LDRRM Erroneous Accounting Entries

5. Payments for various LDRRM supplies and equipment were incorrectly recorded,

resulting in the overstatement of Other Supplies and Materials Inventory

(₱168,334.00), Other Property, Plant and Equipment (₱99,500.00), and Other

MOOE (₱40,250.00), and the understatement of Semi-Expendable Disaster

Response and Rescue Equipment (₱109,595.00) and Disaster Response and Rescue

Equipment (₱198,489.00), thereby affecting the accuracy of the financial statements

as of December 31, 2024.

5.1 COA Circular No. 2012-002 dated September 12, 2012, provides for the accounting

and reporting guidelines for the Local Disaster Risk Reduction and Management

Fund (LDRRMF) of LGUs, National DRRM Fund given to LGUs, and receipts from

other sources. Section 5.1.7 thereof states, “Equipment purchased for disaster

response and rescue operations or activities shall be recorded in the General Fund

books of accounts using the account Disaster Response and Rescue Equipment.”

5.2 COA Circular No. 2015-009 dated December 1, 2015, prescribes the Revised Chart

of Accounts for Local Government Units to record and report the financial

transactions of LGUs. Annex B thereof contains the description of accounts and the

instructions, which partly provides:

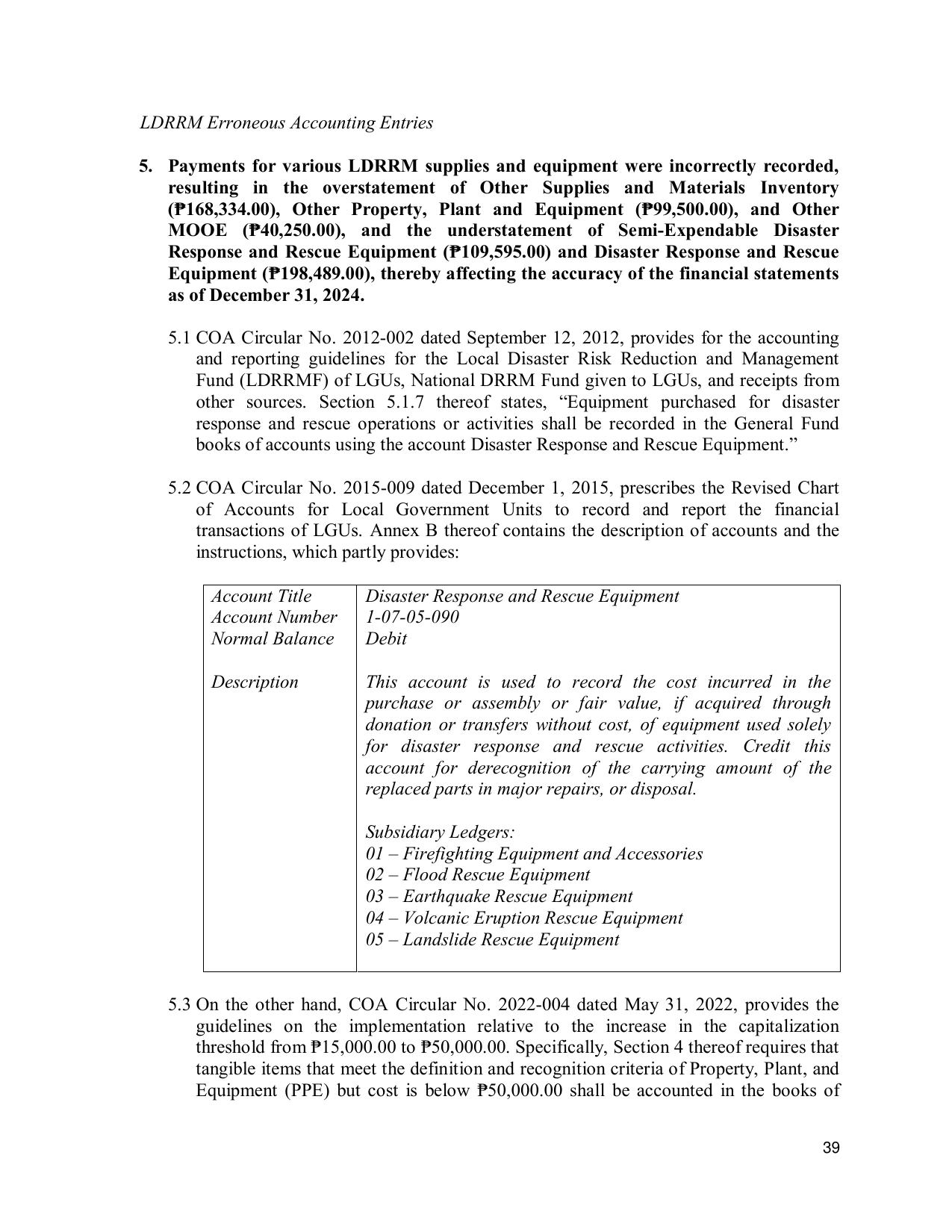

Account Title Disaster Response and Rescue Equipment

Account Number 1-07-05-090

Normal Balance Debit

Description This account is used to record the cost incurred in the

purchase or assembly or fair value, if acquired through

donation or transfers without cost, of equipment used solely

for disaster response and rescue activities. Credit this

account for derecognition of the carrying amount of the

replaced parts in major repairs, or disposal.

Subsidiary Ledgers:

01 – Firefighting Equipment and Accessories

02 – Flood Rescue Equipment

03 – Earthquake Rescue Equipment

04 – Volcanic Eruption Rescue Equipment

05 – Landslide Rescue Equipment

5.3 On the other hand, COA Circular No. 2022-004 dated May 31, 2022, provides the

guidelines on the implementation relative to the increase in the capitalization

threshold from ₱15,000.00 to ₱50,000.00. Specifically, Section 4 thereof requires that

tangible items that meet the definition and recognition criteria of Property, Plant, and

Equipment (PPE) but cost is below ₱50,000.00 shall be accounted in the books of

39