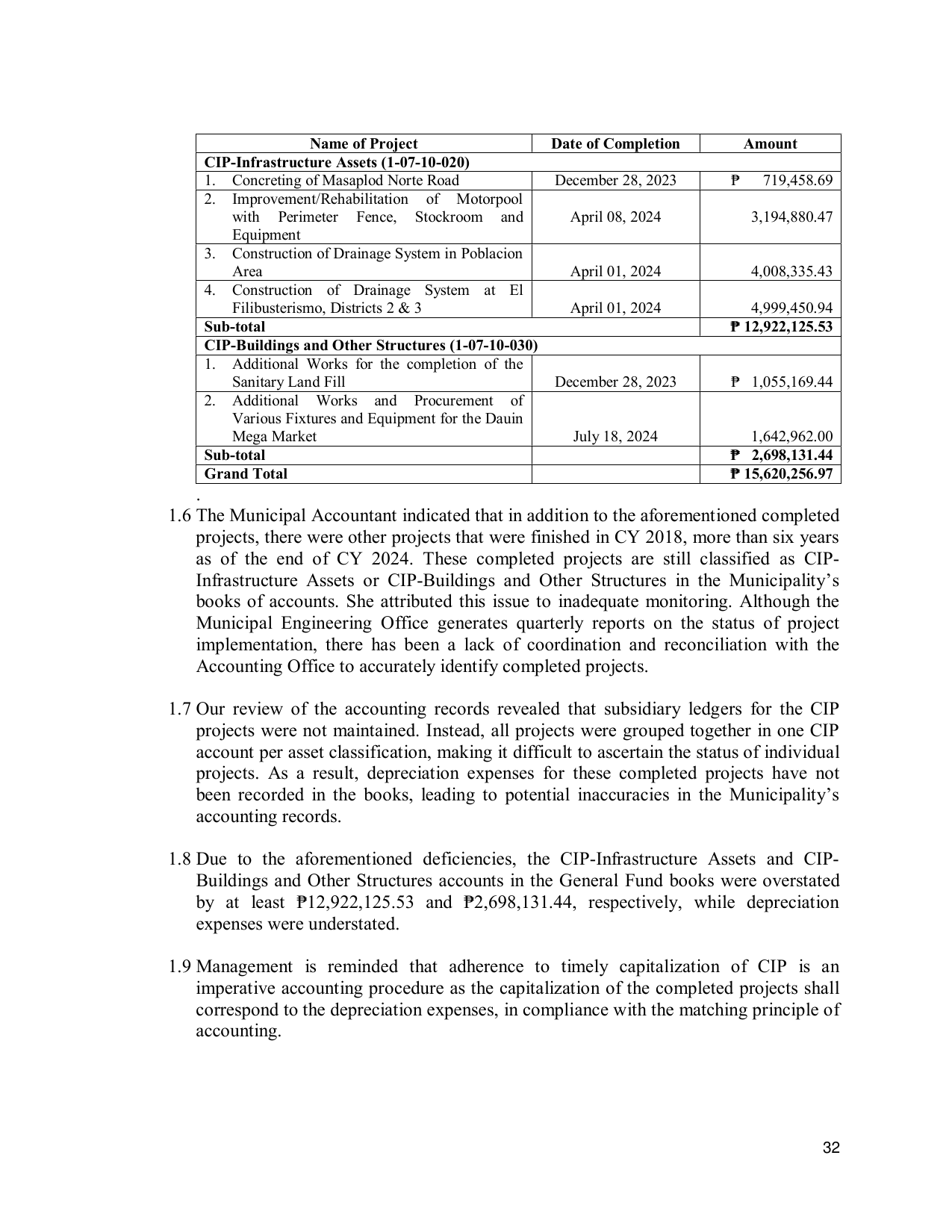

Name of Project Date of Completion Amount

CIP-Infrastructure Assets (1-07-10-020)

1. Concreting of Masaplod Norte Road December 28, 2023 ₱ 719,458.69

2. Improvement/Rehabilitation of Motorpool

with Perimeter Fence, Stockroom and April 08, 2024 3,194,880.47

Equipment

3. Construction of Drainage System in Poblacion

Area April 01, 2024 4,008,335.43

4. Construction of Drainage System at El

Filibusterismo, Districts 2 & 3 April 01, 2024 4,999,450.94

Sub-total ₱ 12,922,125.53

CIP-Buildings and Other Structures (1-07-10-030)

1. Additional Works for the completion of the

Sanitary Land Fill December 28, 2023 ₱ 1,055,169.44

2. Additional Works and Procurement of

Various Fixtures and Equipment for the Dauin

Mega Market July 18, 2024 1,642,962.00

Sub-total ₱ 2,698,131.44

Grand Total ₱ 15,620,256.97

.

1.6 The Municipal Accountant indicated that in addition to the aforementioned completed

projects, there were other projects that were finished in CY 2018, more than six years

as of the end of CY 2024. These completed projects are still classified as CIP-

Infrastructure Assets or CIP-Buildings and Other Structures in the Municipality’s

books of accounts. She attributed this issue to inadequate monitoring. Although the

Municipal Engineering Office generates quarterly reports on the status of project

implementation, there has been a lack of coordination and reconciliation with the

Accounting Office to accurately identify completed projects.

1.7 Our review of the accounting records revealed that subsidiary ledgers for the CIP

projects were not maintained. Instead, all projects were grouped together in one CIP

account per asset classification, making it difficult to ascertain the status of individual

projects. As a result, depreciation expenses for these completed projects have not

been recorded in the books, leading to potential inaccuracies in the Municipality’s

accounting records.

1.8 Due to the aforementioned deficiencies, the CIP-Infrastructure Assets and CIP-

Buildings and Other Structures accounts in the General Fund books were overstated

by at least ₱12,922,125.53 and ₱2,698,131.44, respectively, while depreciation

expenses were understated.

1.9 Management is reminded that adherence to timely capitalization of CIP is an

imperative accounting procedure as the capitalization of the completed projects shall

correspond to the depreciation expenses, in compliance with the matching principle of

accounting.

32