balance. While a 1.27 per cent and 5.05 per cent drop was observed in

2021 and 2022, respectively—attributable to credit transactions related to

housing projects—only a 0.58 per cent to 0.39 per cent downward trend

was noted from 2023 to 2024. This highlights the continued slow pace of

liquidation and weak monitoring, especially considering the long-standing

age of these transfers. With fund transfers ranging from six (6) to 30 years

old, the likelihood of settlement appears remote.

4.4.4. Additionally, financial records revealed no impairment allowances were

established for this account, which could signal an oversight in addressing

the potential risk of non-recovery of these receivables.

b. Inadequate monitoring, missing documents, and non-submission of liquidation

reports

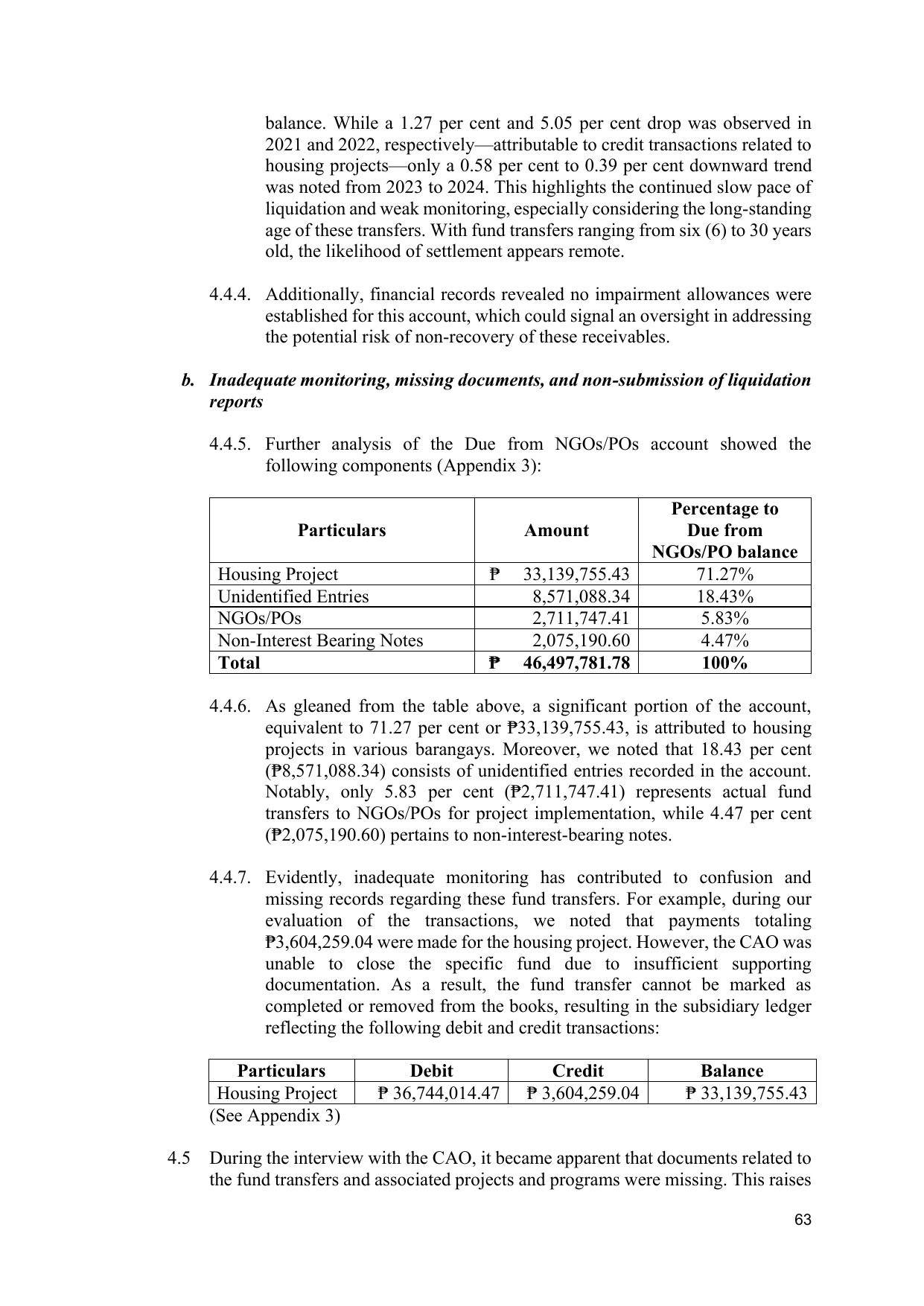

4.4.5. Further analysis of the Due from NGOs/POs account showed the

following components (Appendix 3):

Percentage to

Particulars Amount Due from

NGOs/PO balance

Housing Project ₱ 33,139,755.43 71.27%

Unidentified Entries 8,571,088.34 18.43%

NGOs/POs 2,711,747.41 5.83%

Non-Interest Bearing Notes 2,075,190.60 4.47%

Total ₱ 46,497,781.78 100%

4.4.6. As gleaned from the table above, a significant portion of the account,

equivalent to 71.27 per cent or ₱33,139,755.43, is attributed to housing

projects in various barangays. Moreover, we noted that 18.43 per cent

(₱8,571,088.34) consists of unidentified entries recorded in the account.

Notably, only 5.83 per cent (₱2,711,747.41) represents actual fund

transfers to NGOs/POs for project implementation, while 4.47 per cent

(₱2,075,190.60) pertains to non-interest-bearing notes.

4.4.7. Evidently, inadequate monitoring has contributed to confusion and

missing records regarding these fund transfers. For example, during our

evaluation of the transactions, we noted that payments totaling

₱3,604,259.04 were made for the housing project. However, the CAO was

unable to close the specific fund due to insufficient supporting

documentation. As a result, the fund transfer cannot be marked as

completed or removed from the books, resulting in the subsidiary ledger

reflecting the following debit and credit transactions:

Particulars Debit Credit Balance

Housing Project ₱ 36,744,014.47 ₱ 3,604,259.04 ₱ 33,139,755.43

(See Appendix 3)

4.5 During the interview with the CAO, it became apparent that documents related to

the fund transfers and associated projects and programs were missing. This raises

63