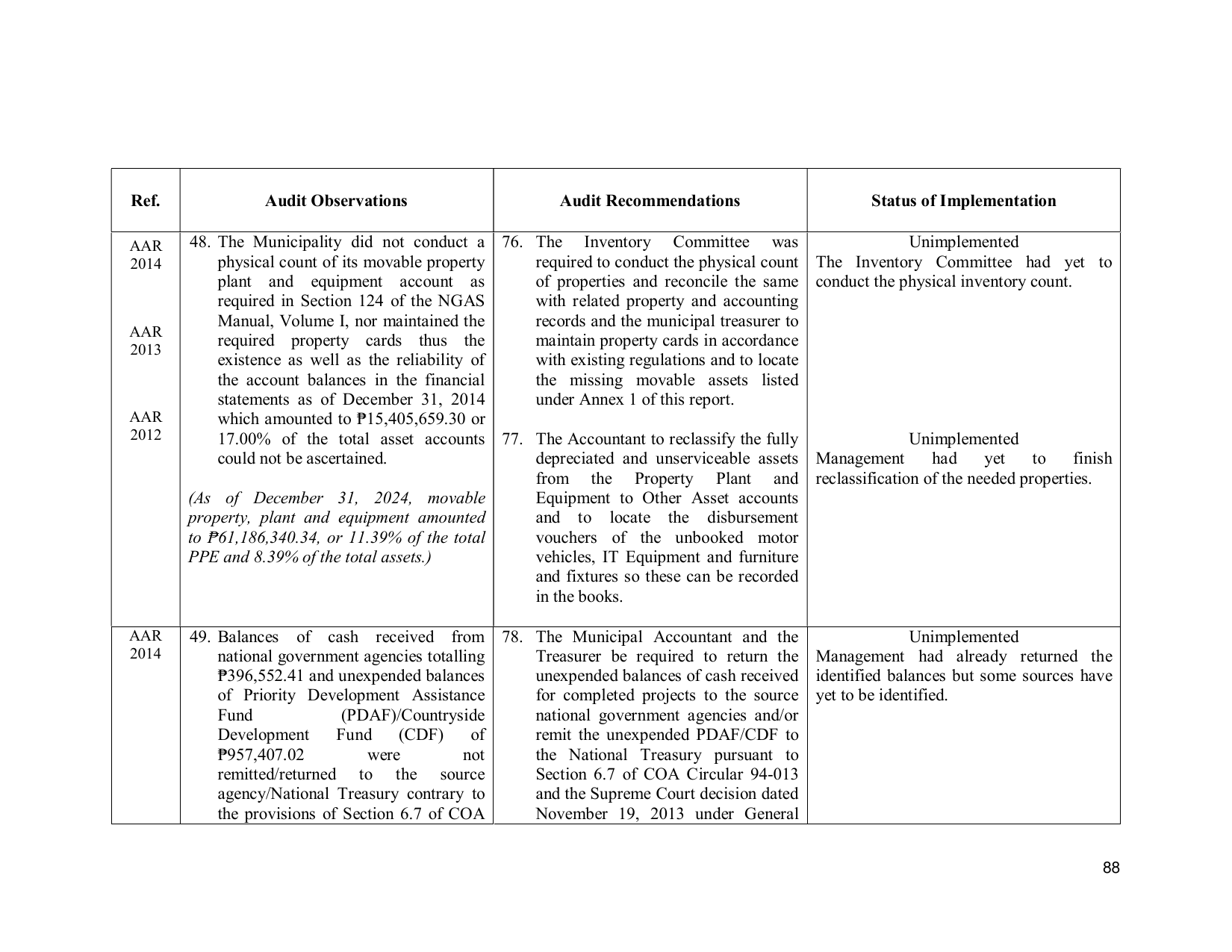

Ref. Audit Observations Audit Recommendations Status of Implementation

AAR 48. The Municipality did not conduct a 76. The Inventory Committee was Unimplemented

2014 physical count of its movable property required to conduct the physical count The Inventory Committee had yet to

plant and equipment account as of properties and reconcile the same conduct the physical inventory count.

required in Section 124 of the NGAS with related property and accounting

Manual, Volume I, nor maintained the records and the municipal treasurer to

AAR

2013

required property cards thus the maintain property cards in accordance

existence as well as the reliability of with existing regulations and to locate

the account balances in the financial the missing movable assets listed

statements as of December 31, 2014 under Annex 1 of this report.

AAR which amounted to ₱15,405,659.30 or

2012 17.00% of the total asset accounts 77. The Accountant to reclassify the fully Unimplemented

could not be ascertained. depreciated and unserviceable assets Management had yet to finish

from the Property Plant and reclassification of the needed properties.

(As of December 31, 2024, movable Equipment to Other Asset accounts

property, plant and equipment amounted and to locate the disbursement

to ₱61,186,340.34, or 11.39% of the total vouchers of the unbooked motor

PPE and 8.39% of the total assets.) vehicles, IT Equipment and furniture

and fixtures so these can be recorded

in the books.

AAR 49. Balances of cash received from 78. The Municipal Accountant and the Unimplemented

2014 national government agencies totalling Treasurer be required to return the Management had already returned the

₱396,552.41 and unexpended balances unexpended balances of cash received identified balances but some sources have

of Priority Development Assistance for completed projects to the source yet to be identified.

Fund (PDAF)/Countryside national government agencies and/or

Development Fund (CDF) of remit the unexpended PDAF/CDF to

₱957,407.02 were not the National Treasury pursuant to

remitted/returned to the source Section 6.7 of COA Circular 94-013

agency/National Treasury contrary to and the Supreme Court decision dated

the provisions of Section 6.7 of COA November 19, 2013 under General

88