AUDIT OBSERVATIONS AND RECOMMENDATIONS

FINANCIAL AUDIT

Inventory totaling ₱109,420,217.02 cannot be fully ascertained

1. The existence and accuracy of the inventory accounts totaling ₱109,420,217.02 as

of December 31, 2024 could not be fully ascertained because of the non-conduct of

a physical count of inventories, incomplete report of issuances, incomplete

Supplies Ledger Cards (SLCs) and Stock Cards (SCs), and inclusion of dormant

items amounting ₱19,815,169.11, thus, overstating the asset and equity accounts.

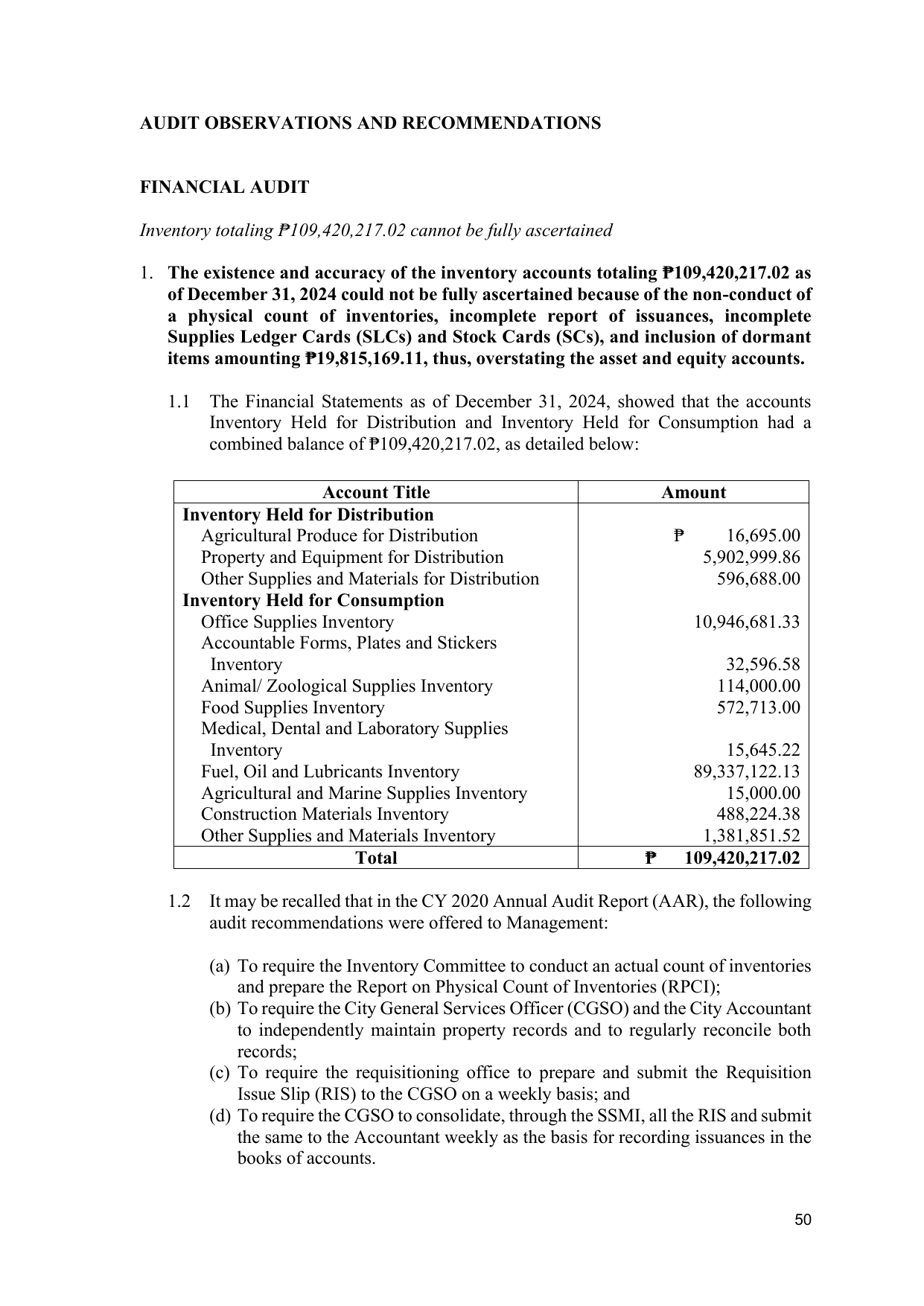

1.1 The Financial Statements as of December 31, 2024, showed that the accounts

Inventory Held for Distribution and Inventory Held for Consumption had a

combined balance of ₱109,420,217.02, as detailed below:

Account Title Amount

Inventory Held for Distribution

Agricultural Produce for Distribution ₱ 16,695.00

Property and Equipment for Distribution 5,902,999.86

Other Supplies and Materials for Distribution 596,688.00

Inventory Held for Consumption

Office Supplies Inventory 10,946,681.33

Accountable Forms, Plates and Stickers

Inventory 32,596.58

Animal/ Zoological Supplies Inventory 114,000.00

Food Supplies Inventory 572,713.00

Medical, Dental and Laboratory Supplies

Inventory 15,645.22

Fuel, Oil and Lubricants Inventory 89,337,122.13

Agricultural and Marine Supplies Inventory 15,000.00

Construction Materials Inventory 488,224.38

Other Supplies and Materials Inventory 1,381,851.52

Total ₱ 109,420,217.02

1.2 It may be recalled that in the CY 2020 Annual Audit Report (AAR), the following

audit recommendations were offered to Management:

(a) To require the Inventory Committee to conduct an actual count of inventories

and prepare the Report on Physical Count of Inventories (RPCI);

(b) To require the City General Services Officer (CGSO) and the City Accountant

to independently maintain property records and to regularly reconcile both

records;

(c) To require the requisitioning office to prepare and submit the Requisition

Issue Slip (RIS) to the CGSO on a weekly basis; and

(d) To require the CGSO to consolidate, through the SSMI, all the RIS and submit

the same to the Accountant weekly as the basis for recording issuances in the

books of accounts.

50