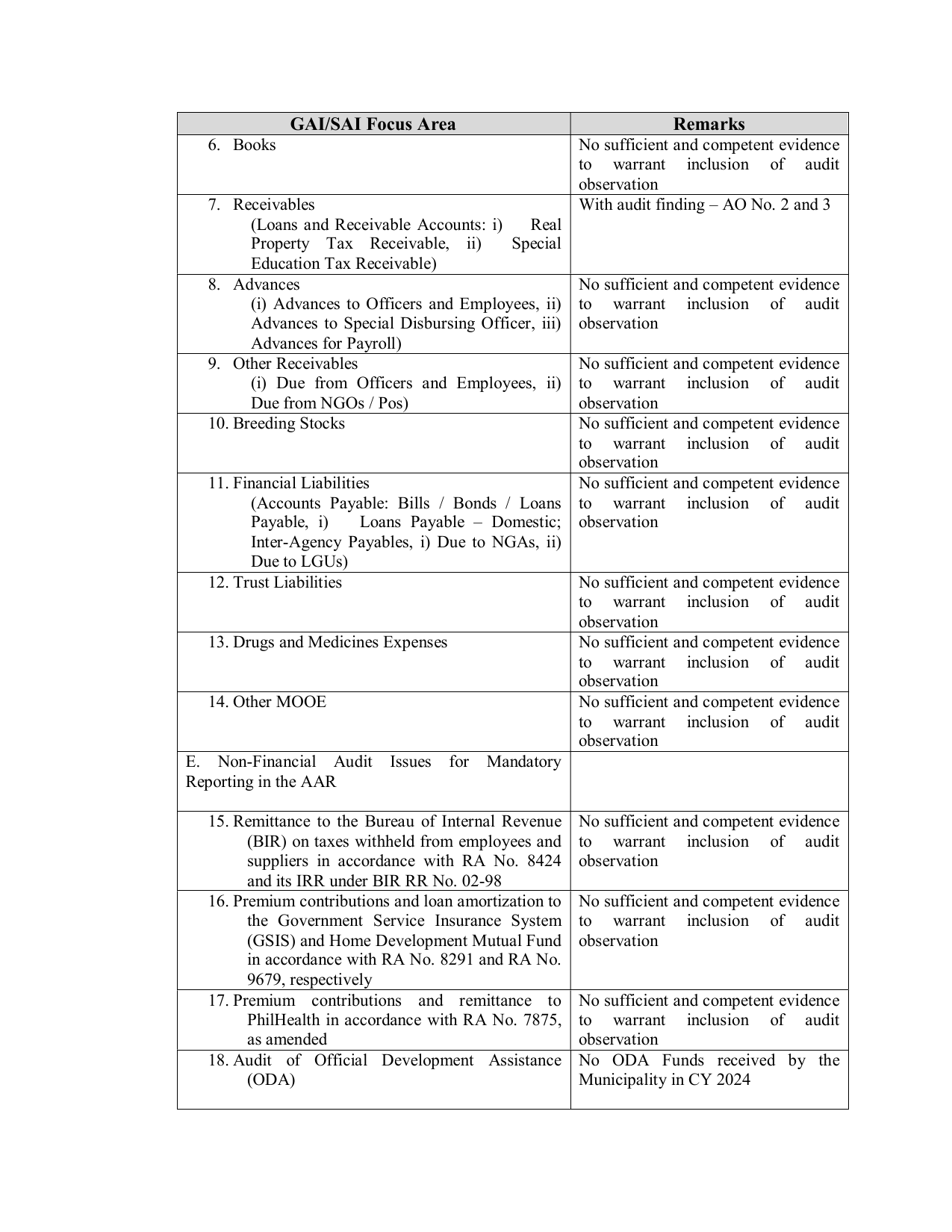

GAI/SAI Focus Area Remarks

6. Books No sufficient and competent evidence

to warrant inclusion of audit

observation

7. Receivables With audit finding – AO No. 2 and 3

(Loans and Receivable Accounts: i) Real

Property Tax Receivable, ii) Special

Education Tax Receivable)

8. Advances No sufficient and competent evidence

(i) Advances to Officers and Employees, ii) to warrant inclusion of audit

Advances to Special Disbursing Officer, iii) observation

Advances for Payroll)

9. Other Receivables No sufficient and competent evidence

(i) Due from Officers and Employees, ii) to warrant inclusion of audit

Due from NGOs / Pos) observation

10. Breeding Stocks No sufficient and competent evidence

to warrant inclusion of audit

observation

11. Financial Liabilities No sufficient and competent evidence

(Accounts Payable: Bills / Bonds / Loans to warrant inclusion of audit

Payable, i) Loans Payable – Domestic; observation

Inter-Agency Payables, i) Due to NGAs, ii)

Due to LGUs)

12. Trust Liabilities No sufficient and competent evidence

to warrant inclusion of audit

observation

13. Drugs and Medicines Expenses No sufficient and competent evidence

to warrant inclusion of audit

observation

14. Other MOOE No sufficient and competent evidence

to warrant inclusion of audit

observation

E. Non-Financial Audit Issues for Mandatory

Reporting in the AAR

15. Remittance to the Bureau of Internal Revenue No sufficient and competent evidence

(BIR) on taxes withheld from employees and to warrant inclusion of audit

suppliers in accordance with RA No. 8424 observation

and its IRR under BIR RR No. 02-98

16. Premium contributions and loan amortization to No sufficient and competent evidence

the Government Service Insurance System to warrant inclusion of audit

(GSIS) and Home Development Mutual Fund observation

in accordance with RA No. 8291 and RA No.

9679, respectively

17. Premium contributions and remittance to No sufficient and competent evidence

PhilHealth in accordance with RA No. 7875, to warrant inclusion of audit

as amended observation

18. Audit of Official Development Assistance No ODA Funds received by the

(ODA) Municipality in CY 2024