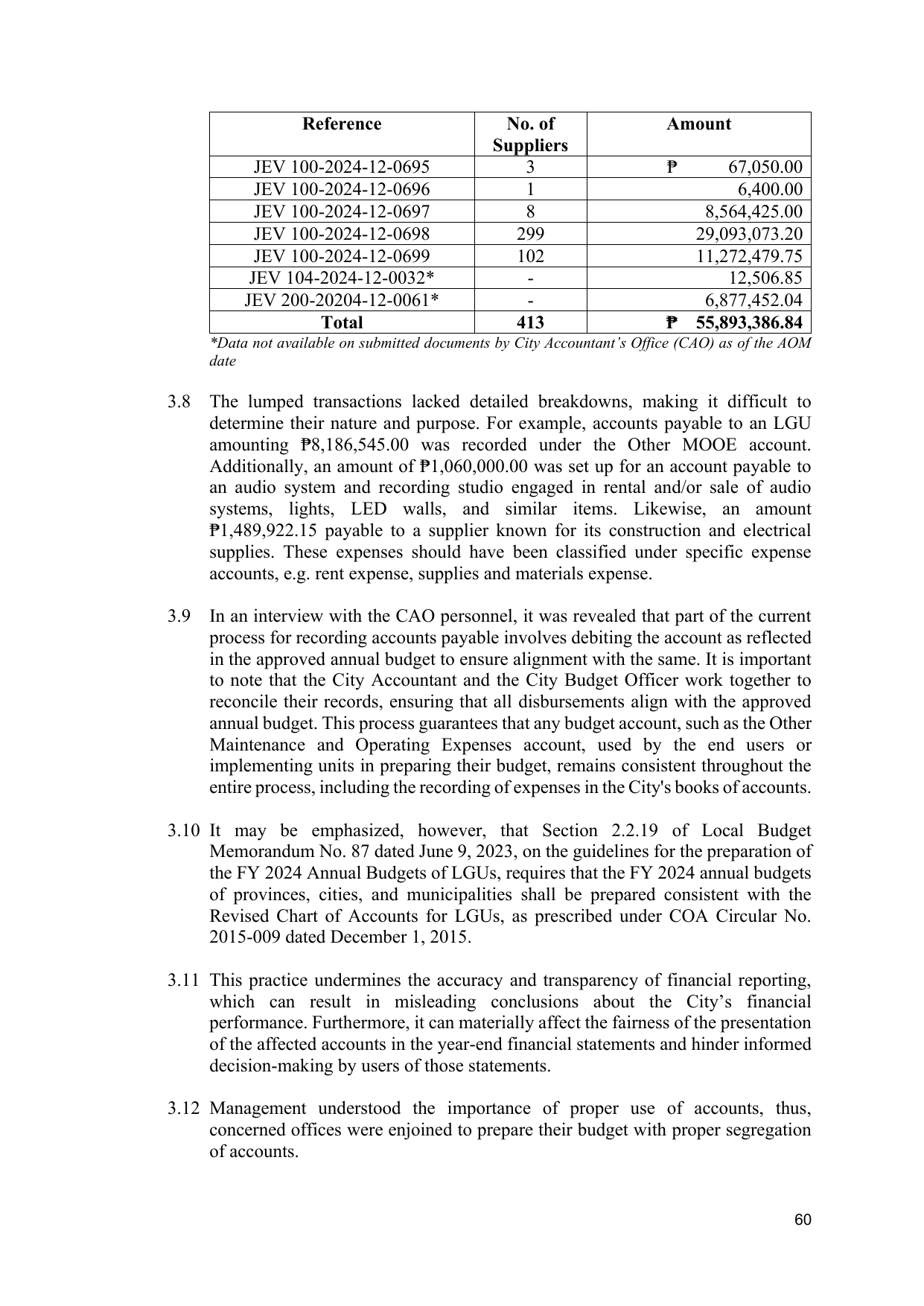

Reference No. of Amount

Suppliers

JEV 100-2024-12-0695 3 ₱ 67,050.00

JEV 100-2024-12-0696 1 6,400.00

JEV 100-2024-12-0697 8 8,564,425.00

JEV 100-2024-12-0698 299 29,093,073.20

JEV 100-2024-12-0699 102 11,272,479.75

JEV 104-2024-12-0032* - 12,506.85

JEV 200-20204-12-0061* - 6,877,452.04

Total 413 ₱ 55,893,386.84

*Data not available on submitted documents by City Accountant’s Office (CAO) as of the AOM

date

3.8 The lumped transactions lacked detailed breakdowns, making it difficult to

determine their nature and purpose. For example, accounts payable to an LGU

amounting ₱8,186,545.00 was recorded under the Other MOOE account.

Additionally, an amount of ₱1,060,000.00 was set up for an account payable to

an audio system and recording studio engaged in rental and/or sale of audio

systems, lights, LED walls, and similar items. Likewise, an amount

₱1,489,922.15 payable to a supplier known for its construction and electrical

supplies. These expenses should have been classified under specific expense

accounts, e.g. rent expense, supplies and materials expense.

3.9 In an interview with the CAO personnel, it was revealed that part of the current

process for recording accounts payable involves debiting the account as reflected

in the approved annual budget to ensure alignment with the same. It is important

to note that the City Accountant and the City Budget Officer work together to

reconcile their records, ensuring that all disbursements align with the approved

annual budget. This process guarantees that any budget account, such as the Other

Maintenance and Operating Expenses account, used by the end users or

implementing units in preparing their budget, remains consistent throughout the

entire process, including the recording of expenses in the City's books of accounts.

3.10 It may be emphasized, however, that Section 2.2.19 of Local Budget

Memorandum No. 87 dated June 9, 2023, on the guidelines for the preparation of

the FY 2024 Annual Budgets of LGUs, requires that the FY 2024 annual budgets

of provinces, cities, and municipalities shall be prepared consistent with the

Revised Chart of Accounts for LGUs, as prescribed under COA Circular No.

2015-009 dated December 1, 2015.

3.11 This practice undermines the accuracy and transparency of financial reporting,

which can result in misleading conclusions about the City’s financial

performance. Furthermore, it can materially affect the fairness of the presentation

of the affected accounts in the year-end financial statements and hinder informed

decision-making by users of those statements.

3.12 Management understood the importance of proper use of accounts, thus,

concerned offices were enjoined to prepare their budget with proper segregation

of accounts.

60