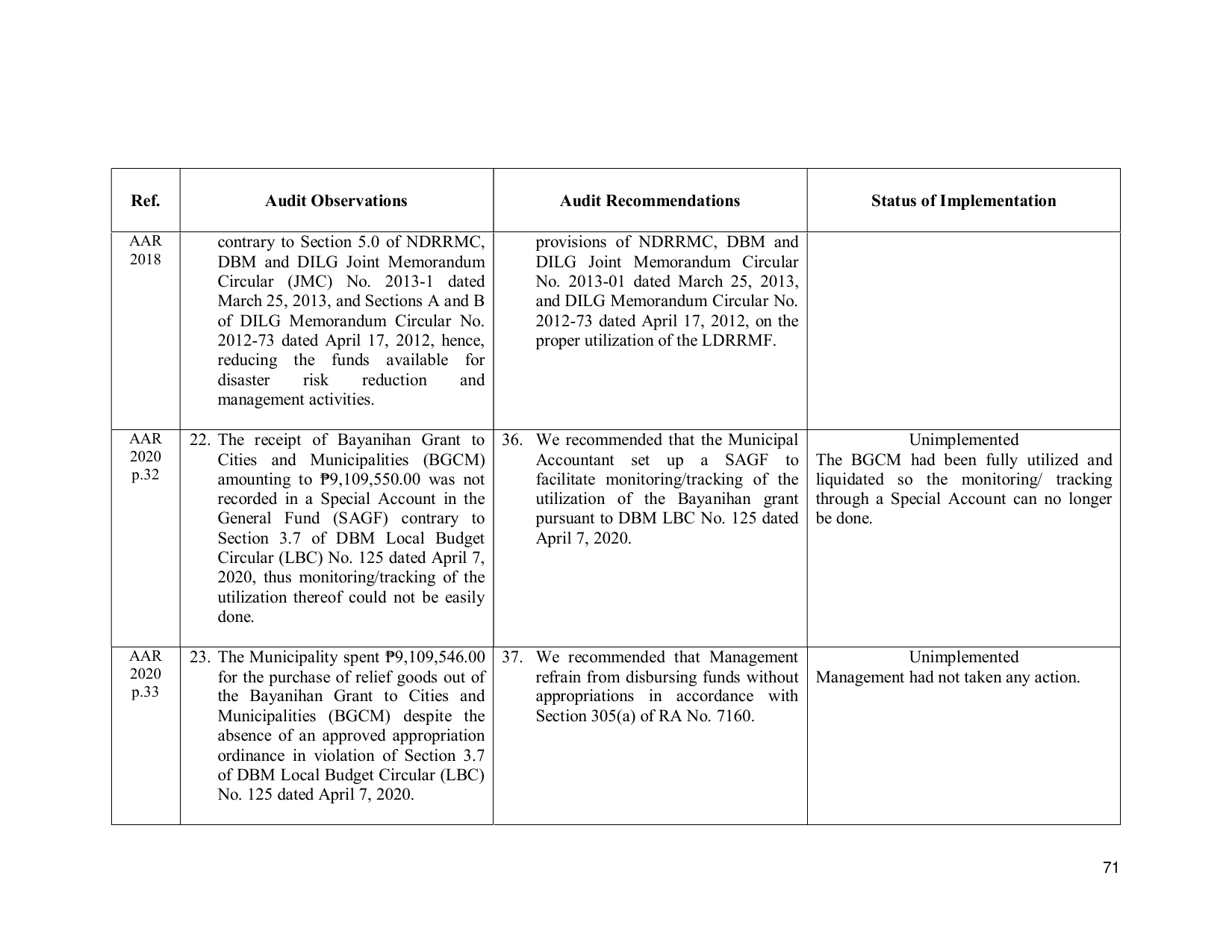

Ref. Audit Observations Audit Recommendations Status of Implementation

AAR contrary to Section 5.0 of NDRRMC, provisions of NDRRMC, DBM and

2018 DBM and DILG Joint Memorandum DILG Joint Memorandum Circular

Circular (JMC) No. 2013-1 dated No. 2013-01 dated March 25, 2013,

March 25, 2013, and Sections A and B and DILG Memorandum Circular No.

of DILG Memorandum Circular No. 2012-73 dated April 17, 2012, on the

2012-73 dated April 17, 2012, hence, proper utilization of the LDRRMF.

reducing the funds available for

disaster risk reduction and

management activities.

AAR 22. The receipt of Bayanihan Grant to 36. We recommended that the Municipal Unimplemented

2020 Cities and Municipalities (BGCM) Accountant set up a SAGF to The BGCM had been fully utilized and

p.32 amounting to ₱9,109,550.00 was not facilitate monitoring/tracking of the liquidated so the monitoring/ tracking

recorded in a Special Account in the utilization of the Bayanihan grant through a Special Account can no longer

General Fund (SAGF) contrary to pursuant to DBM LBC No. 125 dated be done.

Section 3.7 of DBM Local Budget April 7, 2020.

Circular (LBC) No. 125 dated April 7,

2020, thus monitoring/tracking of the

utilization thereof could not be easily

done.

AAR 23. The Municipality spent ₱9,109,546.00 37. We recommended that Management Unimplemented

2020 for the purchase of relief goods out of refrain from disbursing funds without Management had not taken any action.

p.33 the Bayanihan Grant to Cities and appropriations in accordance with

Municipalities (BGCM) despite the Section 305(a) of RA No. 7160.

absence of an approved appropriation

ordinance in violation of Section 3.7

of DBM Local Budget Circular (LBC)

No. 125 dated April 7, 2020.

71