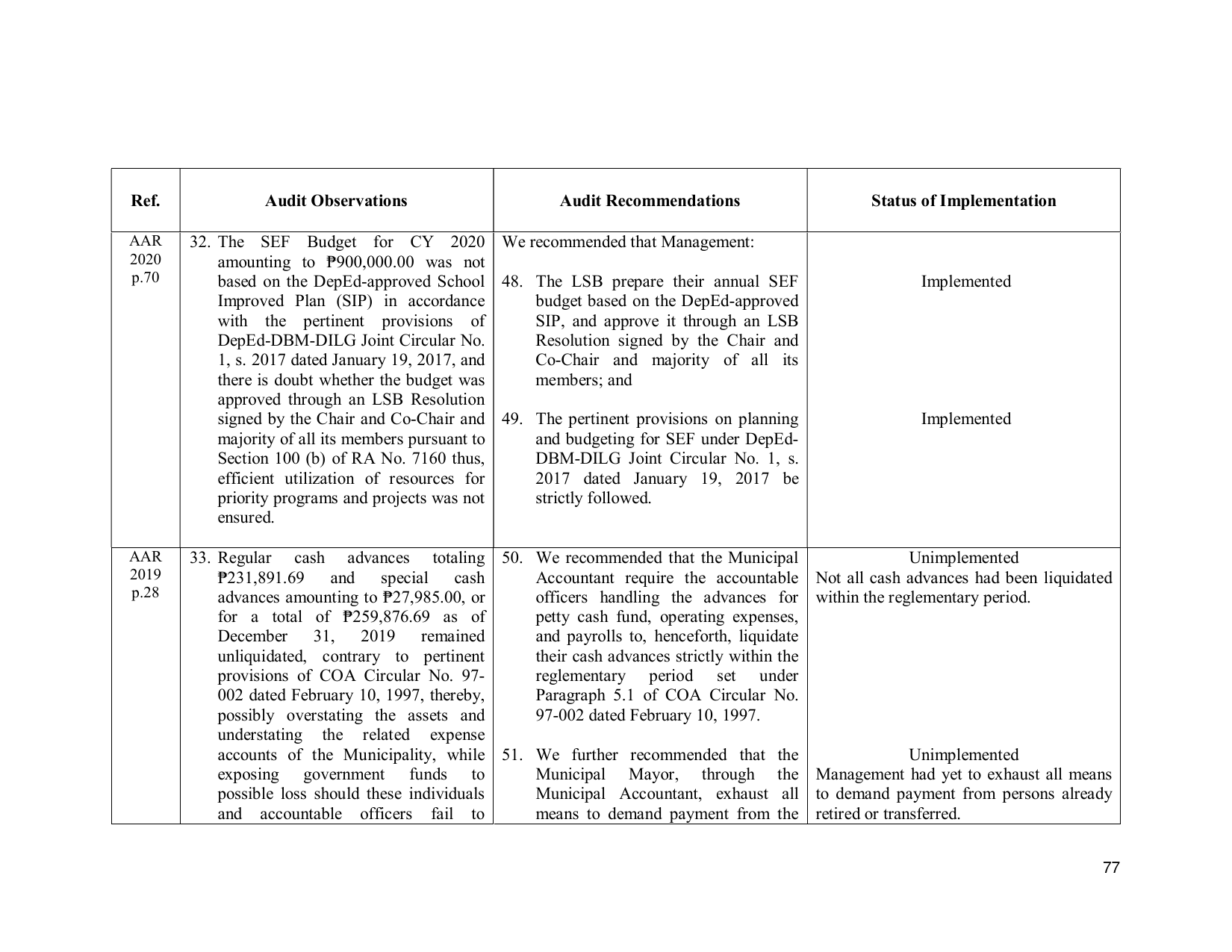

Ref. Audit Observations Audit Recommendations Status of Implementation

AAR 32. The SEF Budget for CY 2020 We recommended that Management:

2020 amounting to ₱900,000.00 was not

p.70 based on the DepEd-approved School 48. The LSB prepare their annual SEF Implemented

Improved Plan (SIP) in accordance budget based on the DepEd-approved

with the pertinent provisions of SIP, and approve it through an LSB

DepEd-DBM-DILG Joint Circular No. Resolution signed by the Chair and

1, s. 2017 dated January 19, 2017, and Co-Chair and majority of all its

there is doubt whether the budget was members; and

approved through an LSB Resolution

signed by the Chair and Co-Chair and 49. The pertinent provisions on planning Implemented

majority of all its members pursuant to and budgeting for SEF under DepEd-

Section 100 (b) of RA No. 7160 thus, DBM-DILG Joint Circular No. 1, s.

efficient utilization of resources for 2017 dated January 19, 2017 be

priority programs and projects was not strictly followed.

ensured.

AAR 33. Regular cash advances totaling 50. We recommended that the Municipal Unimplemented

2019 ₱231,891.69 and special cash Accountant require the accountable Not all cash advances had been liquidated

p.28 advances amounting to ₱27,985.00, or officers handling the advances for within the reglementary period.

for a total of ₱259,876.69 as of petty cash fund, operating expenses,

December 31, 2019 remained and payrolls to, henceforth, liquidate

unliquidated, contrary to pertinent their cash advances strictly within the

provisions of COA Circular No. 97- reglementary period set under

002 dated February 10, 1997, thereby, Paragraph 5.1 of COA Circular No.

possibly overstating the assets and 97-002 dated February 10, 1997.

understating the related expense

accounts of the Municipality, while 51. We further recommended that the Unimplemented

exposing government funds to Municipal Mayor, through the Management had yet to exhaust all means

possible loss should these individuals Municipal Accountant, exhaust all to demand payment from persons already

and accountable officers fail to means to demand payment from the retired or transferred.

77