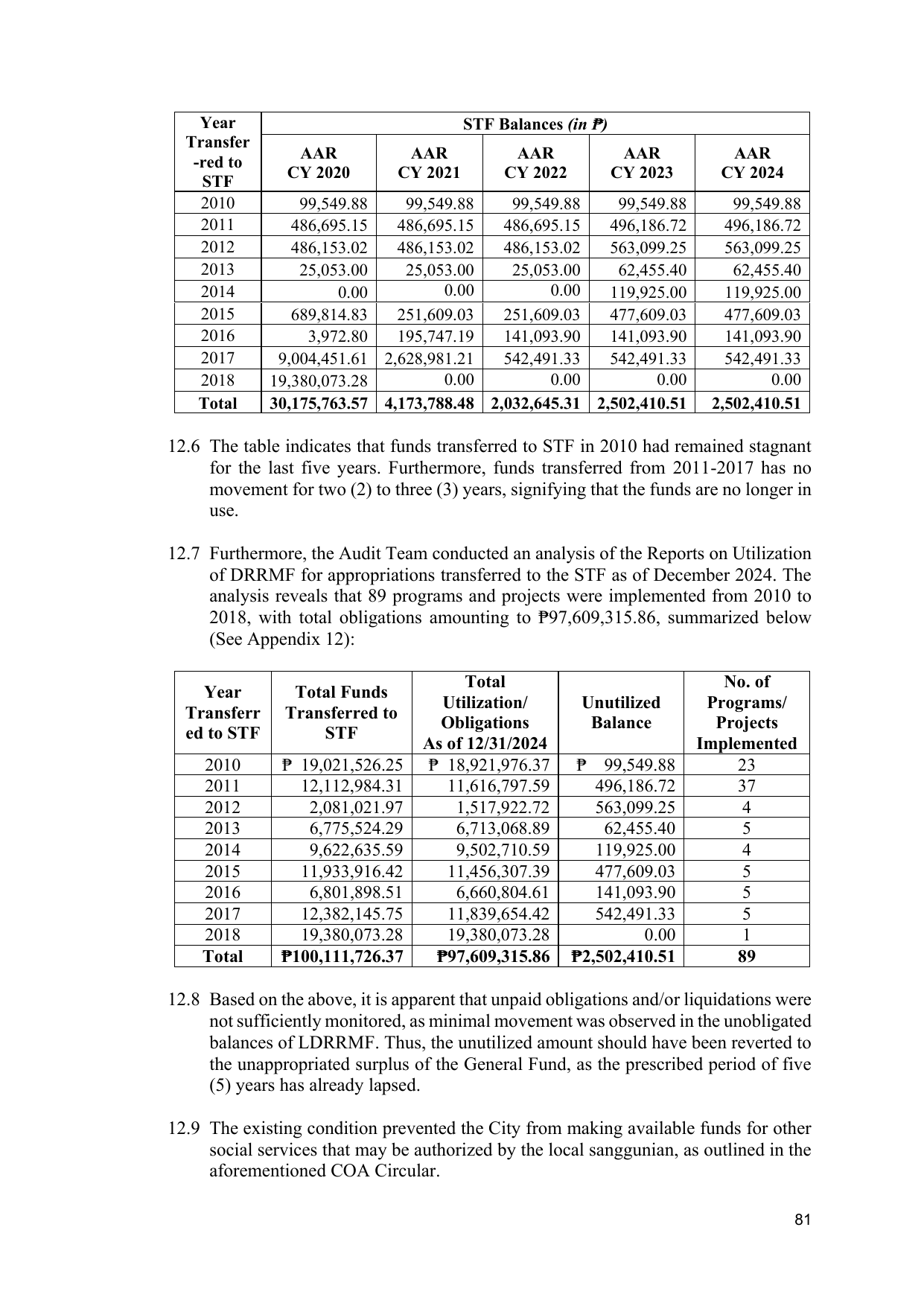

Year STF Balances (in ₱)

Transfer

AAR AAR AAR AAR AAR

-red to

CY 2020 CY 2021 CY 2022 CY 2023 CY 2024

STF

2010 99,549.88 99,549.88 99,549.88 99,549.88 99,549.88

2011 486,695.15 486,695.15 486,695.15 496,186.72 496,186.72

2012 486,153.02 486,153.02 486,153.02 563,099.25 563,099.25

2013 25,053.00 25,053.00 25,053.00 62,455.40 62,455.40

2014 0.00 0.00 0.00 119,925.00 119,925.00

2015 689,814.83 251,609.03 251,609.03 477,609.03 477,609.03

2016 3,972.80 195,747.19 141,093.90 141,093.90 141,093.90

2017 9,004,451.61 2,628,981.21 542,491.33 542,491.33 542,491.33

2018 19,380,073.28 0.00 0.00 0.00 0.00

Total 30,175,763.57 4,173,788.48 2,032,645.31 2,502,410.51 2,502,410.51

12.6 The table indicates that funds transferred to STF in 2010 had remained stagnant

for the last five years. Furthermore, funds transferred from 2011-2017 has no

movement for two (2) to three (3) years, signifying that the funds are no longer in

use.

12.7 Furthermore, the Audit Team conducted an analysis of the Reports on Utilization

of DRRMF for appropriations transferred to the STF as of December 2024. The

analysis reveals that 89 programs and projects were implemented from 2010 to

2018, with total obligations amounting to ₱97,609,315.86, summarized below

(See Appendix 12):

Total No. of

Year Total Funds

Utilization/ Unutilized Programs/

Transferr Transferred to

Obligations Balance Projects

ed to STF STF

As of 12/31/2024 Implemented

2010 ₱ 19,021,526.25 ₱ 18,921,976.37 ₱ 99,549.88 23

2011 12,112,984.31 11,616,797.59 496,186.72 37

2012 2,081,021.97 1,517,922.72 563,099.25 4

2013 6,775,524.29 6,713,068.89 62,455.40 5

2014 9,622,635.59 9,502,710.59 119,925.00 4

2015 11,933,916.42 11,456,307.39 477,609.03 5

2016 6,801,898.51 6,660,804.61 141,093.90 5

2017 12,382,145.75 11,839,654.42 542,491.33 5

2018 19,380,073.28 19,380,073.28 0.00 1

Total ₱100,111,726.37 ₱97,609,315.86 ₱2,502,410.51 89

12.8 Based on the above, it is apparent that unpaid obligations and/or liquidations were

not sufficiently monitored, as minimal movement was observed in the unobligated

balances of LDRRMF. Thus, the unutilized amount should have been reverted to

the unappropriated surplus of the General Fund, as the prescribed period of five

(5) years has already lapsed.

12.9 The existing condition prevented the City from making available funds for other

social services that may be authorized by the local sanggunian, as outlined in the

aforementioned COA Circular.

81