7.2 As such, IPSAS 17, which sets the accounting standards for PPE, states that an

item should be recognized as an asset if, and only if:

a. It is probable that future economic benefits or service potential associated with

the item will flow to the entity; and

b. The cost or fair value of the item can be measured reliably.

7.3 Moreover, Section 4.2 of COA Circular No. 2020-006 dated January 31, 2020,

supplements the recognition criteria stated in IPSAS 17, to wit:

a. Beneficial ownership and control clearly rest with the government;

b. The asset is used to achieve government objectives; and

c. It meets the capitalization threshold of ₱50,000.00.9

7.4 Additionally, paragraph 29 of IPSAS 1 requires an entity to present information

that is relevant, reliable, comparable, and understandable. Understandability, as

discussed in the same standard, is the quality of information that enables users

to comprehend its meaning. It is enhanced when information is classified,

characterized, and presented clearly and concisely.

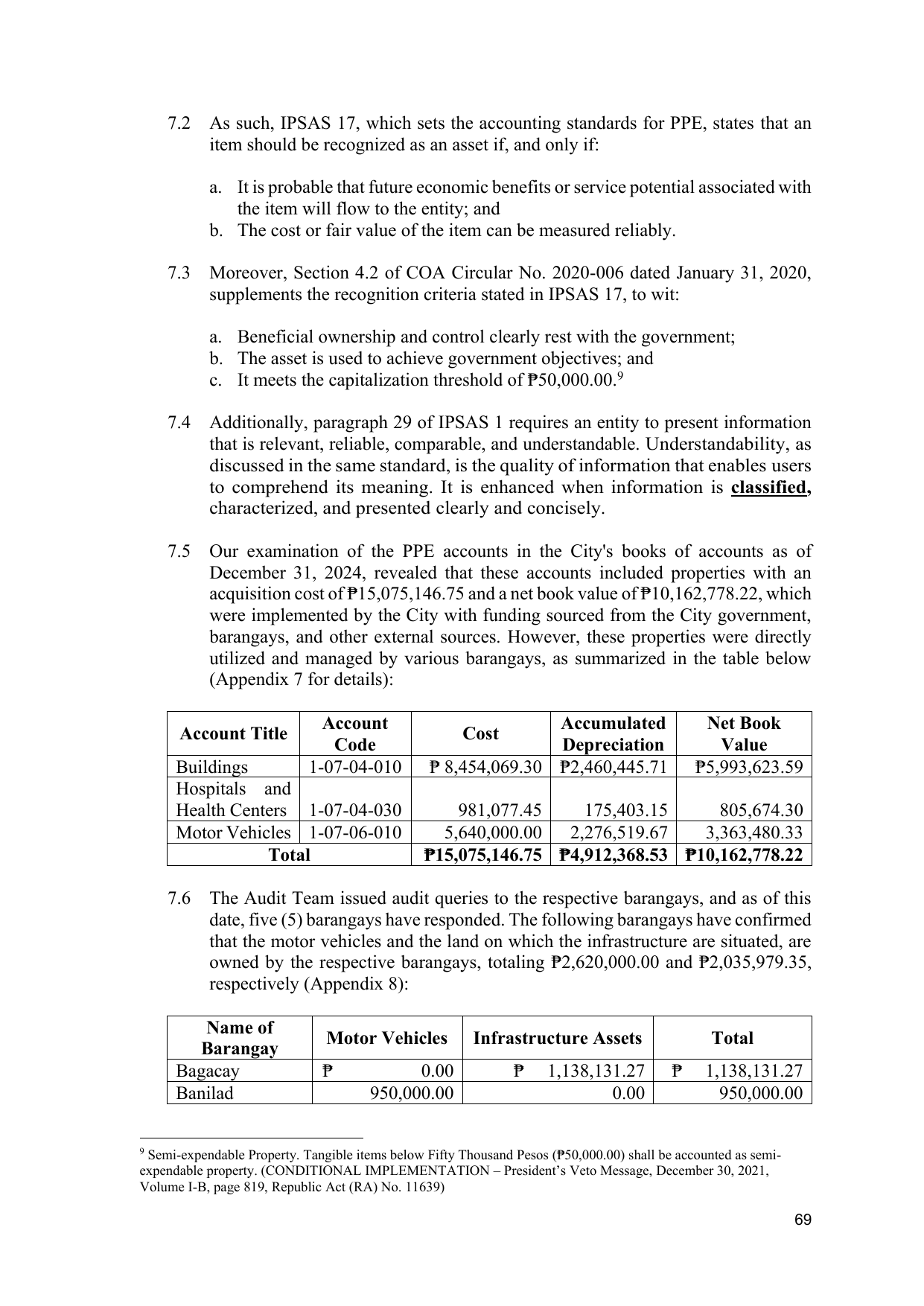

7.5 Our examination of the PPE accounts in the City's books of accounts as of

December 31, 2024, revealed that these accounts included properties with an

acquisition cost of ₱15,075,146.75 and a net book value of ₱10,162,778.22, which

were implemented by the City with funding sourced from the City government,

barangays, and other external sources. However, these properties were directly

utilized and managed by various barangays, as summarized in the table below

(Appendix 7 for details):

Account Accumulated Net Book

Account Title Cost

Code Depreciation Value

Buildings 1-07-04-010 ₱ 8,454,069.30 ₱2,460,445.71 ₱5,993,623.59

Hospitals and

Health Centers 1-07-04-030 981,077.45 175,403.15 805,674.30

Motor Vehicles 1-07-06-010 5,640,000.00 2,276,519.67 3,363,480.33

Total ₱15,075,146.75 ₱4,912,368.53 ₱10,162,778.22

7.6 The Audit Team issued audit queries to the respective barangays, and as of this

date, five (5) barangays have responded. The following barangays have confirmed

that the motor vehicles and the land on which the infrastructure are situated, are

owned by the respective barangays, totaling ₱2,620,000.00 and ₱2,035,979.35,

respectively (Appendix 8):

Name of

Motor Vehicles Infrastructure Assets Total

Barangay

Bagacay ₱ 0.00 ₱ 1,138,131.27 ₱ 1,138,131.27

Banilad 950,000.00 0.00 950,000.00

9 Semi-expendable Property. Tangible items below Fifty Thousand Pesos (₱50,000.00) shall be accounted as semi-

expendable property. (CONDITIONAL IMPLEMENTATION – President’s Veto Message, December 30, 2021,

Volume I-B, page 819, Republic Act (RA) No. 11639)

69