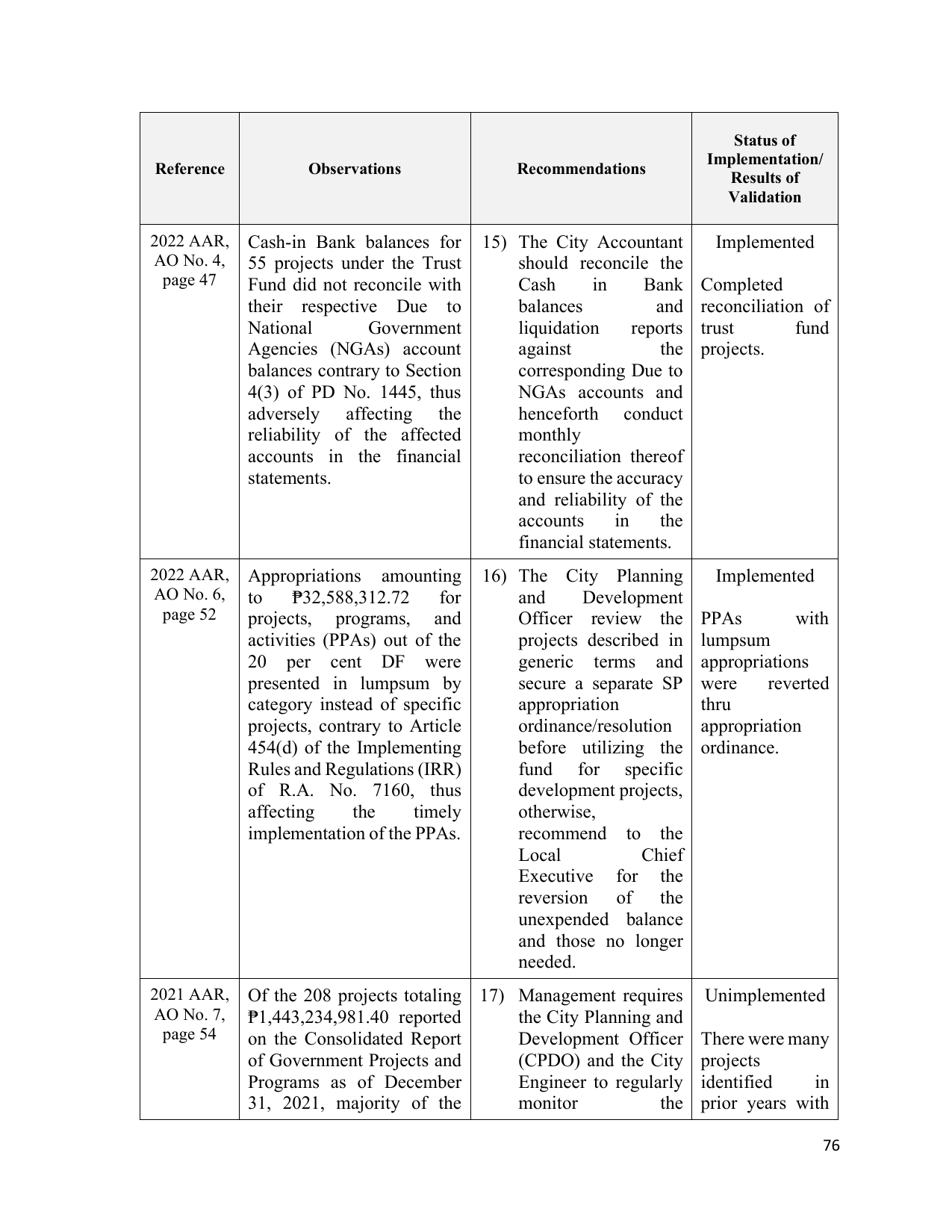

Status of

Implementation/

Reference Observations Recommendations

Results of

Validation

2022 AAR, Cash-in Bank balances for 15) The City Accountant Implemented

AO No. 4, 55 projects under the Trust should reconcile the

page 47 Fund did not reconcile with Cash in Bank Completed

their respective Due to balances and reconciliation of

National Government liquidation reports trust fund

Agencies (NGAs) account against the projects.

balances contrary to Section corresponding Due to

4(3) of PD No. 1445, thus NGAs accounts and

adversely affecting the henceforth conduct

reliability of the affected monthly

accounts in the financial reconciliation thereof

statements. to ensure the accuracy

and reliability of the

accounts in the

financial statements.

2022 AAR, Appropriations amounting 16) The City Planning Implemented

AO No. 6, to ₱32,588,312.72 for and Development

page 52 projects, programs, and Officer review the PPAs with

activities (PPAs) out of the projects described in lumpsum

20 per cent DF were generic terms and appropriations

presented in lumpsum by secure a separate SP were reverted

category instead of specific appropriation thru

projects, contrary to Article ordinance/resolution appropriation

454(d) of the Implementing before utilizing the ordinance.

Rules and Regulations (IRR) fund for specific

of R.A. No. 7160, thus development projects,

affecting the timely otherwise,

implementation of the PPAs. recommend to the

Local Chief

Executive for the

reversion of the

unexpended balance

and those no longer

needed.

2021 AAR, Of the 208 projects totaling 17) Management requires Unimplemented

AO No. 7, ₱1,443,234,981.40 reported the City Planning and

page 54 on the Consolidated Report Development Officer There were many

of Government Projects and (CPDO) and the City projects

Programs as of December Engineer to regularly identified in

31, 2021, majority of the monitor the prior years with

76