3.5 The Municipal Accountant mentioned that the same practice has been followed since

she assumed office more than 10 years ago.

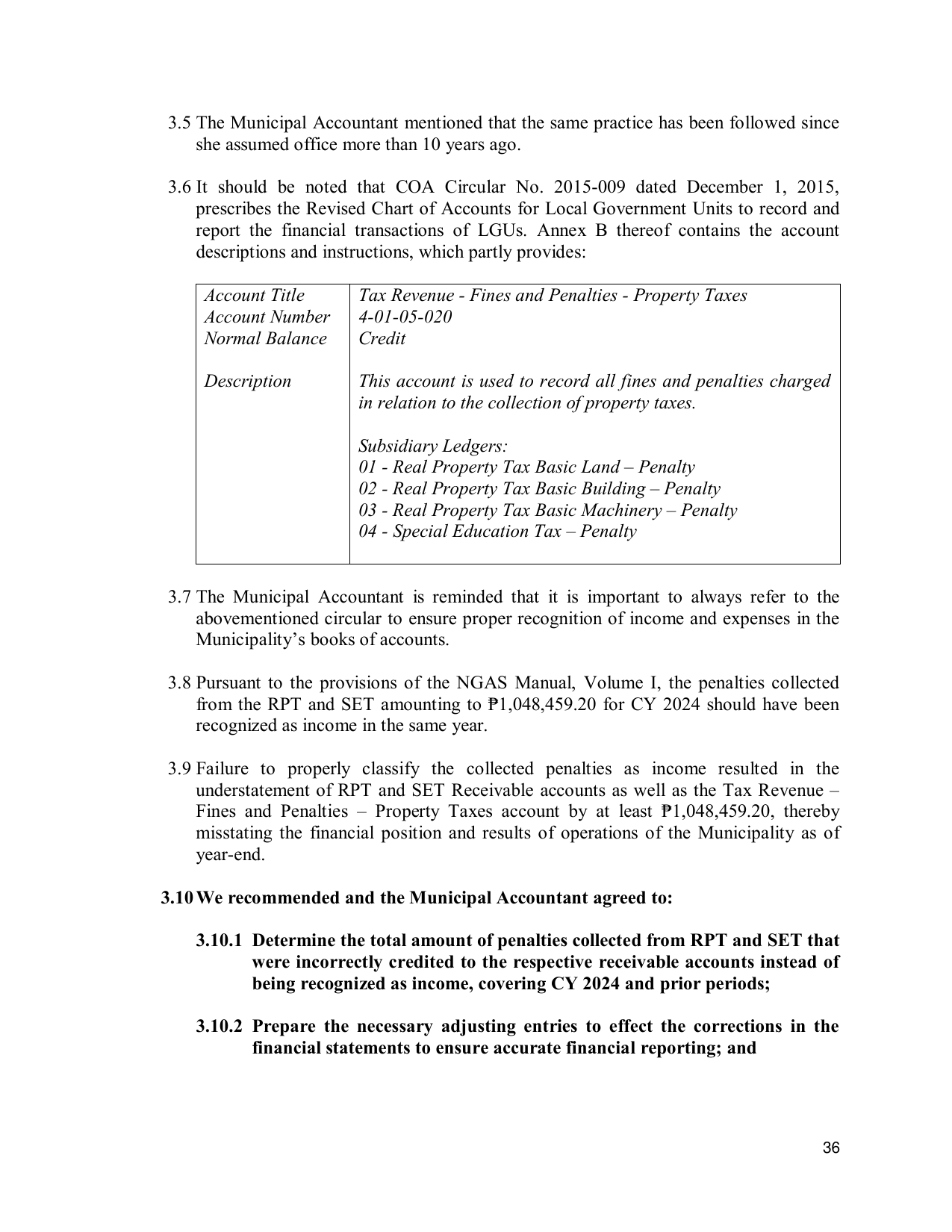

3.6 It should be noted that COA Circular No. 2015-009 dated December 1, 2015,

prescribes the Revised Chart of Accounts for Local Government Units to record and

report the financial transactions of LGUs. Annex B thereof contains the account

descriptions and instructions, which partly provides:

Account Title Tax Revenue - Fines and Penalties - Property Taxes

Account Number 4-01-05-020

Normal Balance Credit

Description This account is used to record all fines and penalties charged

in relation to the collection of property taxes.

Subsidiary Ledgers:

01 - Real Property Tax Basic Land – Penalty

02 - Real Property Tax Basic Building – Penalty

03 - Real Property Tax Basic Machinery – Penalty

04 - Special Education Tax – Penalty

3.7 The Municipal Accountant is reminded that it is important to always refer to the

abovementioned circular to ensure proper recognition of income and expenses in the

Municipality’s books of accounts.

3.8 Pursuant to the provisions of the NGAS Manual, Volume I, the penalties collected

from the RPT and SET amounting to ₱1,048,459.20 for CY 2024 should have been

recognized as income in the same year.

3.9 Failure to properly classify the collected penalties as income resulted in the

understatement of RPT and SET Receivable accounts as well as the Tax Revenue –

Fines and Penalties – Property Taxes account by at least ₱1,048,459.20, thereby

misstating the financial position and results of operations of the Municipality as of

year-end.

3.10 We recommended and the Municipal Accountant agreed to:

3.10.1 Determine the total amount of penalties collected from RPT and SET that

were incorrectly credited to the respective receivable accounts instead of

being recognized as income, covering CY 2024 and prior periods;

3.10.2 Prepare the necessary adjusting entries to effect the corrections in the

financial statements to ensure accurate financial reporting; and

36