Inventories were recognized as expense when issued for utilization or

consumption in the ordinary course of operation.

3.8 Prepayments and Deferred Charges

Prepayments were recorded using the asset method. Adjusting entries were

prepared at the end of the year to record the portion of the prepayment

representing the expense incurred during the current accounting period.

3.9 Property, Plant and Equipment

Property, Plant and Equipment (PPE) were recognized at cost. The cost

includes the purchase price and expenditures directly attributable to the

acquisition of the asset. PPEs are classified as such in the books when the

acquisition costs are at least Fifty Thousand Pesos (₱50,000.00) per unit, in

accordance with COA Circular No. 2022-004 issued on May 31, 2022.

After recognition, PPE were stated at cost less accumulated depreciation.

The straight-line method was adopted in the computation of depreciation over

the useful life of the asset, assigning a residual value of at least 10%. The

estimated useful life of the asset is based on the estimated useful life of PPE by

classification issued by COA. Depreciation starts on the month following the

date of the purchase.

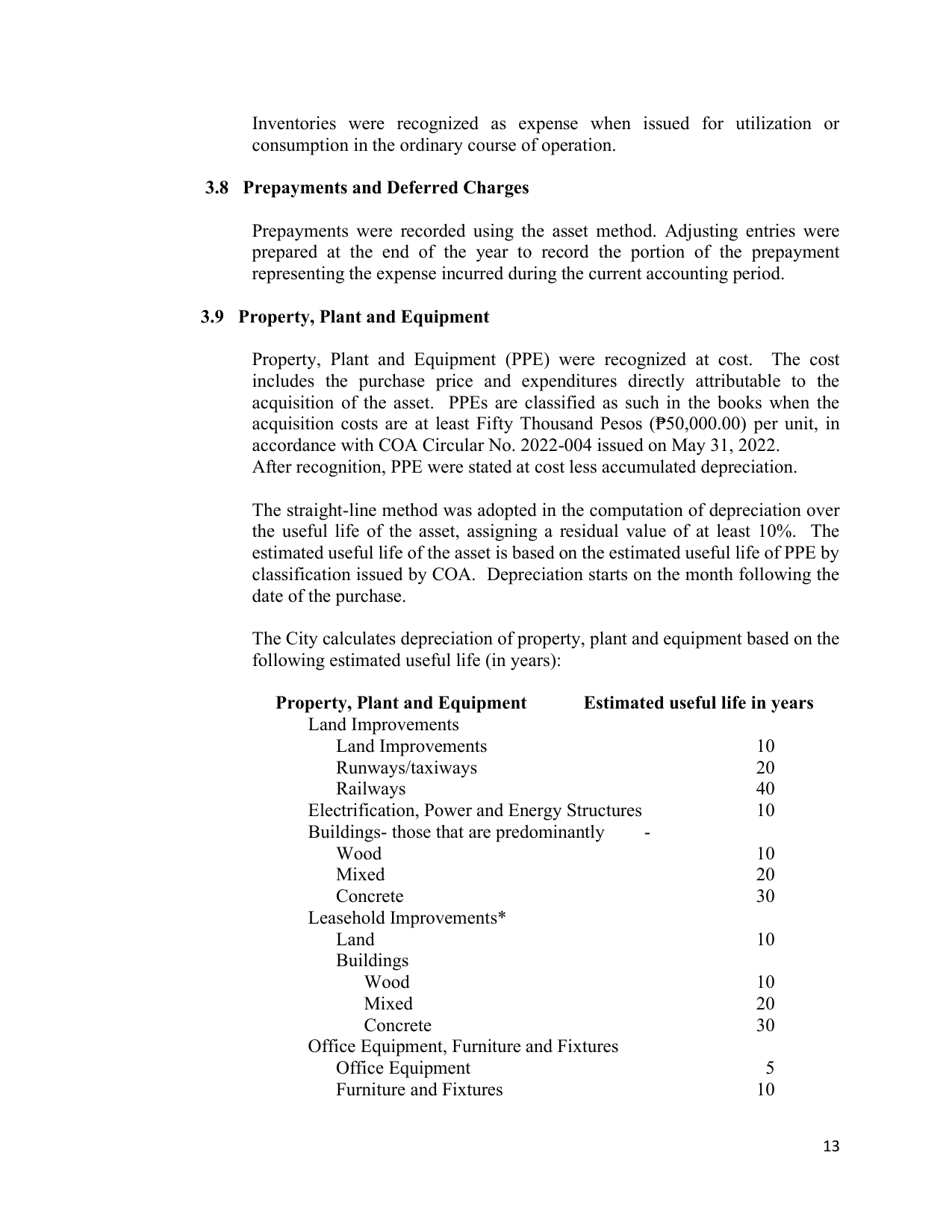

The City calculates depreciation of property, plant and equipment based on the

following estimated useful life (in years):

Property, Plant and Equipment Estimated useful life in years

Land Improvements

Land Improvements 10

Runways/taxiways 20

Railways 40

Electrification, Power and Energy Structures 10

Buildings- those that are predominantly -

Wood 10

Mixed 20

Concrete 30

Leasehold Improvements*

Land 10

Buildings

Wood 10

Mixed 20

Concrete 30

Office Equipment, Furniture and Fixtures

Office Equipment 5

Furniture and Fixtures 10

13