c) Use of RIS for the issuance of supplies and materials not executed

1.3.7. Section 116 of the Manual on NGAS states that requisitions for supplies

and materials shall be accomplished using the RIS for supplies carried in

stock and Purchase Request (PR) for supplies not carried in stock.

1.3.8. Likewise, Section 121 thereof further states that the General Services

Officer shall consolidate weekly the RIS using the Summary of Supplies

and Materials Issued (SSMI). The SSMI shall be submitted to the Chief

Accountant for proper recording of expenditures using appropriate

expenditure accounts.

1.3.9. Further validation of prior years’ audit recommendations revealed that

CGSO has not yet fully implemented the use of the RIS form, and there

has been no consolidation of all RIS in the SSMI. Evidently, SSMI was

not submitted to the City Accountant’s Office (CAO) for proper recording.

d) Inclusion of dormant items totaling ₱19,815,169.11

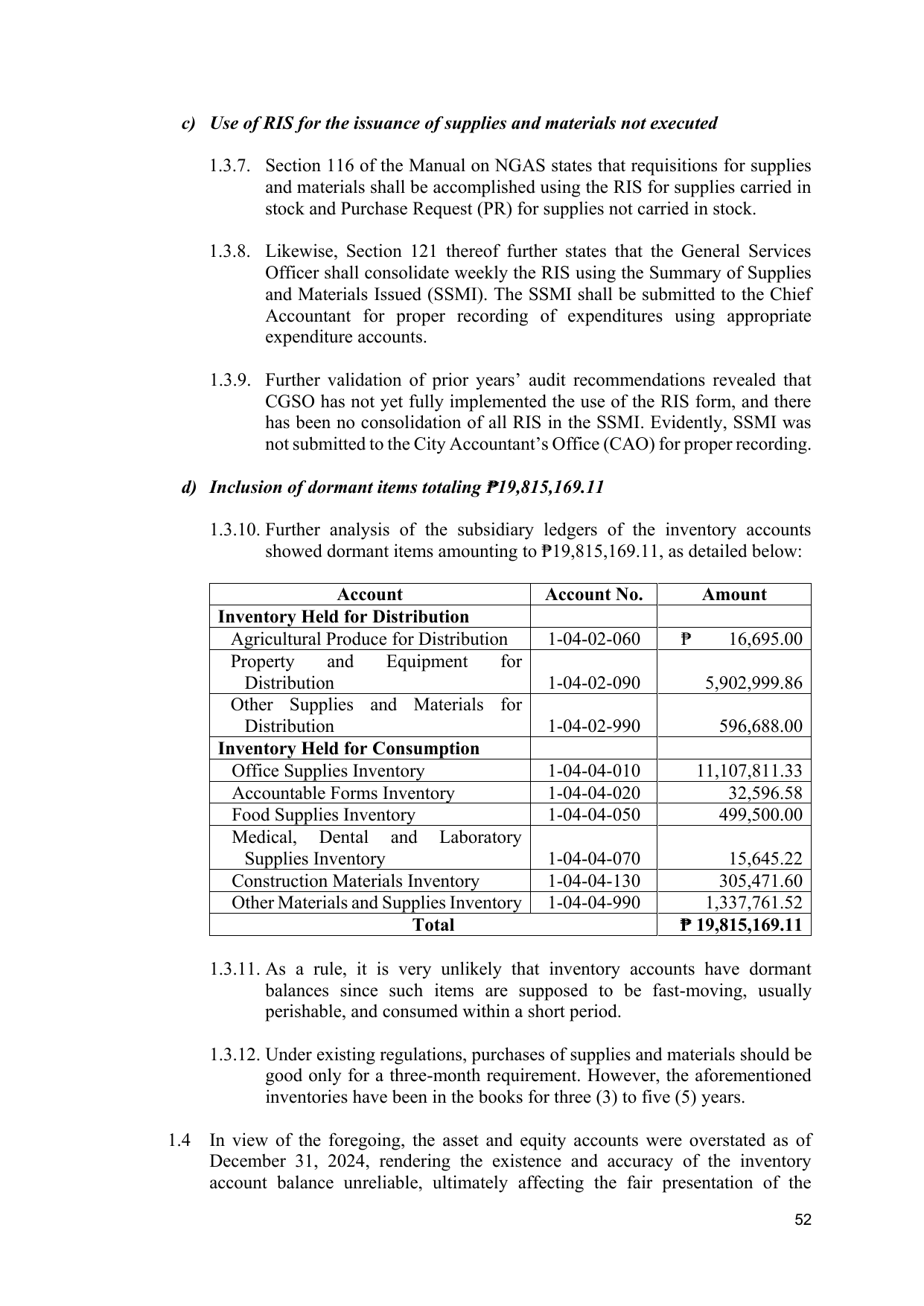

1.3.10. Further analysis of the subsidiary ledgers of the inventory accounts

showed dormant items amounting to ₱19,815,169.11, as detailed below:

Account Account No. Amount

Inventory Held for Distribution

Agricultural Produce for Distribution 1-04-02-060 ₱ 16,695.00

Property and Equipment for

Distribution 1-04-02-090 5,902,999.86

Other Supplies and Materials for

Distribution 1-04-02-990 596,688.00

Inventory Held for Consumption

Office Supplies Inventory 1-04-04-010 11,107,811.33

Accountable Forms Inventory 1-04-04-020 32,596.58

Food Supplies Inventory 1-04-04-050 499,500.00

Medical, Dental and Laboratory

Supplies Inventory 1-04-04-070 15,645.22

Construction Materials Inventory 1-04-04-130 305,471.60

Other Materials and Supplies Inventory 1-04-04-990 1,337,761.52

Total ₱ 19,815,169.11

1.3.11. As a rule, it is very unlikely that inventory accounts have dormant

balances since such items are supposed to be fast-moving, usually

perishable, and consumed within a short period.

1.3.12. Under existing regulations, purchases of supplies and materials should be

good only for a three-month requirement. However, the aforementioned

inventories have been in the books for three (3) to five (5) years.

1.4 In view of the foregoing, the asset and equity accounts were overstated as of

December 31, 2024, rendering the existence and accuracy of the inventory

account balance unreliable, ultimately affecting the fair presentation of the

52