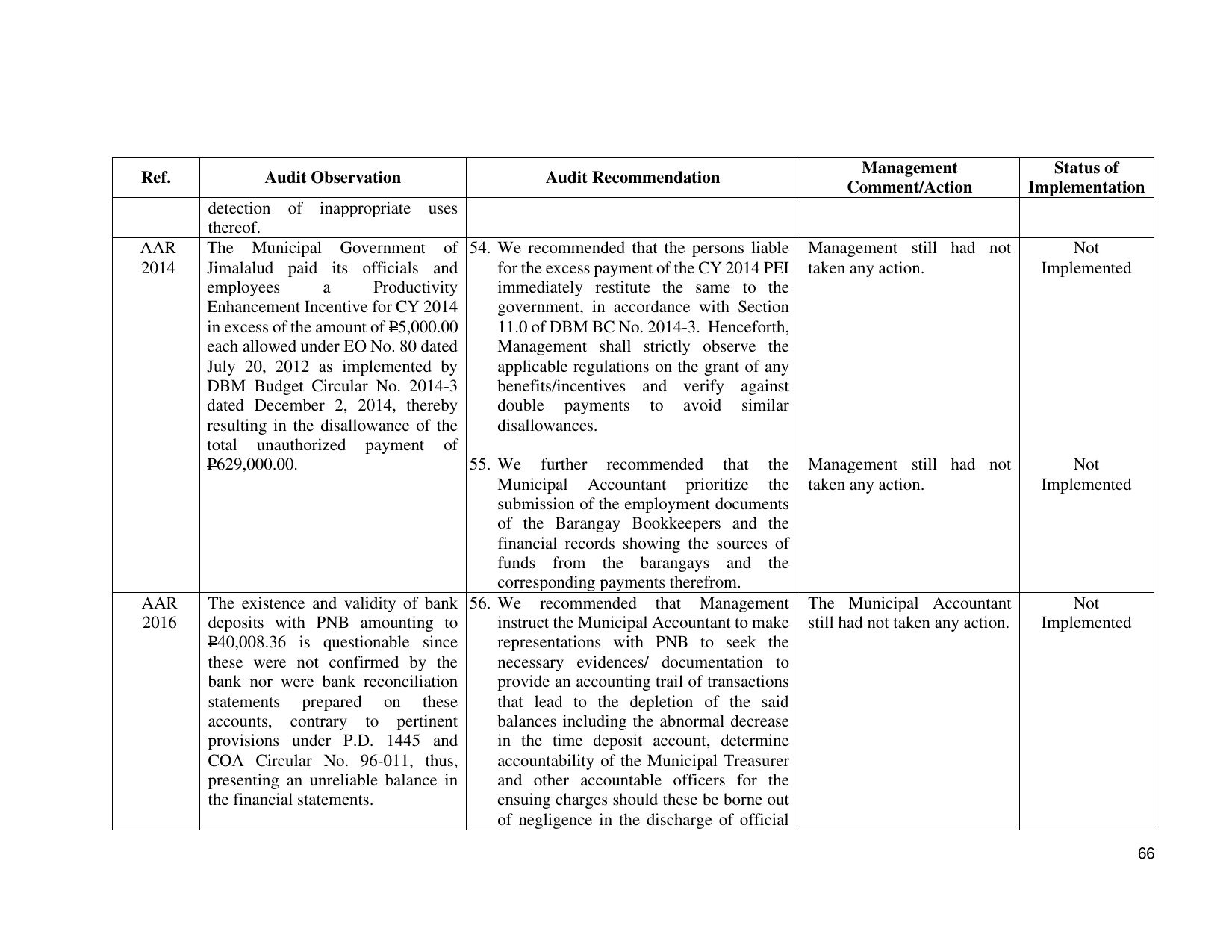

Management Status of

Ref. Audit Observation Audit Recommendation

Comment/Action Implementation

detection of inappropriate uses

thereof.

AAR The Municipal Government of 54. We recommended that the persons liable Management still had not Not

2014 Jimalalud paid its officials and for the excess payment of the CY 2014 PEI taken any action. Implemented

employees a Productivity immediately restitute the same to the

Enhancement Incentive for CY 2014 government, in accordance with Section

in excess of the amount of P5,000.00 11.0 of DBM BC No. 2014-3. Henceforth,

each allowed under EO No. 80 dated Management shall strictly observe the

July 20, 2012 as implemented by applicable regulations on the grant of any

DBM Budget Circular No. 2014-3 benefits/incentives and verify against

dated December 2, 2014, thereby double payments to avoid similar

resulting in the disallowance of the disallowances.

total unauthorized payment of

P629,000.00. 55. We further recommended that the Management still had not Not

Municipal Accountant prioritize the taken any action. Implemented

submission of the employment documents

of the Barangay Bookkeepers and the

financial records showing the sources of

funds from the barangays and the

corresponding payments therefrom.

AAR The existence and validity of bank 56. We recommended that Management The Municipal Accountant Not

2016 deposits with PNB amounting to instruct the Municipal Accountant to make still had not taken any action. Implemented

P40,008.36 is questionable since representations with PNB to seek the

these were not confirmed by the necessary evidences/ documentation to

bank nor were bank reconciliation provide an accounting trail of transactions

statements prepared on these that lead to the depletion of the said

accounts, contrary to pertinent balances including the abnormal decrease

provisions under P.D. 1445 and in the time deposit account, determine

COA Circular No. 96-011, thus, accountability of the Municipal Treasurer

presenting an unreliable balance in and other accountable officers for the

the financial statements. ensuing charges should these be borne out

of negligence in the discharge of official

66